Growth Surge: EC&M's 2018 Top 50 Electrical Contractors Special Report

Amidst what could be one of the most business-friendly environments seen in years, America’s largest electrical contractors appear to be thriving as a group, beneficiaries of growth-oriented tax policies, looser regulation, and a building boom.

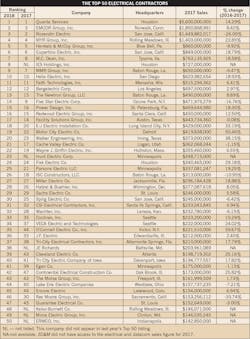

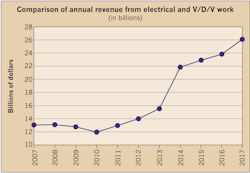

The 50 companies with the highest reported revenue in 2017 brought in a combined $26.2 billion worth of electrical work. Those companies, which comprise EC&M’s annual Top 50 ranking for 2018 in terms of reported prior-year revenues, outdid last year’s collection of key players by $2.4 billion — or 10% above their 2016 revenues of $23.8 billion (Fig. 1).

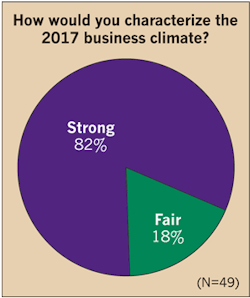

The 2018 Top 50 not only established a new record for non-inflation adjusted income, but also recorded the biggest year-over-year jump in revenues since 2014, when, barreling out of the last recession, the 2015 Top 50 reported a 39% surge. Revenues then basically flatlined until last year. Little wonder, then, that the annual EC&M Top 50 survey, which yields the revenue numbers as well as deep insights into contractors’ business priorities, concerns, challenges, and opportunities, found many respondents upbeat. Eight of 10 companies said the “business climate” was strong (Fig. 2). Look back just two years, though, and the share of contractors seeing a favorable climate was just more than 60%. A year later, seven in 10 of the 2017 Top 50 judged the climate as strong.

What happened to send that number soaring in just two years? Although it’s hard to pinpoint, when revenues continue to surge, a recession isn’t in sight, bottom lines look better because demand is high and some regulatory cost pressures might be easing, and business has government’s ear, what’s not to like?

Hatzel & Buehler, Inc. (No. 28), Wilmington, Del., likes what it sees in terms of the demand trend, and has been working to better position itself to take on more work. Gerard Herr, chief financial officer/VP, says two new offices have been opened in the last three years, and a small contractor was acquired in 2017. At some of the company’s nine branches, management teams are being encouraged to push the envelope.

“We’re equipping senior management with tools they need to achieve improved results, so they can go out and pursue, build, perform, and manage additional work that will generate more revenue,” he says.

In 2017, the company grew revenue 8%, partly the result of expanding demand in health care and industrial markets, Herr says. The company, he says, is on track to grow revenues beyond expectations, and sees a favorable business climate persisting.

“From now through 2020, we don’t really see any slowdown in our business,” he says.

The vice president of J.F. Electric (No. 36), Edwardsville, Ill., sees the good times for his company lasting even longer. Jonathan Fowler says the company’s primary market — transmission & distribution (T&D) work for electric utilities — has the potential to stay strong for another five years. Revenues for the company were flat in 2017, and Fowler sees a repeat in 2018. However, securing steady business with good profit margins is success in his book.

“Our target is to maintain or raise revenues 3% or so this year, but we’re anticipating better growth in 2019 than this year,” he says. “At some point, T&D work will die down, and a lot depends on the course of legislation that allows utilities to recoup costs of building more infrastructure. Work in Illinois seems to be ramping down for us, while work in Missouri is ramping up.”

Moderating expectations

Forecasting growth is fraught with difficulty, especially in the fickle construction and contracting world where business can seemingly dry up or surge on a dime. But over the past several years of EC&M surveys, the Top 50 electrical contractors have been fairly prescient about their own growth, and, by extension, that of the industry. A solid majority have forecast company revenue growth for the ensuing year, and

combined Top 50 growth has followed suit.

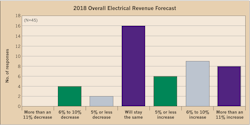

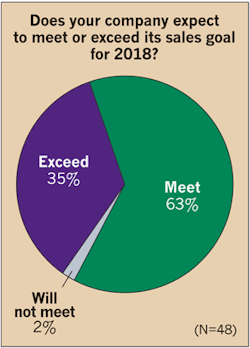

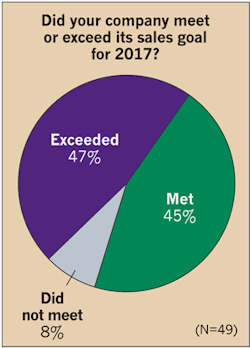

In the latest survey, optimism is again on display, but there’s also a whiff of concern that growth could moderate or even stall. Just over a third predicted their 2018 revenues would stay the same, a number that’s up from 17% last year, and 9% a year earlier (Fig. 3). The share expecting a revenue increase fell to 51%, down from 61% last year and from 63% a year earlier. Contractors also may be getting a bit more conservative when it comes to setting aggressive goals for sales growth. Just over a third said they expected to exceed their sales goal for the coming year, down from 40% in last year’s survey and 46% the year before (Fig. 4). That pullback comes despite numbers showing many electrical contractors indeed topped their sales goal in 2017. Nearly 50% of this year’s Top 50 said sales came in higher than expected, up from the 35% saying so a year earlier, but lower than the 46% of the 2016 Top 50 who said 2015 sales topped estimates (Fig. 5).

At Egan Company (No. 41), Minneapolis, Duane Hendricks, president and CEO, is resigned to slower growth short-term than he may like, following a year when sales were flat. But it’s partly the result of a strategic approach.

“We’re changing strategies a bit on the types of jobs we pursue, making sure the business fits our company,” he says. “Not everything that comes our way is the right thing.”

Egan got a temporary boost from area light rail and sports stadium work in recent years, but that’s over for now. So, by comparison, things now seem slower, Hendricks says. More solar project, multi-family, and education market work has emerged to fill some of that gap, but Hendricks says he’s not expecting much revenue growth this year.

It’s a different story for Cupertino Electric (No. 6), San Jose, Calif. Company revenues grew 19% last year to $850 million, exceeding expectations, and president/CEO Tom Schott sees a chance to crack the $1 billion mark this year, even while maintaining a selective approach to bidding. A specialist in building out data centers, the company is a beneficiary of continued growth in that sector and strong demand from commercial, utility, and renewables customers in California.

“The market outlook is very bullish through 2019, but even with all the shiny things out there to attract our attention, discretion is still important,” he says.

Depending on their orientation and flexibility, strong demand in the electrical services market means contractors can be selective when it comes to projects and market sectors. But opportunities appear to be especially abundant in sectors that have been consistently strong due to continued investment, notably data centers and health care. Like last year’s Top 50 and the group before that, those markets got the most mentions as market sectors expected to be hot in the coming year (Table 1). Markets expected to be the most lackluster included residential and mining/metals, though health care got a high number of mentions as well (Table 2).

Indeed, some degree of specialization still rules the contractor world. For this year’s No. 1 Top 50 contractor, Quanta Services, Inc., Houston, that’s transmission and distribution, a market that by some estimates is growing fast.

“I see constant growth in that sector as we continue to support them in their capital and operational expenditure programs,” says Earl C. Austin, Jr., president and CEO.

At The Newtron Group, L.L.C., (No. 13), Baton Rouge, La., the industrial market is expected to remain strong, says company President John Schempf.

“Cheap and abundant natural gas is driving the chemicals market, and we’re seeing new projects in that area as well as in pulp and paper plants,” he says.

Eye on profit

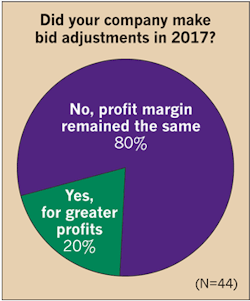

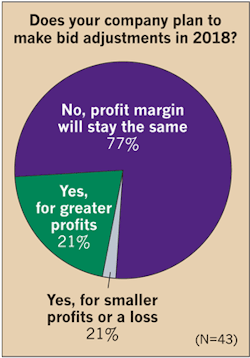

As always, and perhaps even more now when the market is strong, the bottom line is key for contractors. Consistently profitable work is prized, and while that may be more attainable in a seller’s market, contractors also must contend with rising costs, one of which could be labor. For now, though, it appears contractors are either getting the margins they need or are being forced to sit tight. Like last year, only 20% of the Top 50 said they adjusted bids for higher profit in 2017 or were planning to do so in 2018 (Fig. 6 and Fig. 7). Most again said profit margins were generally steady.

Profitable jobs are top-of-mind at Five Star Electric Co. (No. 14), Ozone Park, N.Y., says Vice President/Chief Estimator Russ Lancey. The company has moved away from focusing on revenue and toward looking for big jobs it can execute at enticing margins. The current market conditions are making that more possible than ever.

“We’d rather do one $100-million job than ten $10-million ones, and focus on and better manage that work,” says Lancey. “In a healthy marketplace, the company can be more profitable with less work and without overextending its resources.”

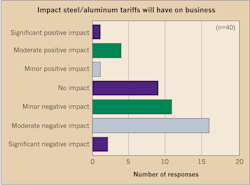

But it all comes down to turning a profit, and that depends partly on controlling costs, something that might get harder if inflation ticks up. When it comes to buying labor and materials, contractors could feel the squeeze if prices begin to rise. Labor costs have been constrained, but prices of commodities like steel and copper, components of materials contractors work with, have been inching up. But they could start to spike because of new tariffs on imported steel and aluminum. Most Top 50 contractors said their businesses stand to be negatively impacted by them (Fig. 8).

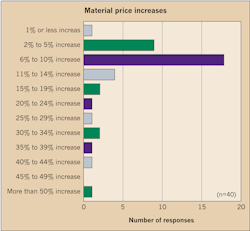

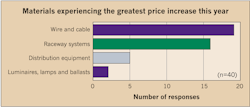

So far, though, contractors say prices on materials they need aren’t rising appreciably. Most who said materials are getting costlier this year said the increase is 10% or less (Fig. 9). But they’re coming primarily on materials contractors work with day in, day out: raceway systems and wire/cable (Fig. 10).

“Those have been increasing over the past few years as metal and copper prices go up,” says Fowler. “That impacts us as we buy materials for commercial and industrial projects, but less so with T&D work where utilities buy it and work out discount deals with suppliers.”

Margins, Fowler says, have been staying steady, but cost increases could eat into profits. If a more contested environment emerges, calculations could change. “We may have to sharpen our pencils and be more competitive.”

Labor worries

That could prove harder, though, especially if labor costs rise, a distinct possibility if the unemployment rate continues to fall and the economy strengthens. That would further complicate a problem that many among the Top 50 say is a persistent problem and their biggest business challenge: finding enough competent and qualified workers to fill jobs that have been coming open at an increasing rate since the economy started to rebound several years ago.

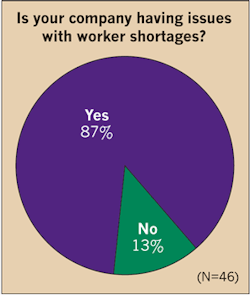

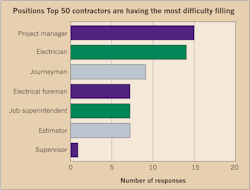

Whether it’s a problem of more openings or difficulty finding candidates, the number of top contractors facing worker shortages has grown. This year, almost nine in 10 indicate they’re “having issues” with shortages (Fig. 11). That’s up from 76% of last year’s grouping and 73% a year earlier. Why the increase? A good bet is that the market is presenting a flood of opportunities that companies must bypass for want of workers. The evidence: Electrician and journeyman have moved up the “most difficult positions to fill” rankings. Those jobs ranked second and third this year, but fourth and fifth last year, and near the bottom two years ago (Fig. 12).

Bobby Lewey, president of IES Holdings, Inc. (No. 8), Houston, says it’s a classic case of demand exceeding supply in the labor market, one complicated by an aging trade workforce and fewer coming in behind those retiring or leaving for other jobs. It’s become more acute for contractors because a robust construction economy is presenting more bidding opportunities.

“Labor costs are probably on the way up, and general contractors and project managers will start to understand they’ll have to address it in pricing,” he says. “One of the things that may happen as we move into this environment is we’ll see more design-build partnering arrangements between subcontractors and general contractors where labor pricing is negotiated and built in.”

Tasked with electrical work on ever more complex and time-constrained data center projects, Cupertino is increasingly challenged to find the specialized labor it needs.

“We’re pulled into a lot of large, fast-track projects that depend on the availability of good, skilled tradespeople who are in shorter supply,” Schott says. “We’ve managed through this the last few years, but it’s an issue that’s building. The war for talent is real.”

One approach, he says, has been to ramp up the hiring of other electrical contractors in areas where Cupertino clients want data centers built. That expands the pool of available labor and minimizes the need to arrange for traveling workers, Schott says.

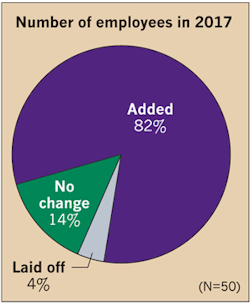

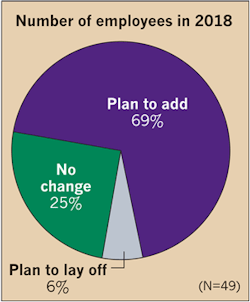

Despite difficulties finding enough workers, the Top 50 have been hiring, and maybe doing more of it than expected. In 2017, 82% added employees, up from 76% that added in 2016 (Fig. 13). Compare that with the 67% of 2017’s Top 50 contractors that anticipated hiring more last year, and signs point to growth that may have surpassed expectations. But in a sign that this group might be expecting growth to taper, 69% said they planned to add employees in 2018, down from 82% that added in 2017 (Fig. 14). It’s clear from the survey that, unsurprisingly, electrical contractors see a strong correlation between business growth and the ability to adequately staff. Almost without exception, the Top 50 said the single biggest barrier to growth was the challenge of finding and retaining quality employees (Fig. 15).

But staffing to handle immediate growth and new opportunity is only part of the labor problem these companies face. The other is building and maintaining a stable, qualified, and trained workforce — a challenge made harder in a job market and economy where workers enjoy growing mobility. The revolving door at many electrical contractors is likely spinning faster as workers seize more options — from retirement to part-time/temporary jobs to new employers that offer higher pay and benefits or better opportunity. The result can be a lot of time and money spent not only hiring for newly created positions, but also keeping existing slots filled.

The best approach for many electrical contractors might be to work to keep the employees they have. But efforts to keep valued employees onboard also carry costs. Whether it’s in the form of more competitive wages and compensation — rated the clear top factor impacting employee retention — or other “soft” incentives, workforce stability improvement strategies don’t come cheap (Fig. 16).

“We haven’t had a great deal of attrition, but we’ve probably been in some bidding wars to keep or hire new people,” Fowler says. “Some of it comes down to money, company culture, and more workplace flexibility.”

Over the last few years, Fowler says, J.F. has worked to improve staff morale and camaraderie. More regular company events have been held that encourage inter-departmental mingling, and awards programs have been instituted.

Training focus mounts

Other companies see the route to reduced employee churn, and other benefits, going through deeper investments in training. Quanta has put $100 million over the last seven years into keeping craft skilled labor fully trained in all aspects of work, most notably safety, says Austin.

“We want to bring people home safely every night, and to work safely our people need the best training,” he says. “The worker of today is not the same worker of 25 years ago, so we’ve had to develop new training techniques.”

A highly trained, adaptable workforce is also becoming more central to growth. Faced with advancing technology that impacts how electrical infrastructure functions and work is performed, electrical contractors need workers with current and increasingly specialized knowledge and skills. The emergence of LED lighting, solar PV and wind energy systems, and building automation systems, for instance, requires workers versed in their intricacies.

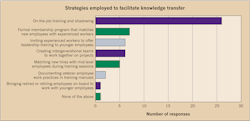

While new hires bring a lot of the book knowledge needed to do work in these emerging areas, there’s a vital knowledge base that resides with veteran employees, many of whom are nearing retirement. Getting that knowledge transferred to younger workers who will pick up the baton is of growing interest to the Top 50. Some are formalizing the process by establishing mentorship programs and staffing project teams with younger and older workers. But most say they rely on a process of osmosis: Younger workers picking up the knowledge they need simply by watching and doing as they perform their jobs (Fig. 17).

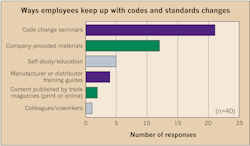

But there’s also a standing need for worker training in core electrical fundamentals, electrical contractors say. For the second survey in a row, the National Electrical Code (NEC) got high mention as an area employees need training support in (Fig. 18). Frequent changes in the NEC and other codes and a lack of uniformity in their adoption by jurisdictions can cloud workers’ understanding, and require more employers to put employees through the learning paces. The most common ways, by far, for contractors to get that done: seminars and company materials (Fig. 19).

While the NEC again got frequent mention as a training need, a couple of areas fell in mentions from last year’s survey: LED/intelligent lighting, which topped the list last year, dipped to fourth; and renewable energy slipped from fourth to sixth. That may be evidence they’re becoming more mainstream.

Tech in the field

Meanwhile, the top mention this year went to a new category: field software, which is being used more as all types of contractors send workers to job sites with mobile devices. Drawn to its potential for boosting productivity, electrical contractors know that to be used effectively those tools must be accompanied by thorough training.

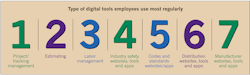

The sheer variety of applications that specialized contractor-focused software can deliver today, combined with the array of products, vendors and platforms involved, elevates the need for comprehensive training. Their growing use in areas critical to efficient project delivery requires across-the-board aptitude. When employed on the job, top electrical contractors say mobile devices are commonly used to access installation, product specification, and codes/standards information (Fig. 20). And when it comes to digital tools generally, project management, estimating, and labor management are common applications (Fig. 21).

Some operations groups within the Newtron Group are early adopters of using mobile technology for job tracking and project specifications and plans, says Schempf. Other groups may follow after seeing whether it can add value, he says, adding one potential negative is worker safety.

“Some industrial facilities are not allowing electronics in the field for safety reasons, so we’re using it more on greenfield projects where it’s more accepted,” he says.

Quanta’s Austin says the company is still evaluating whether mobile devices can be a net plus. “I do have concerns that they may distract the workforce and cause safety concerns, but there’s a place for them.”

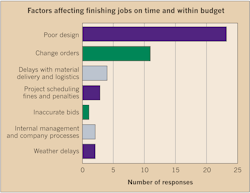

Indeed, their role on job sites could become more central as projects are routinely buffeted from all directions with changes, uncertainties, inaccuracies, and coordination challenges. The ability to stay in the project information loop and react quickly will be vital for contractors looking to head off the multitude of issues that can compromise on-time, on-budget completion. In that regard, the biggest culprits among many, the Top 50 say, are poor designs and change orders, which are often linked (Fig. 22).

H&B’s Herr says he’s seeing more jobs start prematurely, pushed forward by developers’ economic interests.

“We’re seeing more jobs start before plans are complete,” he says. “They sometimes begin 60% done and evolve as it moves forward.”

Hendricks echoes the 60% figure, noting 80% design completion used to be commonplace. “Jobs put out for bid are less complete than they used to be,” he says. “So we have to get very clear on the scope of work in what we propose.”

Design and other coordination-related problems that often plague projects could be reduced with the help of technologies that improve simulation, collaboration, and modeling. BIM has helped in that regard and continues to make headway, but the next frontier is augmented/virtual reality (AR/VR) technologies, which could revolutionize ground-up project development and on-site execution by reducing or eliminating bottlenecks.

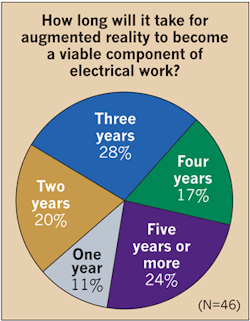

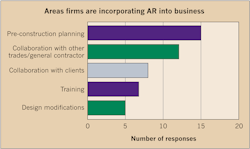

While still embryonic, AR/VR is making headway in construction circles. That’s evident in the assessment of EC&M’s Top 50, 60% of whom said AR, specifically, could be a viable electrical design tool within three years or less (Fig. 23). Both AR and VR could have multiple applications, they say, but pre-construction planning and collaboration hold particular promise (Fig. 24).

Cupertino is working with AR/VR in test scenarios with more clients, says Schott, but there’s still a lot to learn about it.

“It’s still early and we don’t know yet where the value lies,” he says. “The challenge is at what point do go all-in on these types of things and how much influence we can have.”

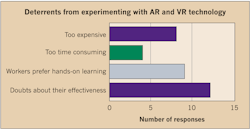

Schott’s reservations are shared by other Top 50 companies. About a third of the 66% who indicated they have yet to experiment with AR/VR said the reason is they have questions about their effectiveness (Fig. 25).

Herr says the technologies’ imprint is there on more jobs, but that for now it’s not filtering down to the contractor level. Still, he says, it could ultimately help contractors if it reduces design implementation challenges the way BIM and 3-D modeling have.

Technology is sure to be at the forefront of Top 50 electrical contractor efforts to stay on a growth curve that took a healthy upward turn in 2017. Whether that trendline lasts into 2018 and beyond is anyone’s guess. But if the broader economy stays strong and they continue to take steps to secure the human capital they need, stay on the leading edge of technology and skills needed in an evolving industry, and focus on timely project delivery, leading electrical contractors will set the pace and a good example for the entire industry.

Zind is a freelance writer based in Lees Summit, Mo. He can be reached at [email protected].

About the Author

Tom Zind

Freelance Writer

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].