It’s tough to say if forecasting 2023 market conditions for the electrical construction market will be harder this year than it has been in the past. That’s because you’ll have to factor in a unique mix of new and old macroeconomic factors — not to mention industry-specific market conditions — when developing your electrical 2023 market forecast, including price increases, product shortages, and concerns over the long-term demand for office space. What’s different about this year’s construction outlook are the concerns about a possible 2023 recession and figuring out how (or if) any downturn will affect your company’s business mix and local market’s economic conditions.

National view

As you prepare for 2023, remember that local market conditions can vary wildly from any macroeconomic prognostication. Be sure to use any national outlook just as a point of comparison to see how your local market, state, or region compares in terms of any forecasted rate of change in revenue. Forecasts for the 2023 nonresidential construction market vary widely. For example, in its Consensus Construction Forecast, the American Institute of Architects (AIA) relies on forecasts from eight leading construction economists — Dodge Construction Network, S&P Global Market Intelligence, Moody’s Analytics, FMI, ConstructConnect, Associated Builders & Contractors, Wells Fargo Securities, and Markstein Advisors.

AIA’s consensus forecast for the 2023 nonresidential market calls for a 6% increase. The panel of economists’ forecasts reflected the diversity of opinion on 2023’s business prospects and ranged from three double-digit increases — 14.7% by FMI; 12.9% by ConstructConnect; and 10.6% by Dodge Construction Network — to three forecasts that were less than half the growth rate of AIA’s Consensus Forecast for the nonresidential segment. Calling for less growth were economists from Wells Fargo Securities, Associated Builders & Contractors, and Markstein Advisors. They see nonresidential market growth coming in at less than a 3% increase next year.

Bookmark AIA’s website, www.aia.org, if you want regular analysis of construction market conditions. AIA Chief Economist Kermit Baker provides updates on the AIA Consensus Construction Forecast twice a year and manages AIA’s Architecture Billings Index (ABI), which provides an indication of design and billings activity at architectural firms. Because architects typically are involved in the construction cycle at least nine to 12 months before a project breaks ground, the ABI is a trusted leading indicator for nonresidential construction activity.

While the ABI has been strong for most of 2022, Baker said in the most recent report that some signs of an economic slowdown are emerging. AIA’s ABI score for October was 47.7 points — the first decline in billings since January 2021 (any score below 50 indicates a decline in firm billings). Inquiries into new projects continued to grow in October with a score of 52.3 points, while the value of new design contracts declined (with a score of 48.6 points).

“Economic headwinds have been steadily mounting and finally led to weakening demand for new projects,” he said. “Firm backlogs are healthy and will hopefully provide healthy levels of design activity against fewer new projects entering the pipeline should this weakness persist.”

While presenting his 2023 construction forecast in a November 15 webinar, Richard Branch, chief economist for Dodge Construction Network, said that although he has built out both downside and upside 2023 forecasts, his base forecast for the construction industry does not call for a recession. He believes spending on total U.S. construction starts will register little change on a percent basis and drop fractionally in 2023 to $1,068 billion from $1,083 billion. “Assuming there is no recession, construction is flat in 2023,” he said.

Branch’s base case for U.S. GDP growth calls for a 0.7% increase, while his downside/recessionary scenario ratchets GDP growth down 2%. His “Upside Forecast” sees a 4.1% increase in GDP growth for next year.

He said that while the number of developers still building, the recent easing in price increases for construction materials, some large hospital and industrial projects in the pipeline, and passage of some large local bond measures for construction could stop a recession in the construction market, pricing pressures are still a major concern. “Pricing will be challenging going into first half of 2023 but will see improvement in the back half,” he said.

The largest of the recently passed major bond measures that will support construction in some local markets include $2.4 billion for technology and stadium improvements by the Austin, Texas, Independent School District (ISD); $3.2 billion for facility improvements by the San Diego Unified School District (USD); and $1.7 billion by the Long Beach, Calif., USD.

While some local metros may have reason to cheer in the institutional, educational, and industrial market, Branch said widespread challenges in the residential market will be a drag on construction. That’s an issue for contractors and their suppliers as well as design professionals because of the impact housing has on other segments of the business.

“I have always viewed the construction sector as a train, and residential leads the train as the engine,” said Branch, explaining that the housing market will continue to suffer from buyers’ affordability issues, higher mortgage rates, increases in lot acquisition costs, building material costs, and labor shortages. He believes the trough in spending on single-family housing will occur late in 1Q or early 2Q of 2023, but that the market overall will see a 6% decline next year, assuming there is no recession. Multi-family housing will continue to be the stronger segment, he said.

Next year’s challenges

2023 macroeconomic outlook. Monthly surveys of senior executives can offer valuable market insight to get a broad sense of economic conditions in the electrical market and the overall U.S. economy. In its “Electrostats” column, Electrical Wholesaling publishes regular updates of the ElectroBusiness Conditions Index (EBCI), a monthly survey of executives at electrical manufacturers who are members of the National Electrical Manufacturers Association (NEMA). The EBCI Index has been sliding deeper into negative territory in 3Q 2022. In the most recent report published in late October, NEMA said, “Economic headwinds, including rising interest rates and a deeply unsettled geopolitical environment contributed to the general malaise, but policy support for ‘electrification and energy efficiency’ provided a backstop to the otherwise glum outlook.”

The Conference Board offers two solid monthly macroeconomic indicators — its Measure of CEO Confidence and its U.S. Leading Economic Indicators (LEI). The most recent reports were both pessimistic. The Conference Board said CEO confidence sunk further to start Q3 and is at its lowest level since the Great Recession, while the association’s LEI report said a recession is likely before year-end.

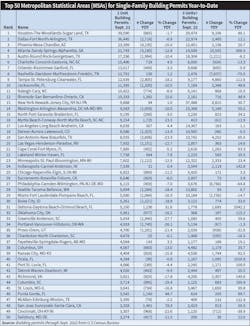

Price increases continue for electrical products. Year-over-year price increases for electrical products are decelerating but remain at near historically high levels, according to Electrical Marketing’s monthly Electrical Price Index (EPI). The October 2022 EPI data showed additional cooling in prices for key electrical products, with a monthly decline of 0.7% and a 9% year-over-year (YOY) increase to a 197.6 reading for the total index. Power wire & cable bucked this trend with a 2.1% monthly increase that supported its 10.8% YOY pricing gain. With a decline of 4.7%, conduit fittings had the biggest monthly drop. In “normal” times, you rarely see monthly price increases in the EPI of more than 1%. That’s why the string of double-digit YOY price increases that hit the market each month from April 2021 through August 2022 is so out of the ordinary. See Table 1 for data on other price increases in the EPI.

Long lead times. Although lead times for many electrical products aren’t as bad as they used to be, in many cases, they are still months from normal. Switchgear has seen lead times that extend out more than a year, according to one distributor’s response in the Electrical Marketing/Vertical Research Partners (VRP) quarterly survey. They are also still an issue with products like lighting controls and automation equipment powered or controlled by semiconductor chips.

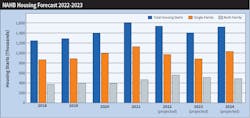

A tough slog for single-family construction. Single-family construction will probably be the slowest market sector over the next year or two, as sky-high interest rates, affordability issues, and lack of buildable lots in many popular markets are pummeling home builders. Market conditions for multi-family construction aren’t as dismal. While some Sunbelt markets are scratching out increases in single-family construction, the national data on housing starts and building permits is downright ugly. Multi-family construction is also expected to slow, but according to National Association of Home Builder’s (NAHB) 2022 forecast, it will be up 18.1% this year before sliding 8% in 2023. See the Figure.

“This will be the first year since 2011 to post a calendar year decline for single-family starts,” said Robert Dietz, chief economist, NAHB. “We are forecasting additional declines for single-family construction in 2023, which means economic slowing will expand from the residential construction market into the rest of the economy.”

Jerry Konter, NAHB chairman and a home builder/developer from Savannah, Ga., echoed this sentiment. “Mirroring ongoing falloffs in builder sentiment, builders are slowing construction as demand retreats due to high mortgage rates, stubbornly elevated construction costs, and declines for housing affordability,” he added.

The impact of hybrid/remote work on office construction and renovation. While work-at-home trends vary and evolve by region and type of industry, the post-COVID reality or remote officing is definitely affecting demand for new office space.

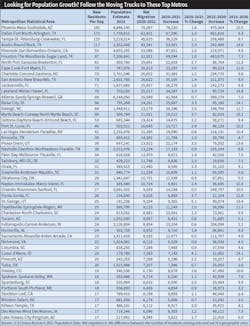

It’s a huge issue in New York, for example. While the Big Apple has some major office projects underway, the results of a survey by the Partnership for New York City points to what could be the long-term trend of fewer people working five days a week in the city’s offices. The survey of more than 160 major Manhattan office employers said that, as of mid-September 2022, only 49% of Manhattan office workers are currently at the workplace on an average weekday. The Partnership said return-to-office rates are projected to increase gradually through the rest of 2022, with 54% of workers expected in the office on an average weekday by January 2023 (see Table 2 for the largest markets for office space in the United States).

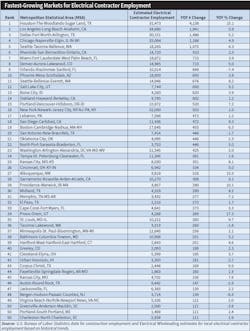

Labor shortages persist. Even though total U.S. employment at electrical contracting firms is trending at more than 1 million employees for the first time ever, electrical contractors seem to be having the most trouble attracting and keeping new employees. This challenge has created a market opportunity for companies on the supply side that can provide new tools and preassembled electrical products that help electrical contractors work smarter and more efficiently in the field. Check out Table 3 to see which local markets added the most electrical contractor employees over the past year.

Reasons to be cheerful

Federal infrastructure spending programs will spark investments in infrastructure, renewables and construction of massive factories to produce semiconductors, electric vehicles and lithium batteries for EVs, photovoltaic systems, and microgrids. Funds from federal programs like the Infrastructure Investment and Jobs Act (IIJA), CHIPS and Science Act, and the Inflation Reduction Act (IRA) will have a direct impact on the electrical construction market because of their intent to fund the installation of residential and commercial PV systems, microgrids, EV charging systems, grid upgrades, and renovation of commercial facilities with more efficient electrical and mechanical systems. At least one electrical manufacturer told EC&M recently that this influx of federal funding will be a “once-in-a-lifetime opportunity” for the electrical industry.

By now, many folks have heard about all of the federal stimulus funding for electric grid modernization, EV charging stations and residential PV installations. But there’s a lesser-know source of tax deductions that could be of interest to many of your customers that you can use to land new energy-retrofit jobs. A post at www.cbh.com says that in its Section 179, which covers the Energy-Efficient Commercial Building Deduction, the IRA will almost triple the per-sq-ft tax deduction in 2023 that building owners can get for energy-efficient retrofits in commercial or multi-family building from $1.88 per sq ft to $5 per sq ft.

Life-science laboratories and data centers — two patches of growth. In the latest Dodge Momentum Index, Sarah Martin, senior economist for Dodge Construction Network, said data centers and life science laboratories “have thrived in 2022 and continue to support strength in planning activity.”

Life-science laboratories are an interesting niche because of the money biotech companies are investing in the development of new pharmaceutical drugs. Demand for the construction of these facilities has not been as affected by the work-from-home trend as other real-estate sectors because folks can’t bring home the high-dollar lab equipment and work stations. If you ever want to learn more about the growth in this sector, check out the investment analyses of Alexandria Real Estate Equities (Ticker symbol: ARE), which can often be found as a top pick for REIT (Real Estate Investment Trust) stocks.

The world of mega-projects. EC&M’s editors don’t remember ever seeing so many billion-dollar factories underway at the same time — and it’s even more unusual that so many of them are in these same areas (semiconductors, electric vehicle plants, and EV battery plants). U.S. Census Bureau data is picking up on this spending. For the better part of 2022, industrial construction spending has been one of the strongest elements of the overall construction market, and the YOY increases in spending in some segments leap off the page. Through September 2022, total manufacturing construction spending was up 43.3% over September 2021 to $113,399 million. The computer/electronic/electrical segment hit $4,291 million in September 2022, an amazing 319.7% increase in one year. Tech spending on data centers and all that EV and battery plant construction is pushing spending into the stratosphere.

The IRA and CHIPS legislation mentioned earlier will certainly spark construction of plants in these areas, but even before these bills became law, manufacturers had announced their intentions to invest billions of dollars in these areas. Table 4 highlights the largest of these plants, but it seems like a week doesn’t go by when you hear about another new project hitting the drawing boards. In mid-November, AP reported that a Freyr Battery, a Norwegian company, will invest $2.6 billion in an electric battery factory located in Newman, Ga. (near Atlanta). Many of the new projects that made the news over the past year in the EV or semiconductor industries were substantially larger than this facility. For example, Intel announced plans this year that it would build a $20-billion semiconductor campus in Licking, Ohio, and make a $20-billion investment in its existing Ocotillo plant in Chandler, Ariz. Not to be outdone, Intel competitor Texas Instruments will spend $30 billion on several semiconductor chip fabrication plants in Sherman, Texas, and Taiwan Semiconductors has a $6-billion plant underway in Phoenix.

In the EV market, some of the larger plants involve Ford and SK Innovation, its EV battery partner, which plan to spend $11 billion on several EV and battery facilities in Glendale, Kan., and Stanton, Tenn. Ford has plenty of competitors building U.S.-based EV plants, too. Rivian plans to build a $5-billion plant straddling Morgan and Walton Counties in Georgia; Hyundai broke also ground on a $5.5-billion factory in Ellabell, Ga., in late October.

The Sunbelt and Intermountain states — the gift that keeps on giving. Yes, the Sunbelt’s coastal hotspots seem to continually get lashed by hurricanes or lower-grade tropical storms, and many of the region’s roadways are choked with traffic at rush hour. But if you want to find many of the nation’s hottest construction markets, look no further than the Sunbelt region.

Let’s start in Nashville to see the tremendous residential and commercial growth Music City has seen over the past decade. From there, let’s wander through the country roads hugging the shoulders of North Carolina’s Smoky Mountains to see all the new vacation/retirement homes being built there. Swing through all the new commercial development in Charlotte and Raleigh-Durham, N.C., and then hit the Outer Banks — another magnet for vacation/retirement homes. After that, it’s time to venture further south down Route 95 past South Carolina’s island-speckled coastline and retirement getaways, and check out what’s promoted as the I-85 Industrial Boom Belt from South Carolina to Georgia. And don’t forget to venture on to the state’s hub city of Atlanta. Figure out the best time to beat the traffic, but now it’s time to move on to Florida and its seemingly ever-growing metros of Orlando, Tampa-Clearwater Beach-St. Petersburg, Sarasota, Fort Myers, and Naples. Catch your breath and grab a grouper sandwich, but then motor through Texas and the colossal new residential developments you see in Houston, Dallas, Austin, and San Antonio (Table 5). Don’t forget the gushing oil business of Midland-Odessa either. Take a break for a bit, but then head on to Intermountain Region, the other U.S. region with a major concentration of fast-growing markets. Start in the sprawling Valley of the Sun in Phoenix, which once again leads the nation in net migration (Table 6), before heading north to the bright lights of Las Vegas. Pack your skis or hiking boots and explore all the growth in Salt Lake City, Orem, Ogden, Provo and Logan, Utah, along the 80-mile Wasatch Mountains front and the epic outdoors adventures in the nearby peaks. You can either head north to Boise, Idaho, to see how that metro has grown over the past few years, or east to Colorado’s Front Range that stretches about 175 miles from Fort Collins south through Boulder, Denver, and Colorado Springs — home to millions of new residents and hundreds of new businesses drawn to the outdoor lifestyle. Complete this road trip, and you will have seen most of the metros that continually rank as the fastest-growing markets in the United States.

Looking ahead. The chances for a mild recession in 2023 seem pretty good, but you can still find some economists who think the U.S. economy can escape any serious downturn next year. Of course, if the war in Ukraine took an unexpected turn (or the current meltdown in parts of the cryptocurrency market spread to equities and bonds) we could be looking at a “Black Swan” event that could radically change economic conditions. However, this generation of managers in the electrical construction market have already guided their companies through the depths of the pandemic. Therefore, the crisis management skills they developed/utilized in the COVID-19 era should be enough to get them through any new and nasty economic surprises.

About the Author

Jim Lucy

Editor-in-Chief, Electrical Wholesaling & Electrical Marketing

Over the past 40-plus years, hundreds of Jim’s articles have been published in Electrical Wholesaling, Electrical Marketing newsletter and Electrical Construction & Maintenance magazine on topics such as electric vehicles, solar and wind development, energy-efficient lighting and local market economics. In addition to his published work, Jim regularly gives presentations on these topics to C-suite executives, industry groups and investment analysts.

He launched a new subscription-based data product for Electrical Marketing that offers electrical sales potential estimates and related market data for more than 300 metropolitan areas. In 1999, he published his first book, “The Electrical Marketer’s Survival Guide” for electrical industry executives looking for an overview of key market trends.

While managing Electrical Wholesaling’s editorial operations, Jim and the publication’s staff won several Jesse H. Neal awards for editorial excellence, the highest honor in the business press, and numerous national and regional awards from the American Society of Business Press Editors. He has a master’s degree in communications and a bachelor’s degree in journalism from Glassboro State College, Glassboro, N.J. (now Rowan University) and studied electrical design at New York University and graphic design at the School for Visual Arts.