Data Centers Continue to Dominate Construction Pipeline

Key Takeaways

- Construction starts increased by 12.8% in March, with nonbuilding and data center projects leading the growth.

- Residential starts declined 7.2% year-to-date, with single-family homes decreasing but multi-family projects expanding.

- Nonresidential building starts grew by 6.3%, though commercial office and warehouse projects experienced month-to-month declines.

Dodge Construction Network’s two most recent reports on construction activity highlighted the sluggish nature of the overall construction market but pointed to the overwhelming strength of the data center market.

Dodge said total construction starts rose 12.8% in March to a seasonally adjusted annual rate of $1.2 trillion. Nonresidential building starts grew by 6.3%; residential starts improved 2.6%; and nonbuilding starts rebounded 37.9% over the month. On a year-to-date basis, total construction starts were down 0.5% through March. Nonresidential starts were down 0.2%; residential starts were down 7.2%; and nonbuilding starts improved by 6.4% over the same period. For the 12 months ending March 2026, total construction starts were up 5.4% from the 12 months ending March 2025. Residential starts were down 5.3%; nonresidential starts were up 6.5%; and nonbuilding was up 15.8%.

“A few strong categories overcame slight weakness in all the others in March,” said Eric Gaus, chief economist of Dodge Construction Network, in the press release. “The commercial segment shows the most strength with 12-month growth for all sub-categories except warehousing.”

Nonresidential sector

Nonresidential building starts improved 6.3% in March to a seasonally adjusted annual rate of $466 billion. Commercial starts were down 9.2%, mostly driven by the month-to-month (m/m) pullback (-16%) in offices and data centers. Warehouses (-6.6% m/m) also lost ground in March. Hotels (+19.3% m/m) and stores (+5.6% m/m) saw nice gains. Parking garages also showed a small gain (+0.8% m/m).

Institutional starts contracted 1.5% over the month, despite growth in education (+3.4% m/m) and health care (+9.7%). Other institutional categories more than offset that growth, dropping 11.8% m/m. After a lackluster February, manufacturing construction also bounced back, increasing by 251.9% m/m. On a year-to-date basis through March, nonresidential starts are down 0.2%. Commercial and industrial construction gained (+18%), while institutional starts were down (-17.8%) over the same period.

For the 12 months ending March 2026, total nonresidential starts were up 6.5% compared to the 12 months ending March 2025. Commercial starts were up 19.2%, institutional starts decreased 5.7%, and manufacturing starts were up 20.2% over the same period.

Residential sector

Residential building starts grew by 2.6% in March to a seasonally adjusted annual rate of $385 billion. Single-family starts decreased 5.3% m/m, and multi-family starts expanded by 15.3% m/m. On a year-to-date basis, residential starts are down 7.2%, with single-family starts down 14.1% and multi-family starts up 6.1%.

For the 12 months ending March 2026, total residential starts fell 5.3%. Single-family starts fell 15.7% compared to the 12 months ending March 2025, and multi-family starts increased 16.3% over the same period.

The Dodge Momentum Index (DMI), which measures the three-month moving value of nonresidential building projects going into planning and is shown to lead construction spending for nonresidential buildings by a full year to 18 months, increased 1.8% in March to 250.5 (2000=100) from the downwardly revised February reading of 246.2 points. Over the month, commercial planning grew 7%, and institutional planning momentum declined 8.8%.

“Planning momentum in March was powered almost entirely by data center projects, with most other sectors easing back,” said Sarah Martin, associate director of forecasting at Dodge Construction Network. “For some categories, this reflects a natural reset after the outsized growth in late 2025. But for others, elevated macroeconomic risks are likely beginning to feed into planning decisions.”

On the commercial side, planning momentum slowed across all commercial sectors apart from data centers. Institutional planning saw widespread weakness, with only education and public buildings moderately gaining traction. Despite recent declines, the DMI remains elevated. The DMI was up 25.8% YOY when compared to March 2025. The commercial segment was up 28.5% (-12.7% when data centers are removed), and the institutional segment was up 19.6% over the same period.

A total of 54 projects valued at $100 million or more entered planning throughout February. The largest of those projects included 17 individual buildings, each valued at $500 million, for the Amazon Data Center Campus in Hamlet, N.C. Similarly, 10 individual buildings, each valued at $250 million, entered planning in relation to the Microsoft Data Center DSM50 project in Dallas, Iowa. The largest institutional construction projects were the $245-million MCLJ Outpatient Pavilion in San Diego, Calif.; the $183-million Orlando Health Viera Hospital (Phase 1B) in Viera West, Fla.; and the $175-million Bachelor Enlisted Quarters renovation project at Camp Pendleton North in San Diego, Calif.

Nonbuilding sector

Nonbuilding construction starts jumped 37.9% in March to a seasonally adjusted annual rate of $369 billion. Three mega-projects continued the flip-flopping streak in the electric power/utilities segment, which popped up 353.6% m/m in March. Miscellaneous nonbuilding increased as well, rising 44% over the month. Conversely, highways and bridges (-13.6% m/m) and environmental public works (-4.1% m/m) reversed gains from the previous month. On a year-to-date basis through March, nonbuilding construction was up 6.4% alongside the year-to-date growth in electric power/utilities (+68.6%). The remaining public works sectors, however, are seeing deeper year-to-date declines.

For the 12 months ending March 2026, total nonbuilding starts were up 15.8%. Environmental public works fell by 6.4% compared to the 12 months ending March 2025. Highway and bridge starts were down 1%; miscellaneous nonbuilding starts were up 34.9%; and utility/gas starts increased 52.3% over the same period.

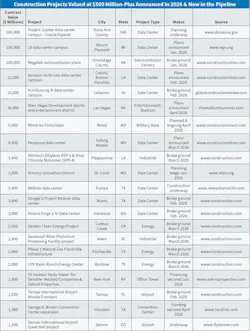

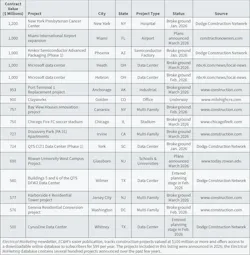

Trophy Jobs Continue to Break Ground

These mega-billion-dollar projects are now in the pipeline and should drive building activity for months to come.

Although the overall construction climate isn’t too inspiring right now in many cities and regions of the country, there always seem to be a few new mega-projects to capture the imagination of construction professionals.

Data center campuses continue to increase in scale, led by the plans of Oracle and OpenAI to build the $16.5-billion Project Jupiter data center campus in southern New Mexico and Microsoft’s January 2026 proposal for a $13-billion campus that would include 15 data centers in Mount Pleasant, Wis.; Amazon’s February 2026 announcement for a $12-billion multi-site data center campus in Caddo and Bossier Parishes, La; a $10-billion Meta data center campus in Lebanon, Ind; and Penzance’s plans announced this month for a $4-billion data center in Falling Waters, W.Va. In the Table on pages 18 and 20, 14 of the projects valued at $500 million or more are data centers, which is a pretty solid indicator that they will continue to dominate the construction market in the near future.

Other projects that made news over the past few months include the $10-billion Starr Vegas Development sports and entertainment district on the drawing boards for downtown Las Vegas; the $5-billion in planned and on-going construction at the Minot Air Force Base in Minot, N.D.; the $1-billion expansion of Miami International Airport; a $750-million soccer stadium for the Chicago Fire FC soccer team in Chicago; and Rowan University’s innovative $690-million West Campus Development Project in Glassboro, N.J. The project includes an integrated district for health and manufacturing innovation that would tap into the school’s focus on health care and advanced manufacturing. Features of the project include multi- and single- family housing, a retirement community, a hotel and conference center, medical offices, and a manufacturing center that would include R&D labs, a virtual reality center, and manufacturing space for private companies.

Another large project that made headlines is the new American Express headquarters planned for part of the old World Trade Center site in lower Manhattan (see Photo on page 16). While the company did not release the project’s total contract value, it will easily be one of the largest office projects in the nation. The 55-story office tower will be 1,226-ft tall and include 2 million square feet of space. The company said the building’s capacity would be up to 10,000 workers and is expected to be completed by 2031.

Arizona State University also has plans for two interesting projects — the $187-million John S. McCain III Library and Museum, which had a ceremonial groundbreaking on the university’s Tempe, AZ, campus in January, and the $200-million Arizona State University Health Building, expected to start construction in July 2026, approximately 12.6 miles west of nearby downtown Phoenix.

About the Author

Jim Lucy

Editor-in-Chief, Electrical Wholesaling & Electrical Marketing

Over the past 40-plus years, hundreds of Jim’s articles have been published in Electrical Wholesaling, Electrical Marketing newsletter and Electrical Construction & Maintenance magazine on topics such as electric vehicles, solar and wind development, energy-efficient lighting and local market economics. In addition to his published work, Jim regularly gives presentations on these topics to C-suite executives, industry groups and investment analysts.

He launched a new subscription-based data product for Electrical Marketing that offers electrical sales potential estimates and related market data for more than 300 metropolitan areas. In 1999, he published his first book, “The Electrical Marketer’s Survival Guide” for electrical industry executives looking for an overview of key market trends.

While managing Electrical Wholesaling’s editorial operations, Jim and the publication’s staff won several Jesse H. Neal awards for editorial excellence, the highest honor in the business press, and numerous national and regional awards from the American Society of Business Press Editors. He has a master’s degree in communications and a bachelor’s degree in journalism from Glassboro State College, Glassboro, N.J. (now Rowan University) and studied electrical design at New York University and graphic design at the School for Visual Arts.