Key Takeaways

- Data center construction remains the primary growth driver, with projects exceeding $10 billion and accounting for a significant share of nonresidential spending growth.

- Market bifurcation is evident, with high growth in data centers contrasted by slow or declining activity in residential, office, and industrial sectors.

- Tariffs, immigration enforcement, and supply chain issues continue to influence product pricing and labor availability, impacting project timelines and costs.

- Megaprojects of $1 billion or more, especially in data centers, are crucial to industry growth, with investments expected to reach trillions globally by 2030.

Providing a forecast for the 2026 electrical construction market is a bit trickier than usual because it’s hard to predict exactly where six key market drivers — product pricing, tariffs, electrical contractor employment trends (Table 1), federal immigration policy, construction spending, and megaprojects — will be trending next year.

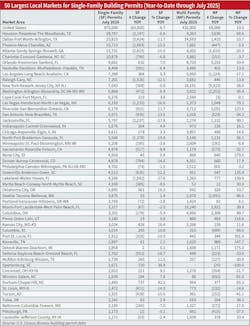

Electrical product prices are reasonably tolerable right now. But lingering uncertainties remain over which products will be affected by higher tariff rates; product areas are still seeing double-digit year-over-year (YOY) increases. According to the latest Electrical Price Index published monthly by Electrical Marketing newsletter at www.electricalmarketing.com, prices for building wire (+10.2%), switchgear (+11.9%), and fuses (+10.5%) are up double digits year-over-year through August 2025 (Table 2).

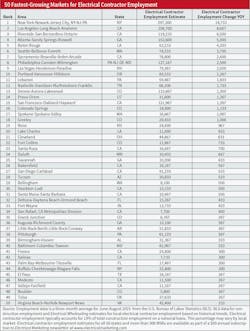

National electrical contractor employment appears to be at historically high levels of more than one million workers, but the most recent data available at press time goes back to July — and those numbers showed some softening. It’s tough to get an up-to-date snapshot of contractor employment trends because no federal data has been available from the U.S. Census Bureau, which collects employment data as well as data on building permits (Table 3), housing starts, and construction spending.

Economists also believe the Trump Administration’s immigration policy is tightening the flow of foreign-born workers into the construction industry because they fear job-site ICE raids and deportation. A recent survey by the Associated General Contractors (AGC), Arlington, Va., said the construction industry has been impacted by stepped-up immigration enforcement. “Twenty-eight percent of respondents report being affected directly or indirectly by immigration enforcement activities during the past six months,” noted the press release. “Specifically, 5% report a job site or off site was visited by immigration agents. Ten percent say workers left or failed to appear because of actual or rumored immigration actions. And 20% report subcontractors lost workers.”

The impacts of immigration enforcement varied considerably by state, according to AGC survey results. “Contractors in Georgia, Virginia, Alabama, Nebraska, and South Carolina were more likely to be impacted, ranging from 75% of firms in Georgia to 36% in South Carolina. Conversely, only 8% of firms in Idaho and 9% in Alaska reported being impacted by immigration enforcement activities during the past six months.”

A tale of two markets

One economic trend is clear in the electrical construction market: If your company is fortunate enough to be working on data centers (or is located in one of the Sunbelt markets that seem to have perpetually sunny business climates), you are probably feeling pretty darn good about your 2026 business prospects. On the flip side, if acres of data centers aren’t being built in your local market — or if the local economy is bumping along at a slow or no-growth rate because there isn’t much new nonresidential or residential business in the pipeline — the future might not look quite so bright.

Right now, only the most pessimistic economists are calling for an outright recession in the United States, but many, if not most, will bend your ear about the “K-shaped economy,” where some segments of the overall economy are doing very well while other sectors are struggling to grow.

The electrical construction industry is a good example of the K-shaped economy in action. Riding the upper growth arm of the “K” is the data center market (growing annually at a high double-digit growth rate). Hanging onto the lower leg of the “K” with little or no growth are many other key construction market segments, such as residential and office construction and much of the industrial market (outside of semiconductor plants).

These “bifurcated” market conditions are likely to last through most of 2026, although the federal tax cuts that take effect next year (and any further cuts in interest rates) should juice up capital spending on new construction and renovation projects and make residential mortgages more palatable for many homebuyers, stimulating home construction.

Impact of megaprojects

In ConstructConnect’s Construction Economy Outlook Fall Webcast held on November 13, Chief Economist Michael Guckes said the impact of megaprojects of $1 billion or more in total contract value cannot be underestimated — and that these jobs account for much of the growth in the nonresidential construction market.

Not surprisingly, many of these megaprojects are data centers. In the past, only the largest data centers topped $1 billion in total contract value. However, over the past year or two, the size of these jobs has increased dramatically. For example, the contract value for the proposed La Osa data center project in Eloy, Ariz., tops $30 billion, and 10 other data center projects of over $10 billion in total contract value were either in the proposal or design stage or broke ground from July 2025 through October 2025. Of the 34 megaprojects EC&M’s editors found topping $1 billion in contract value during this time period,13 were data centers (accounting for roughly 60% of their combined contract value), as shown in Table 4.

Dominance of data centers

Distributor, independent rep, and manufacturer respondents to the quarterly survey published by Electrical Wholesaling and Vertical Research Partners (VRP), Stamford, Conn., an equity research firm, believe data center construction will continue at its rapid pace into the new year. “Data centers remain the primary driver of activity, with hyperscale demand notably robust and no signs of a slowdown,” said Nick Lipinski a VRP equity analyst and vice president. “Outside of data centers, the industrial and construction demand environment remains relatively subdued.”

Lipinski also said the distributors, manufacturers, and independent manufacturers’ reps who responded to the survey reported a wide range of results “with the extremes ranging from strong double-digits on the upside to significant double-digit declines on the downside.” He also noted: “There was some degree of deceleration in September, mirroring the slowdown suggested in chemical and transportation markets. However, this was not widespread and did not seem overly concerning to respondents in terms of influencing the forward outlook. It appears to have been more of a modest sequential step down after robust activity over the summer. The general view is that trends in Q3 will continue through year end, and 2026 should see incremental improvement.”

Lipinski also said there were clear regional and industry sector divergences in the respondent commentary in Q3, and that survey respondents large enough to participate in the data center end market are seeing a continued robust demand environment that seemed to accelerate in the quarter.

“The data center market in the United States has grown to the point of parity with office construction in dollar value,” he said. “Further, the electrical intensity in a data center is much higher than for an office building or any other nonresidential application. This is contributing to the bifurcation of results with data center strength more concentrated in larger distributors versus general construction activity, which is more relevant for a broader swath of players.”

He added that outside of data centers, the general industrial and construction landscape is relatively subdued, although there were pockets of strength in the food and beverage sector.

Examples of data centers’ domination of the construction market were easy to find. For instance, in the September 2025 Dodge Momentum Index (DMI), published monthly by Dodge Construction Network, Sarah Martin, Dodge’s associate director of forecasting, said that in September, without data centers, commercial planning would have only increased 0.5% for the month. The DMI is a monthly measure based on the three-month moving value of nonresidential building projects going into planning, shown to lead construction spending for nonresidential buildings by a full year to 18 months.

“Planning momentum remained steadfast for data centers, health care, and public buildings throughout September and will correlate to stronger construction spending in early 2027,” said Martin in the press release. “After a prolonged period of uncertainty, owners and developers are advancing projects into planning, but activity is expected to normalize in future months.”

A recently published research report on data centers, “Data Centers Lead the Way,” also pointed to the huge impact data centers are having on the electrical construction industry. Author Kevin Coleman said electrical products and systems account for 40% or more of the total construction spend in data centers. Published by Channel Marketing Group, Raleigh, N.C., and DISC Corp, Houston, the report also said that from March 2024 through the third quarter of 2025, data center investments accounted for more than 70% of the increase in private nonresidential construction spending in the United States.

“The numbers are staggering,” wrote Coleman. “At the current pace, 2025 data center construction starts will hit $46 billion — a 55% YOY growth rate. And this isn’t a temporary spike. McKinsey estimates that by 2030, data centers will require $6.7 trillion of investment worldwide to keep pace with demand.”

Kermit Baker, the chief economist for the American Institute of Architects (AIA), Washington, D.C., and author of one of the best construction forecasts available (Consensus Construction Forecast), said growth in the level of spending on data centers is unprecedented and expected to continue at an elevated pace. “After increasing by more than 50% in 2024, spending is expected to grow by another 33% in 2025 and by an additional 20% in 2026,” he said in the AIA forecast, which was published in July. “However, even in this sector, there are growing concerns that electrical equipment shortages, power requirements, and community opposition may slow the pace of growth.”

Slow growth ahead for nonresidential market

In his July update to AIA’s Consensus Construction Forecast for 2025-2026, Baker says there’s both good and bad news about nonresidential construction spending on buildings. “First, the good news,” he said. “In spite of stubbornly high long-term interest rates, inflation rates stalled above the Federal Reserve Board’s target, falling consumer confidence scores, disappointing levels of home building activity, rising tariff rates for many inputs to construction, and construction labor shortages exacerbated by restrictive immigration policies, the outlook for the remainder of the year and into 2026 is largely unchanged from where it was at in the beginning of the year.”

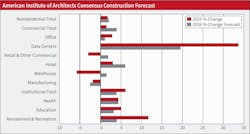

What’s the bad news? “The outlook for spending entering the year was very pessimistic. The consensus is that overall spending on nonresidential buildings not adjusted for inflation will increase only 1.7% this year and grow very modestly to just 2% next year (Fig. 1). The commercial sector outlook is about on par with the broader industry, with a projected 1.5% increase this year rising to 3.9% in 2026. Spending on the construction of manufacturing facilities — the industry’s bright spot in recent years — is expected to decline 2% this year with an additional decline of 2.6% next year. Institutional facilities are expected to be the strongest sector with projected gains of 6.1% this year and another 3.8% in 2026.”

Blue-Chip office space in demand, but expect another tough year for office construction

Baker also said in AIA’s Consensus Construction Forecasts that remote work has contributed to a historically high national office vacancy rate of near 20%. Although office retrofits in existing facilities have increased, he maintains the spending in this construction segment isn’t high enough to offset the decline in spending on new offices. In some cities, the conversion of offices or hotels to apartments is providing a welcome boost to office construction, as is the case in New York City.

While office vacancy rates have been at historically high levels in many metropolitan markets, the Chicago-based JLL real estate advisory firm said in its Office Market Dynamics report that vacancy rates were beginning to decline in Q3 2025. According to the report, “After a prolonged runup that had seen overall vacancy rates nearly double nationally since 2019, office vacancy rates have begun to decline for the first time since early 2019 with vacancy falling five basis points to 22.5% at the end of Q3.” The report went on to say: “Markets in the Sunbelt that have been the beneficiaries of corporate relocations in the past decade, most notably Texas, Florida, North Carolina, Nashville, and Atlanta. These markets have experienced positive net absorption year-to-date and only generated marginal occupancy losses in 2024.”

In its Office Q3 2025 Market Beat report, Cushman & Wakefield, Chicago, said while the demand for top-tier Class A office space is recovering, the construction pipeline has been declining precipitously since its 2020 peak. “Deliveries and starts are hitting lows not seen in the past decade. In Q3 2025, 7.1 million sq ft (msf) of new office space opened, a total that is 30% below the quarterly average since the beginning of 2020. Just 13.4 msf of office space has been delivered year-to-date (YTD), which is a decrease of 50% from a year ago and represents the lowest first three quarters of a year since 2012,” the report said.

The Cushman & Wakefield report projected a national office vacancy rate of 20.7%, with quite a few large market suffering from office vacancy rates of 25% or greater, including Atlanta (25.4%); Austin, Texas (29.4%); Dallas (25.8%); Denver (26%); Los Angeles’ central business district (31%); Minneapolis-St. Paul (28.3%); Manhattan, N.Y.’s Midtown South area (25.6%); Phoenix (27.1%); San Francisco (34%); and Seattle. (29.6%). Some small- and medium-sized markets were seeing much lower vacancy rates for the quarter, according to the report: Charleston, S.C. (7.3%); Colorado Springs, Colo. (9.8%); Fort Myers/Naples, Fla. (4.1%); the Inland Empire region of Southern California (8.8%); and Reno, Nev. (9.5%).

While it’s tough to find many super-large office projects in the pipeline, the BXP’s $2-billion 343 Madison Ave 930,000-sq-ft office tower in Midtown Manhattan is now underway (Photo 1). Being built by Turner Construction, the project will be 46 stories tall and is targeting LEED Platinum certification from the U.S. Green Building Council. Interestingly, JP Morgan’s new 60-story headquarters building — a project with an estimated total construction cost of $3 billion that opened earlier this year — is about four blocks away. That building is one of the tallest offices built in the country over the past few years.

Slowdown expected in industrial spending

Few economists are expecting big growth in the 2026 industrial market. AIA’s Consensus Construction Forecast is calling for a 2.6% decline next year after a 2025 decline of 2%. Six of the 10 construction economists who participate in this forecast are expecting declines in industrial construction in 2026. S&P Global Market Intelligence was the most pessimistic with its forecast for a 15% decline, while economists from Wells Fargo and Piedmont Crescent Capital were the most bullish with forecasts topping 5% (Fig. 2).

Over the past year, at least four industrial projects valued at $1 billion or more entered the construction pipeline. The $10-billion Micron Technology White Pine Commerce Center in Clay, N.Y., (recently put on hold) and the $12-billion Formosa Plastics Sunshine Project in Saint James, La., are in the planning stage. The $7-billion Amkor semiconductor plant in Tempe, Ariz., and the $1-billion Johnson & Johnson Biologics Manufacturing Facility, in Wilson, N.C., are also now underway.

Residential market may start to pick up

The National Association of Home Builders (NAHB), Washington, D.C., is starting to see some signs of growth in the single-family residential market and is forecasting single-family starts to increase 0.6% to 950,000 (Fig. 3). However, it sees multi-family starts declining 3.4% to 396,000.

NAHB pointed to other signs of growth in a recent press release, reporting that future sales expectations surpassed the 50-point breakeven mark in the NAHB/Wells Fargo Housing Market Index (HMI) for the first time since last January, and builder confidence in the market for newly built single-family homes was 37 points in October — up five points from September and the highest reading since April.

“The HMI gain in October is a positive signal for 2026 as our forecast is for single-family housing starts to gain ground next year,” said NAHB Chief Economist Robert Dietz in a press release. “The 30-year fixed-rate mortgage fell from just above 6.5% at the start of September to 6.3% in early October. Combined with anticipated further easing by the Fed, builders expect a slightly improving sales environment — albeit one in which persistent supply-side cost factors remain a challenge.”

In ConstructConnect’s Construction Economy Outlook Fall Webcast on November 13, AIA’s Baker said that, according to a recent survey by the TurboHome ResiClub Housing Sentiment Survey conducted in July, if rates for a 30-year fixed mortgage dropped to 5.5%, 66% of U.S. households would consider that an acceptable rate for the purchase of a home.

Other markets to watch

Judging from the number of projects valued at more than $100 million now in the construction pipeline, the mass transit, hospital and school and university construction market segments seem like they should offer solid growth prospects next year.

Mass transit. Over the past decade, billions of dollars in new and retrofit construction has transformed many of the nation’s airports. Two airport projects in the pipeline are the $700-million Memphis International Airport now underway and the $575-million Cincinnati-Northern Kentucky airport in the planning stage in Erlanger, Ky. Another big airport-related job is the $3-billion renovation of Newark Airport’s AirTrain that broke ground in September 2025 (Photo 2).

Hospitals. AIA’s Consensus Construction Forecast anticipates 4.3% growth in its health segment, even with anticipated growth in 2025. Over the past two years, the largest hospital projects making news included the $3-billion Cooper University Health Care hospital expansion in Camden, N.J., which entered the planning stage in February 2025 (Photo 3); the $1.5-billion Lyndon B. Johnson Hospital replacement in Houston, which began construction in May 2024; and the $1-billion Intermountain Health St. Vincent Regional Hospital in Billings, Mont., which announced plans in November 2024. EC&M editors found at least 27 hospital projects valued at $200 million or more in the pipeline.

Schools and universities. AIA’s Consensus Construction Forecast anticipates 3.2% growth in its health segment, down from 2025’s 5% growth. While facility construction projects at K-12 schools and universities often aren’t as large as the megaprojects in other areas of the nonresidential construction market, there are numerous projects in this niche valued at more than $100 million now in the planning or construction process. EC&M’s editors found 26 projects of this size in the pipeline over the past two years. The largest were the $842-million University of California at San Francisco academic building, which broke ground in September 2024; the $493-million Revere High School project in Revere, Mass., which entered the planning stage in April 2025; the $465-million dormitory at the University of California campus in Berkeley, Calif. (announced in November 2024); and the $420 million Phillip A. Levy Engineering Center at the University of Wisconsin in Madison, Wis., now underway.

Final thoughts

Although we may see a softer construction market in 2026 still dominated by data centers, there still appears to be a healthy flow of small and mid-sized projects valued at $100 million to $250 million entering the pipeline. When you consider that electrical work accounts for no less than 10% of the typical construction project, there will still be good money to be made next year for electrical contractors and other electrical professionals in select construction niches.

Retrofit work in existing commercial buildings should provide some solid business opportunities, and the news from the lighting market is that the first generation of LED lighting systems that were installed a decade or more ago are aging and will need to be replaced over the next few years with the latest LED and control technology.

Business conditions in the electrical construction industry typically vary widely by local geographic market and individual construction niche. However, on a national basis, it seems like growth in the low single digits for the U.S. electrical construction market is a pretty safe if unspectacular bet.

About the Author

Jim Lucy

Editor-in-Chief, Electrical Wholesaling & Electrical Marketing

Over the past 40-plus years, hundreds of Jim’s articles have been published in Electrical Wholesaling, Electrical Marketing newsletter and Electrical Construction & Maintenance magazine on topics such as electric vehicles, solar and wind development, energy-efficient lighting and local market economics. In addition to his published work, Jim regularly gives presentations on these topics to C-suite executives, industry groups and investment analysts.

He launched a new subscription-based data product for Electrical Marketing that offers electrical sales potential estimates and related market data for more than 300 metropolitan areas. In 1999, he published his first book, “The Electrical Marketer’s Survival Guide” for electrical industry executives looking for an overview of key market trends.

While managing Electrical Wholesaling’s editorial operations, Jim and the publication’s staff won several Jesse H. Neal awards for editorial excellence, the highest honor in the business press, and numerous national and regional awards from the American Society of Business Press Editors. He has a master’s degree in communications and a bachelor’s degree in journalism from Glassboro State College, Glassboro, N.J. (now Rowan University) and studied electrical design at New York University and graphic design at the School for Visual Arts.