Using Aggregated Data to Analyze Specialty Contractor Performance

Many contractors today use some type of construction management software to oversee the myriad of details inherent to projects both large and small — from billing and invoicing to inventory and timelines. These details help contractors improve workflows and grow profits by creating a unified set of data that can help optimize business performance.

While this information has always helped contractors manage their companies individually, it’s now being aggregated and analyzed by Trimble Viewpoint, a construction ERP company that began pulling this data from roughly 1,000 customers and publicizing it into a Quarterly Construction Metrics Index starting in Q4 2020. The index, which is designed to help industry leaders understand the current construction landscape and assess how their own companies are performing against industry averages, tracks metrics that provide an overall snapshot of the health of the industry, including as it pertains to specialty contractors — project starts, contract values, hiring trends, and cash flow statistics.

While various industry groups and governing bodies regularly publish industry benchmarks, using data pulled from a customer base provides a deeper, more insightful look at data that is used for day-to-day business management. The following is a snapshot of this data for the last three quarters as it relates to specialty contractors, along with an examination of what it means for the vertical in retrospect and looking ahead to the rest of the year.

The challenge of 2020

2020 was a challenging year for the construction industry with project starts and hiring both down 30% and contract values down 25%. However, according to the Quarterly Construction Metrics Index for Q4 2020, specialty contractors had a smoother ride compared to general contractors and heavy highway/civil contractors that saw significantly lowered project starts, hiring rates, and contract values.

While the reasons vary by business, much of this was attributed to specialty contractors being able to pick up work left behind by general contractors and because of their service businesses, which largely continued unabated despite the pandemic.

A rough start to 2021

Surprisingly, the Q1 2021 Index indicated that specialty contractors hit a few bumps at the beginning of 2021, seeing declines when it came to pending jobs, contract values, and hiring. Specifically, pending jobs declined 25% to 30% in January and February compared to the same period in 2020 (Fig. 1).

Contract values were down 50% in the quarter. Hiring was also down 50% in January/February and down 30% in March.

The continuation of social distancing requirements and distribution issues likely played into delayed project starts, preventing many businesses from functioning properly. The lowered project starts for specialty contractors may have also been due to the abundance of previous work finally catching up with them. One positive stat revealed that specialty contractors spent roughly 150% more in Q1 2021 compared to Q1 2020, which may have indicated they were confident new projects were on the horizon as cash spending is typically an indicator of business confidence.

Andy Gordon, chief operating officer for Colorado-based Encore Electric, says that his company was fortunate to have had a lot of work in January and February. This was largely due to the health care and data center vertical markets, both of which saw active growth during the pandemic. At the same time, “there was a lot of uncertainty with our sales funnel and many projects were delayed, redesigned, or altogether canceled. Additionally, this was when commodities, particularly steel, plastics, copper, and aluminum, became very unstable in both cost and availability,” he says.

The beginning of a recovery?

In contrast, the Q2 2021 Index demonstrated that specialty contractors experienced a sizable bounce back. Backlogs increased 20%, mostly due to big project increases in April (45%) and May (50%). Net hiring increased 9.7% (Fig. 2), with June being the highest month of growth.

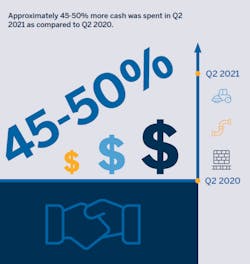

Contract values remained stable, and 43% more cash was spent in Q2 2021 as compared to Q2 2020 (Fig.3).

During the second quarter of 2021, the industry as a whole benefited from the rebound in projects that were put on hold during 2020. Investment in existing structures and infrastructure remained high throughout the quarter, boosted by favorable finance rates, and contributing to the project increases seen in the specialty trades.

Continued high growth in residential construction subcontracts and increases in service work (as opposed to new construction work) by specialty trade contractors likely fueled hiring; however, recruiting skilled labor has and will continue to be a challenge for the industry.

Finally, the significant increase in cash spending is a partial bellwether for increasing confidence and backlogs in the market. Nonetheless, continued uncertainties in the supply chain and volatile material prices may dampen this impact looking ahead.

“Q2 2021 felt like the most normal quarter of any of the past 18 months,” Gordon says. “Projects that were slow to start, started. New project contracts were awarded, and there were fewer COVID-19 impacts on our workforce. Our recruiters were constantly looking to bring in new people, and I don’t anticipate that changing anytime soon.”

A look ahead

The remainder of 2021 continues to offer a ray of hope for specialty contractors, many of whom successfully weathered the initial storm of 2020 and have seen their businesses rebound throughout this year — particularly during the last quarter. That being said, variables outside of anyone’s control continue to exist (from material prices and supply chain issues to the Delta variant and the Infrastructure Bill), which may elevate or hinder the industry’s ability to recover, depending on how the chips fall.

Anne Hunt is the director of data and analytics for Trimble Viewpoint. For more information, visit www.viewpoint.com.

About the Author

Anne Hunt

Anne Hunt is the director of data and analytics for Trimble Viewpoint. She leads the incubation and innovation of new data-first services to revolutionize how clients and the construction industry at large operates.