Making Sense of the K-Shaped Economy

Key Takeaways

- The U.S. economy shows signs of modest, single-digit growth in 2026 amid mixed hard and soft data signals.

- Consumer spending remains strong, driven mainly by high-income earners, while confidence levels decline, indicating cautious outlooks for the near future.

- The labor market has rebounded slightly, but revisions and sluggish hiring suggest ongoing headwinds for employment growth.

- Sector performance is bifurcated: data center construction surges, while nonresidential and housing sectors face recessionary pressures.

- Companies in the electrical industry should adopt a nimble, strategic approach to capitalize on high-growth sectors and mitigate risks from underperforming areas.

The macroeconomic outlook remains mixed as we enter 2026, partly due to the absence of reliable data stemming from the longest government shut down in history and the disconnect between the messages that hard data (like retails sales, industrial production, capital investment, and jobs) and soft data (like consumer and CEO confidence) are sending right now. As we plan for 2026, an objective assessment is necessary to have realistic expectations for the economy and for growth in the electrical industry in the year ahead. Planning for mild, single-digit macroeconomic growth next year appears to be the prudent thing to do. However, an acknowledgement of the fact that we’re traversing a K-shaped economy — with winning and losing sectors — is equally prudent.

Retail sales and labor market trends

Consumption is the main driver of the U.S. economy, with personal consumption expenditures comprising about two-thirds of gross domestic product (GDP) every year. An effective way to track consumption, which reflects the consumer’s willingness and ability to spend money, is through a data series called “Advance Retail Sales for Retail Trade and Food Services,” published monthly by the U.S. Census Bureau. As of the third quarter of 2025, this series alone represented more than $8.6 trillion of economic activity on an annualized basis.

Despite all the policy uncertainty and geopolitical turmoil witnessed in 2025, retail sales accelerated over the course of the year and were up 4.3% on a cyclical basis (year-over-year) through September (Fig. 1). Initial data for holiday sales, specifically the critical Black Friday through Cyber Monday weekend, is coming in stronger than anticipated. This shows that U.S. consumers, despite feeling gloomy about the economy, kept spending throughout the year, although the bulk of that spending is attributed to high-income earners (more on this later).

The job market rebounded in September, with the U.S. economy adding 119,000 jobs (Fig. 2), bucking the recent trend of weaker job gains since April. Although unemployment ticked up slightly to 4.4%, wages were up 3.8% over the past 12 months, outpacing inflation and helping consumers feel like they can continue to spend money. Unfortunately, revisions to employment data from July and August showed that job gains for the two months were 33,000 lower than previously reported. May and June were also quite weak from a hiring perspective. Objectively, it’s evident that the labor market is noticeably weaker since April, when “Liberation Day” launched a more-aggressive reciprocal tariff regime against America’s trade partners, and companies adopted a wait-and-see mentality regarding their robust hiring plans.

Consumer and business confidence

While the latest available “hard” data for retail sales and job gains was somewhat encouraging, “soft” proprietary data that tracks sentiment and reflects how individuals and businesses think, feel, and talk about the economy was more negative in November (as it was not interrupted by the government shutdown), and has been compared to the hard data for many months. In assessing data series such as U.S. Consumer Confidence and CEO Confidence from the Conference Board, we get a glimpse into the mindset of consumers and businesses, including those in the electrical industry, allowing us to ascertain what their outlook is heading into 2026.

The Consumer Confidence Index (Fig. 3) declined by 6.8 points in November to 88.7, falling to its lowest level since April after moving sideways for several months. The pullback was evident in both the Present Situation Index, which reflects consumers’ assessment of current business and labor market conditions, and the Expectations Index, which portrays consumers’ near-term outlook. Consumers were notably more pessimistic about business conditions six months from now and indicated plans to curb spending, at least to a degree, in the months to come.

The Measure of CEO Confidence (Fig. 4) is a barometer of the health of the U.S. economy from the perspective of U.S. chief executives and gauges CEOs’ expectations about future actions their companies plan to take regarding capital spending, employment, recruiting, and wages. The Index, which has declined precipitously since early 2025, fell to 48.0 in Q4, down one point from 49.0 in Q3. A reading below 50 reflects more negative than positive responses. CEOs’ views of general economic conditions now versus six months ago remained slightly negative, while CEO’s six-month expectations for the economy turned from neutral to pessimistic. This points to persisting headwinds for the industrial economy and, potentially, for the electrical industry as we enter 2026.

Industrial production and capital investment

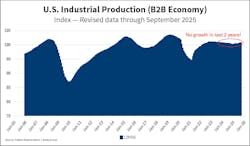

U.S. Industrial Production, a benchmark for the volume of industrial activity/capital spending and a reflection of the B2B economy, is a much better barometer for the electrical industry than consumption or overall job gains. The industrial production business cycle (assessing rates-of-change on a year-over-year basis) closely matches that of the electrical industry, with turns in the cycle and transitions from periods of growth to contraction and vice versa happening on a similar timeline.

A recent annual revision of “U.S. Industrial Production” data from the Federal Reserve Board showed that there has been essentially no growth in the industrial economy over the last two years. In fact, comparing the 12-month moving total values from September 2023 to September 2025 yields growth of -0.002% during this 24-month timespan (Fig. 5). This is a validation of the notable headwinds the electrical sector has faced in recent years. In the last few months, Industrial Production has been slowly accelerating, and currently the short-term (quarter-over-quarter) growth rate stands at 1.3%, while the longer term (year-over-year) growth rate remains a more-anemic 0.4%. However, the upside momentum in the quarterly rate was broken after April’s “Liberation Day” announcement, and the current trajectory of the series, including the latest input from leading indicators, points to sideways movement as the most likely trajectory over the next two quarters.

Capital spending data, represented by a series called “U.S. Nondefense Capital Goods New Orders,” is performing much better. Through September 2025, annual Capital Goods New Orders were up 2.1%. Furthermore, the quarterly growth rate was 4.1%, implying more upside momentum is imminent for the annual growth rate over the next two quarters (Fig. 6). However, as this series is dollar-denominated, whereas Industrial Production is an index, the acceleration in the New Orders data is at least partially reflecting the impact of price increases — and not just organic market growth. In other words, the disparity between the growth rates of the two series in Fig. 5 and Fig. 6 presents clear evidence of inflationary pressure. Heading into 2026, companies in the electrical industry must focus on profitable revenue growth, as inflation will likely continue to accelerate into 2026.

The K-shaped economy

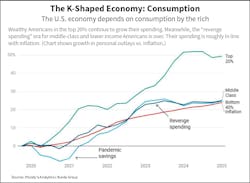

A K-shaped economy describes a bifurcated economic landscape, where different segments of the economy perform at vastly different rates — like the two diverging lines of the letter “K.” In late 2025, examples of a K-shaped economy can be found in both the retail sales-driven consumption sector, which comprises nearly 70% of GDP, and the capital investment-driven construction sector, which is more directly relevant to companies in the electrical industry.

Figure 7 shows that while overall Retail sales are growing at a healthy clip through September, it is the top 20% of income earners that are driving growth, while the middle-class and bottom 40% of income earners are just keeping up with inflation. As shown in Fig. 8, the K-shaped economy is also evident as data center construction is up by $16 billion from the start of 2024, while the rest of nonresidential construction is down by more than $55 billion over the same time frame.

The K-shaped economy highlights an unusually complex period for the electrical industry. Macro-economic growth appears solid, yet hiring is sluggish, and the unemployment rate has ticked up. Overall, consumer spending is still rising, but Americans are less confident. AI-related data center construction is soaring while nonresidential construction and the housing sector are in recession.

This conflicting narrative underscores the need for companies in the electrical industry to remain nimble and to pivot to the outperforming sectors of the market — all while mitigating the downside pressure and risks associated with the underperforming sectors. A proactive strategic approach — one that requires market share gains and new customer acquisition — is the only certain way to ensure company performance meets targets and objectives in 2026.

About the Author

Alex Chausovsky

Director of Analytics and Consulting at the Bundy Group, Alex is a highly experienced market researcher and analyst with more than two decades of expertise across industries such as automation, industrial technology, healthcare, business services and manufacturing. He has consulted and advised companies throughout the U.S. and Canada, Europe, South America, and Asia. Alex has delivered more than 1,000 presentations, webinars, and workshops to small businesses, trade associations, and Fortune 500 companies and is the go-to source of industry data and insights for hundreds of enterprises across a spectrum of industries.