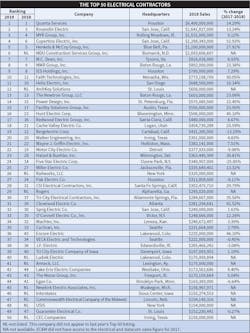

Business Booms, Uncertainty Looms: EC&M's 2019 Top 50 Electrical Contractors Special Report

Scrambling to meet growing demand in a strong construction economy while also retooling operations to reflect a changing industry, electrical contractors are faced with a challenge akin to changing a tire on a moving vehicle. They must keep their eyes on the busy road in front of them but also make sure their businesses are ready for the long haul and changing road conditions.

“Construction is following in the footsteps of industrialization,” says Clay Scharff, president and CEO of ArchKey Solutions (No. 12), a St. Louis-based electrical contractor formed in 2018 to bring together two operating subsidiaries for greater synergy, collaboration, and customer responsiveness (St. Louis-based Sachs Electric and Minneapolis-based Parsons Electric). “It’s been slow to come and talked about for years, but now the pain is great enough to force a change. Industry data tells us the size and complexity of projects are growing exponentially, while our industry is not (keeping pace).”

Since the 1930s, Sachs Electric has been the preferred electrical contractor for the St. Louis Cardinals, and for almost two decades Parsons Technologies has facilitated A/V event support and system maintenance at Busch Stadium. Both Sachs and Parsons are ArchKey Solutions Companies.

Miller Electric Co. (No. 25), Jacksonville, Fla., also sees pressure growing for electrical contractors to adapt to an evolving construction industry.

“Our industry has a reputation of being slow to adopt new technologies, but that’s changing over time as the world becomes more digital,” says Kyle Hensley, chief financial officer, adding that the company now has an executive solely responsible for guiding Miller’s digital transformation.

CSI Electrical Contractors partnered with DPR Construction to provide electrical construction to Behr Paint headquarters in Santa Ana, Calif. The team renovated this three-story building, including a new gym, an indoor-outdoor space, offices, and more.

At Sprig Electric (No. 32), San Jose, Calif., eyes are on the horizon, trying to assess how a changing electrical infrastructure could ultimately impact traditional electrical contractors in the future.

One of the company’s long-term challenges, says President and Chief Information Officer Mark Mandarelli, is “managing the [impact of the] industry’s transition to low-voltage applications for what was traditionally electrical work. ‘Smart’ buildings with many more digital devices incorporated will affect how a building operates and how things are designed, installed, and managed.”

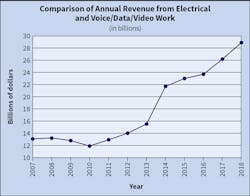

In the meantime, current business for all three demands attention and continues to be strong, as it does for most of the electrical contractors on this year’s annual listing of the top firms ranked by revenue — the EC&M 2019 Top 50. ArchKey, Miller (No. 25), and Sprig (No. 32) contributed to a 2018 electrical and voice/data/video work revenue number that totaled a (current dollar) record $28.8 billion for all 50 firms combined on this year’s list (Fig. 1). That was 10% higher than prior-year revenues for last year’s Top 50 ($26.2 billion) and more than 20% above the 2017 Top 50’s $23.8 billion.

Revenue for the EC&M Top 50 began surging in 2014 as the hangover from the financial crisis abated and has grown steadily since. Today, many contractors find themselves happily swarmed with business as virtually all types of construction are being lifted by generally favorable economic trends, including low interest rates, rising real estate values, low unemployment, and relatively strong consumer spending and business investment. Of the 39 firms that were in both the 2018 and 2019 Top 50 rankings, only eight reported revenue decreases in 2018, several of which were just fractional declines.

Wayne J. Griffin Electric completed this electrical/telecommunications installation at the new 368,000-sq-ft Sanford High School and Regional Technical Center, Maine’s largest public school project.

Worries persist, however, that the nation’s long economic recovery may be running on fumes, and that slowing growth or even a recession is looming. That would surely reverberate in the construction economy and ultimately dent contractors of all types. For now, though, business is seemingly good in the electrical contractor space, and most are trying to squeeze as much out of the good times as they can — leaving worries about what the future may hold in terms of demand for their services, at least, on the back burner.

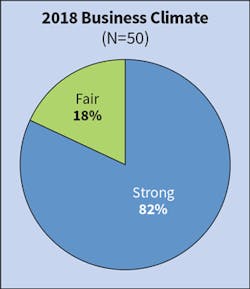

Optimism Not Shaken

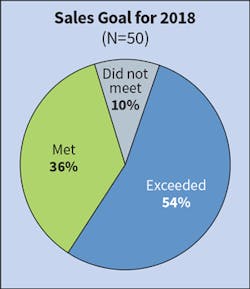

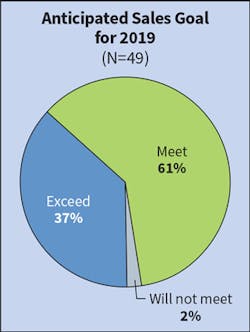

Overall, contractor optimism is evident in the results of EC&M’s annual Top 50 survey. Assessing the overall business climate, more than three-quarters of respondents said it was strong, mirroring the response from last year’s Top 50 (Fig. 2). But there was a notable move upward in the number reporting performance surprises. More than half said they surpassed their sales goal, whereas 47% of the 2018 Top 50 reported doing so (Fig. 3). Cautious once again, however, only about one-third said they expected this year’s sales to top their goals (Fig. 4).

continue to characterize their

businessclimate as “strong.” In

2018, that number rose to 82%.

companies that exceeded revenue

expectations increased by seven

percentage points from last year.

firms (37%) this year than

last year (35%) indicated

they would “exceed”

revenue expectations for

the current year.

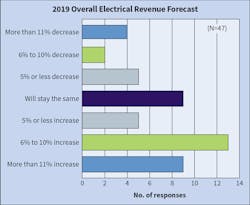

At the same time, almost half say they see their 2019 revenues increasing respectably, at least 6%, with a fair subset saying double-digit increases aren’t out of the question (Fig. 5). Last year, about one-third forecast 2018 revenues of 6% or more, so spirits may be higher.

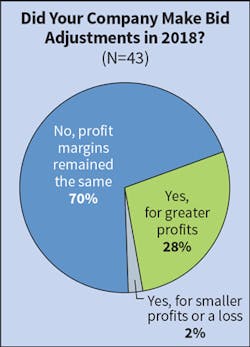

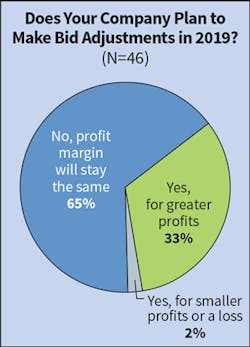

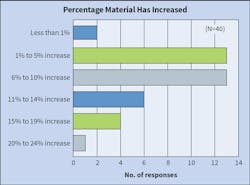

A sign that business is indeed good — and that mounting demand is producing a textbook economic response — is that the profit picture may be improving as well. Whereas 20% of last year’s Top 50 said they had made bid adjustments for slightly greater profits, the figure jumped to 28% this year (Fig. 6). More revealing is that almost one-third of firms on the current list said they’d adjust for higher profit this year, up from just nine of the 50 ranked firms last year (Fig. 7). Almost all said adjustments would be in the low single-digits, but profits could come under pressure if inflation heats up. It’s been mute in the economy overall, but contractors indicate prices of key materials they need continue to tick up (Fig. 8 and Fig. 9).

on the Top 50 list realized about the

same profit margins as they did the

prior year. Of those that adjusted bids

for greater profits, 95% fell within the

0% to 5% range.

on whether they expect profit margins

to increase or stay the same this year.

Of those companies that did adjust

their bids for greater profits, 100% fell

within the 0% to 5% increase range.

Fig. 9. “Distribution equipment” replaced “wire and cable” this year as the material type experiencing the greatest increase in price overall.

Victor Salerno, CEO of O’Connell Electric Company, Inc. (No. 33), Victor, N.Y., says rising tariffs on Chinese-made products are a concern. The impact has been limited so far, though the company did have a problem securing electrical components for a bridge project recently.

The Marriott CityPlace Hotel at Springwood is located at the Springwoods Village Community north of Houston. Completed in September 2018, under the GC Austin Commercial, Walker was contracted to perform all electrical installations as well as security and video surveillance systems.

At Miller Electric, revenue grew 13% in 2018 to $336 million, a result of sustained increases in capital spending in its core health care and data center markets, as well as the signing of more long-term service and maintenance contracts, many related to potential natural disaster recovery scenarios, Hensley says. Picking its spots carefully, the firm has seen steady top-line growth over the last few years and the emergence of some higher-margin opportunities.

“We try to focus on market verticals where we can provide some value differentiation, such as downtime reduction in service disruptions and in areas where the customer is willing to pay for a higher level of quality, not situations where we always try to be the low bidder,” says Hensley.

Growing revenue 53% to $1.3 billion, Cupertino Electric, Inc., (No. 4), San Jose, Calif., logged the largest top-line increase, benefitting from more demand in its core markets and continued success in expanding geographically through more project partnerships — chiefly data centers — with other electrical contractors.

During its construction, the Gaylord Rockies Resort was the largest non-casino hotel being built in the United States and included 15 floors with nine restaurants, a lazy river, spa, pool atrium, and a train caboose. Encore Electric provided comprehensive design-assist services and installation of power, lighting, and life-safety systems to the 1 million-sq-ft hotel as well as its 30 acres of remaining outdoor space around the hotel.

“Two years ago, data center work was worth $100 million, and now we’re at $400 million annually,” says Tom Schott, president and CEO. “That work has given us more of a national presence, and our utility division is getting more business as utility-scale renewable energy projects advance.”

Looking ahead, Schott says the coast looks clear for more revenue gains through at least 2020 because of its favorable market positioning, but that Cupertino must “be prepared to react and adjust” to changing market conditions. That will mean building up a presence in areas that could rise when commercial spending declines, such as public infrastructure work and airports.

USIS panels built custom for each apartment in the company’s 60,000-square-foot pre-fab shop. All circuits are labeled and cut to exact length, ready for delivery.

With demand looking firm in markets like education, manufacturing, and power/transmission and distribution, O’Connell continues to make investments to support growth. Salerno says the company has expanded its headquarters and sunk $7 million into new T&D infrastructure service vehicles in anticipation of bumping revenue up 20% this year, on the heels of a 12% gain to $250 million in 2018.

“There’s a lot going on in the power sector, especially with new substations being built and more alternative energy-related work such as battery storage,” he says. “We’re getting some huge projects, and we’ve been bidding aggressively to take on more.”

Top Markets Steady

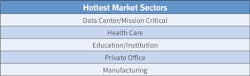

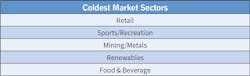

While the power/T&D market looks attractive for companies like O’Connell and Cupertino, bigger opportunities for contractor revenue growth may lie elsewhere near term. Despite signs of a resurgent dynamism, power/utilities/T&D did slip out of the top five “hottest market sectors” for companies in 2018, its slot taken by manufacturing (Table 1). Data centers/mission critical and health care again got the most mentions, reflective of broader national expenditure and infrastructure investment trends. But markets are always changing and evolving, and electrical contractors must remain nimble. Some, too, are highly specialized or regionalized, leaving them out of bounds for some but critical for others. One case in point is health care: It also ranked high on the roster of 2018’s “slowest” markets (Table 2).

Table 1. For the third year in a row, data center/mission critical construction and health care stayed on top as markets bringing in the greatest dollar volume of projects in 2018.

Table 2. Again this year, retail topped the list as the slowest market among Top 50 respondents.

Nevertheless, it was a key market for Encore Electric, Inc. (No. 36), Lakewood, Colo., whose revenue bolted ahead 46% in 2018. Chairman and president Willis Wiedel says the firm isn’t limiting itself in terms of scope but has been careful to have the resources in place to handle whatever it takes on. “Health care and data center work were a big part of that growth, but institutional generally has been busy, along with resort hotel work, a hotel project at the Denver airport, and some recent college stadium projects,” he says.

Some contractors continue to mine opportunities in more growth-challenged sectors. Rogers (No. 29), Alpharetta, Ga., has long had a stake in the retail market, and despite the declining share of brick-and-mortar stores, the sector is still an important one, says Ayla Tribble, marketing manager.

“We’ve been predicting some changes there, but now what we’re seeing is opportunity in transforming them to more experiential spaces, which falls in line with electrical services,” she says. “Retail is becoming similar to the restaurant and entertainment space.”

With a position as one of the industry’s leading self-permitting lighting contractors, Tribble says Rogers remains well positioned to serve those markets as they evolve and incorporate new illumination schemes.

Determined not to be caught flat-footed if the economic backdrop changes, ArchKey is assessing market conditions and trying to plan for any disruption, Scharff says. That means studying emerging markets for electrical services as well as pursuing abundant current opportunity in sectors like mission critical, industrial, renewables, technology, and health care.

This multi-building development with special lighting packages and EV charging stations by Cupertino Electric, Inc., is a biotech hub located in South San Francisco.

“We see demand in certain markets continuing to be strong through next year, while others may have reached their peak,” he says. “We take a proactive approach in researching new markets. Our goal is to be balanced and diversified, and that requires a consistent business development effort.”

Worker Worries

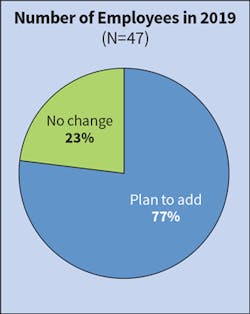

While opportunities abound for contractors, so do challenges in assembling the assets needed to get jobs done and meet external/internal expectations. Nowhere is that challenge more prevalent than in the area of labor. Contractors again say, definitively, that finding and keeping employees is their top business challenge, that their need for labor is strong, and that they remain solidly in hiring mode.

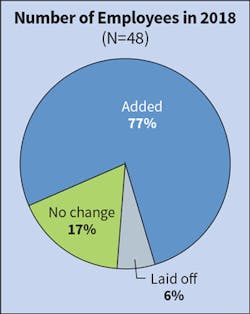

Fig. 10. The number of Top 50

firms adding headcount last year

held strong at 77%.

Fig. 11. As has been the case for

the last several years, the vast

majority of Top 50 firms expect to

add workers in 2019 or maintain

headcount levels.

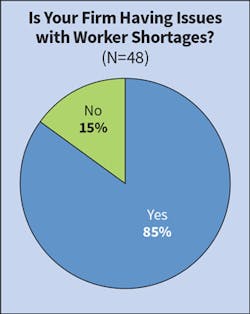

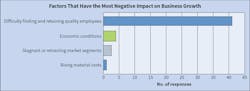

A firm three-quarters of contractors say they hired more workers last year and planned to again in 2019 (Fig. 10 and Fig. 11). But in a period of strong growth, they seemingly can’t get out in front of it; 41 companies said they were having “issues” with worker shortages, a number that’s 25% higher than two years ago (Fig. 12). The issue, it seems, relates unsurprisingly to the ability to seize opportunities and grow the business. Eighty-five percent of companies said difficulty finding/retaining good employees was the single biggest barrier to growth (Fig. 13).

Fig. 12. Again this year, the

overwhelming majority of Top 50

companies (85%) indicated they were

experiencing worker shortages.

Fig. 13. Again this year, the most obvious deterrent from business growth among Top 50 firms relates to staffing challenges.

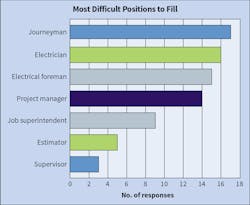

One sign labor woes might be abating some is that hiring trouble spots may be less diffuse. Contractors queried two years ago were much quicker to identify a broader collection of seven named positions as “difficult to fill”; on average each got 16 separate mentions. This year, each one got 11, on average. The problem area, though, remains clustered in four roles: journeyman, electrician, foreman, and project manager (Fig. 14).

Fig. 14. “Journeyman” replaced “project manager” as the hardest position to fill this year, according to Top 50 respondents.

Houston-based Quanta Services, (No. 1), upped its revenue 14% in 2018 despite labor force issues it’s been trying to ameliorate.

“We have constraints in the labor force, especially when it comes to specialty skilled labor,” says Earl (Duke) Austin, president and CEO. “We’ve invested in training over the last five-plus years to mitigate these concerns.”

On the Shell Deer Park Olefins Flare Gas Recovery Project, MMR installed 20,230 feet of conduit, 90,940 feet of electrical cable, 9,800 cable terminations, and 160 luminaires.

Part of the industry-wide solution, he says, is to start filling the pipeline with young people keen to become skilled laborers. The goal should be a more diverse workforce, put on an apprenticeship path and regularly trained after hiring.

At Sprig, the bigger need is in the staff required to win projects and keep them on track. Project managers and engineers and estimators are in shorter supply, and that’s making productivity a key concern.

“We’re all very busy, and we’re at the point where we don’t have a number to call for even bad help,” Mandarelli says. “We have to position ourselves to do what we can with what we have, but we’re investing heavily in doing that.”

ArchKey Solutions companies Parsons Electric and Sachs Electric were awarded a series of projects at the Marathon Mandan refinery in 2018 and continue to provide a full range of electrical, civil, instrumentation, technologies, and testing services.

Encore has been hard pressed to find journeymen to deploy, but equally worrisome in a period of growth is finding strong management. Its portfolio of more “complex” and increasingly larger projects, Wiedel says, adds to the pressure to deploy the talent needed to understand project nuances and shepherd resources effectively.

“Another round of 40% growth would be difficult because of the need for strong supervision, given the diversity of the work we take on,” he says. “That’s the most important factor for us today.”

Managing a Transition

The ability to manage and perform jobs well, though, comes with experience, something electrical contractors are sure to lose over time as a wave of Baby Boomer retirements builds. Add in the fact that the industry is finding it harder to recruit younger people into many key jobs, and it becomes clear contractors could face a future labor squeeze that will demand productivity enhancement achieved through a mix of training, mentoring, guidance, best practices development, and technology deployment.

The Limestone to Gibbons Creek transmission line project consisted of 68 miles of 345kV double-circuit transmission line and 1,400 structures in the Texas counties of Limestone, Leon, Madison, and Grimes. The L.E. Myers Co. provided construction management, material procurement, and construction services, including right-of-way clearing, environmental controls, foundation installation, structure assembly, and erection and conductor stringing.

Contemplating that, Top 50 contractors indicate they’re using the entire toolbox to address the specific challenge of bridging the knowledge and experience gap between veterans edging out the door and new recruits coming in. On-the-job training is by far the most popular tactic of seven listed, suggesting that in a busy period new hires must hit the ground running. But six others got a fair number of mentions as ones being used, each drawing more than last year. In total, contractors responding checked the boxes 125 times; last year the seven tactics drew 53 checks in all (Fig. 15).

Fig. 15. To combat the current state of skilled labor shortages in the industry, Top 50 firms overwhelming cited “on-the-job training and shadowing” as their No. 1 method of transferring knowledge between veteran workers and their newly hired counterparts, but many other strategies are at work as well.

Knowledge transfer is increasingly important, but also trickier today because the business is changing, says Cupertino’s Schott.

“The way projects are managed and built today is very different from even five years ago,” he says. “Transferring experience gained from years of experience is key, along with making sure we’re translating those lessons in a way that resonates with young people and applies to what we’re seeing today.”

Five Star is currently performing over $800 million of electrical work on the East Side Access project, which will provide access for trains from Long Island and Queens to the east side of Manhattan and the new concourse below Grand Central Terminal. The East Side Access megaproject is one of the largest transportation infrastructure projects currently underway in the United States.

Training and development at Miller are being formalized and broadened. In a new role, a chief learning officer will focus on training content and methodology, and one focus will be on developing increasingly valuable “soft skills,” Hensley says.

“Electrical engineering or a similar educational background used to be the path to project manager, but the new vision is for someone, regardless of education, to go from zero to Miller-quality project manager over five to seven years,” he says.

Leveraging Technology

Advances in information technology are making such on-the-job learning approaches more viable, as is the fact that electrical work is changing. Entirely new areas of expertise and skill are emerging, and much of it is absorbed in that fashion. But formalized training also remains critical, and contractors are making that a core part of their employee retention, quality control, and productivity enhancement regimen. Whatever the mode, contractors see some workforce training gaps that need filling in with electrical fundamentals, new technology tools, and project elements seeing more demand (Fig. 16).

Fig. 16. Again this year, Top 50 respondents named the “NEC” and “field software” as the most common topics their employees need training support on.

With “smart” buildings in demand, Mandarelli says Sprig teams will inevitably need advanced training in how connectivity and control elements are designed and deployed in those spaces. More broadly, training across the board is bound to become more central.

“Our investment is as big as ever,” he says. “The goal is to be as operationally efficient as possible and that means educating everyone on tools and processes.”

Lighting with integrated controls is installed at the executive offices of Aruba, Santa Clara, Calif. Sprig Electric performed follow-on lighting work after the core and shell electrical infrastructure installation.

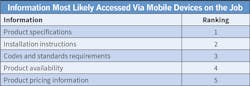

Technology adoption (software and hardware alike) could be an important change agent in the future training and project delivery equation for contractors. The mobile device and app revolution has put more powerful IT in the hands of all workers, boosting productivity, reducing costly errors, and improving communication. Contractors say software/apps workers use in the field are making many historically time-consuming tasks more manageable, enabling better overall project management, a key to profitability (Fig. 17). From accessing product details to installation guidelines to codes and standards particulars, mobile devices are becoming the speedy conduit for essential information crews need to keep jobs moving (Fig. 18).

Fig. 17. More Top 50 respondents indicated their employees use project management and time management tools than any other types of digital programs.

Fig. 18. Top 50 respondents indicated their employees are accessing product specifications, installation instructions, and codes and standards requirements most frequently in the field.

Last year, Cupertino deployed an app for worker safety-related observations in the field. The SmartTagIT product, Schott says, allows the company to drill down into an issue that impacts worker well-being, cost control, and productivity. Safety-incident reporting is now more timely, transparent, and accessible, he says, opening the door to improved prediction and prevention of incidents.

This four-building Academy Square commercial office project in Los Angeles is built above an underground parking structure and includes electrical and low-voltage work performed by Cupertino Electric, Inc.

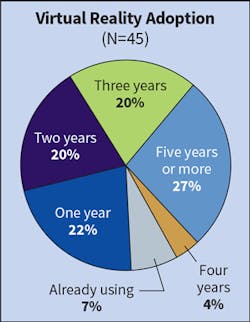

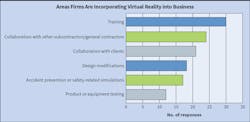

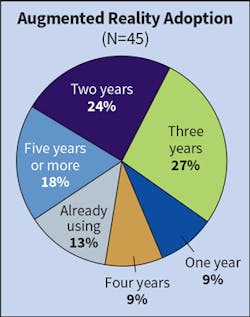

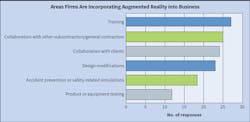

One of technology’s most promising contributions to future construction efficiency improvement is in the area of enhanced project analysis. Augmented reality (AR) technology that integrates detailed project drawings and data into real-time project work via visualization devices, and virtual reality (VR) technology that creates a completely simulated environment, enabling enhanced experimentation and collaboration, may have wide applications in construction. And it appears they’re on more electrical contractors’ radar. The bulk of contractors say that, at best, they’re both a few years away from impacting electrical construction work, but a handful claim to be using the technologies now. Contractors see a range of potential applications for AR and VR, with training topping the list (Fig. 19, Fig. 20, Fig. 21 and Fig. 22).

Fig. 19. More than 60% of

Top 50 firms are either already

using virtual reality technology

or see it as a viable component

of their electrical work in the

next three years. On the other

hand, nearly 30% don’t see it

materializing until five years

or more.

Fig. 20. These are the top six areas in which Top 50 respondents see their firms incorporating virtual reality technology into the business in the next few years.

Fig. 21. Nearly three-fourths of

Top 50 firms are either already

using augmented reality

technology or see it as a viable

component of their electrical

work in the next three years.

Fig. 22. These are the top six areas in which Top 50 respondents see their firms incorporating augmented reality technology into the business in the next few years.

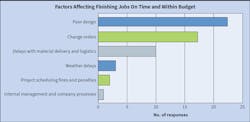

Both also hold the promise of streamlining the entire construction project design process, one that — along with change orders — contractors finger as the biggest source of problems that produce project delays and cost overruns. The three listed likely causes of those delay and cost issues were marked 49 times by this year’s Top 50; last year the number was 38 (Fig. 23).

Fig. 23. The majority of Top 50 firms consider “poor design” or “change orders” as having the greatest impact on their company’s ability to get a job done on time and within budget.

Design flaws are not a new problem, says Wiedel, but they’re growing more consequential as construction schedules are compressed. “Trying to design and build things too quickly is a recipe for disaster,” he adds.

But that’s part of the predicament not a few electrical contractors find themselves in today as the nation’s infrastructure is built out, upgraded, and hardened in what’s amounting to a sustained period of freewheeling investment. Continued growth has been welcomed by contractors, and a potential slowdown is worrisome, but a bulging pipeline of work also magnifies many of the challenges they face in positioning their businesses for a future that is sure to look different from the past and the present.

O’Connell Electric crews watch as a 2.5MW generator is rigged onto a 10,000-gallon diesel tank at a Verizon data center in Rochester, N.Y. It’s one of a pair backing up a new 480V, 4,000A double-ended service feeding the facility.

Citing the human resources quality and availability issue that so many contractors lament, Scharff says the future will belong to companies that can adapt.

“Contractors are being forced to change the way they build, and those that embrace the change, lead through it, and transform their business will do well,” he says.

Zind is a freelance writer based in Lees Summit, Mo. He can be reached at [email protected].

Sidebar: What Keeps Electrical Contractors Up at Night

Challenge is ever-present in business, and it’s always fashionable for participants to say their time in history is the most challenging. That may or may not be true now, but electrical contractors in EC&M’s 2019 Top 50 aren’t shy about sharing their thoughts on the most pressing challenges of the day.

As in years past, labor availability and quality received many mentions when contractors were queried about the greatest business challenge they face in the next few years. But there were others, too. Here’s a sampling of a few telling verbatim responses:

• Implementing technology into the building process to increase productivity.

• Adjusting to market conditions.

• The good economy has attracted “outlier” companies into our marketplace.

• We see more opportunities for increased prefabrication, but it will be hard to get people to identify it.

• We believe the entire construction industry will be facing the next recession in the coming year to 18 months. This will create challenges on many levels for owners, GCs, and specialty contracting.

• Non-union infiltration into the marketplace. The amount of work available to union contractors is reducing, and prices are being forced downward.

• Demand for housing, mortgage rates, and material costs.

• Continuing to increase our capacity to shift and grow with emerging technologies and other global and industry changes.

• Tariffs.

• Economic and political issues affecting the amount of work. Also, overall market cycle nearing a downturn. If the market stays flat or improves, the shortage of talented labor will continue to be an issue.

• Being selective about the projects we take on is an important factor in this economy. Choosing to work with reputable customers that pay on time and bidding projects that have enough margin built into our price is important.

About the Author

Tom Zind

Freelance Writer

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].