Riding the Data Center Boom: EC&M’s 2026 Top 40 Electrical Design Firms Special Report

Key Highlights

- Data centers accounted for over half of electrical design firms' top markets in 2025, significantly boosting revenues and project complexity.

- AI adoption increased to two-thirds of firms, expanding into diagnostics, troubleshooting, and design optimization, though trust in AI for final outputs remains cautious.

- Supply chain disruptions, tariffs, and federal policy uncertainties posed challenges, leading firms to adapt project timelines, modify designs, and diversify markets.

- Labor availability improved slightly, with more firms hiring and focusing on training in AI, energy storage, and electrical codes to meet market demands.

- Firms anticipate continued growth in 2026, driven by electrification, microgrids, and infrastructure resilience, despite potential setbacks from policy and supply chain issues.

Sponsored by Champion Fiberglass

The short answers to just about every question on the economy, employment, and technology seemingly boiled down to two items in 2025: artificial intelligence (AI) and data centers. AI seeped into every crevice of the marketplace while data centers, AI’s lifeblood, became controversial shorthand for a future less demanding of human labor and more demanding of investment, land, power, and water. Squarely in the center of all that disruption sat businesses bringing it all to life — few as consequential as those responsible for the electrical component of those projects.

For one key leg of that stool, the electrical design element, 2025 was another one for the record books — at least in terms of revenue for leading firms, driven in no small measure by data center work. Electrical design firms that made the cut for EC&M’s Top 40 Electrical Design Firms for 2026, based on reported 2025 electrical-only revenue, collectively brought in $5.776 billion. That marked another all-time nominal high for the annual Top 40, topping revenues firms reported for 2024 by 10.6%.

Clues to the growing importance of data centers, as well as myriad other performance and sentiment measures, again came from a proprietary EC&M survey of Top 40 member firms.

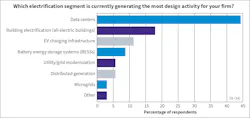

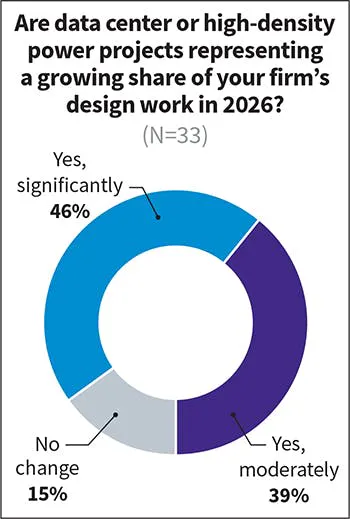

In this year’s installment, just over half of respondents put data centers in their top-three “hottest” markets list (Table 1) for 2025. That share has steadily risen, from 22% in 2023 to 43% in 2024. Amplifying that finding, 44% placed data centers as the single “electrification-related” task generating the most design work for their firms (Fig. 1), far outpacing others, including all-electric buildings and electric vehicle (EV) charging infrastructure. Likewise, nearly half expect data centers to be a significantly growing share of their 2026 design work (Fig. 2).

Hogging the spotlight

More focus on the data center space may have come at the expense of other markets. At 35%, in line with last year but 16 points behind first-place data centers, the power/utility market got the second-most top three mentions. Health care had the third most — but fell sharply — from a 43% tie with data centers last year to 27% this year. Other top 2025 markets were government, education, manufacturing and water, all of which tapered off in mentions.

Lagging markets — those deemed “coolest” — were a little less concentrated (Table 2). Hospitality and private office again led the pack, but not as forcefully. In 2024, they were, respectively, in 38% and 34% of respondents’ top three lists; this year, they were each at 26%. Retail, tied for second with education and residential and new to the upper end of the cool list along with several others including manufacturing and renewables, also edged down, from 24% to 19%.

That wider dispersion in “cool” markets may suggest that despite the unusually large impact of data centers as a market, design firms found a lot that was working in 2025, as solid revenue growth attests. Data centers clearly grabbed the limelight, padding many firms’ bottom lines, but others found a rough equivalent in other dynamic markets, some closely linked.

Wade Leipold, executive vice president of Faith Technologies Incorporated (FTI), (No. 14), Menasha, Wis., is quick to attribute much of the firm’s 31% design revenue boost to data center work. More projects with more complexity and more compressed timelines are keeping FTI humming, with no end in sight. It may have the feel of a “bubble,” he says, but “there’s a lot of money behind this data center activity now, which is a major difference from other phases” of past manias like the infamous dot-com boom and bust. “Even with a backlog, we don’t see anything tapering off at this point.”

Water-market specialist Carollo Engineers, (No. 10), Walnut Creek, Calif., capitalized on continued demand not only for electrical work in rehabbing and building traditional treatment and delivery projects, but also on surging demand for water cooling systems in the data center market.

The former is growing, Ron Burdick, SVP and discipline engineering director says, because “all of the infrastructure is dated” and feeling the strain of growing populations and industry, requiring enhancements and “upgraded facilities to meet demands for higher-quality discharge.”

Meanwhile, adds Joe Karl, business development manager for electrical programming, instrumentation and controls, more data centers, as well as chip plants, are turning to water for essential cooling, requiring complex EPIC designs for pre- and post-treatment systems to deliver, circulate, and expel it safely and cleanly.

“Data centers used to be tiny with no need for big water-cooling systems,” he says. “Now, as they’ve grown in size, these servers are generating much more heat (and water has become the more effective cooling solution).”

Rapid data center expansion has put more demand on power resources, supporting electrical design and consulting business for electric utility specialists like Toth & Associates, Inc., (No. 26), Springfield, Mo. That market was “extremely strong” for the company last year, says president Adam Toth, supercharged by surging data center demand for ample, reliable power. But utilities had other pressing needs, too.

“A lot of reserve generation capacity that needs to be connected to the grid is being built, and there are ongoing projects to retire, rebuild, and replace older electrical infrastructure,” Toth says.

2025: It was complicated

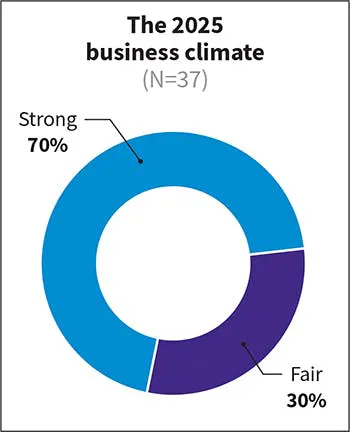

While almost all Top 40 companies saw revenue growth in 2025 — the top 10 averaging about 20% — assessments of the past year were somewhat muted. Most rated the prior year business climate strong (Fig. 3), but that share dipped to 70%; the number was 78% for last year’s Top 40.

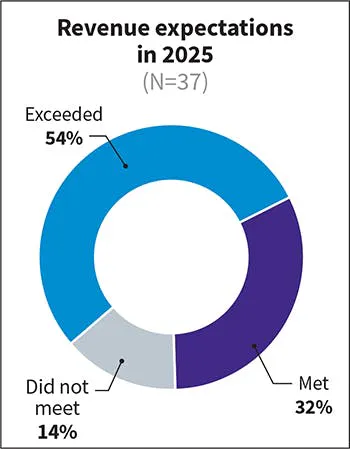

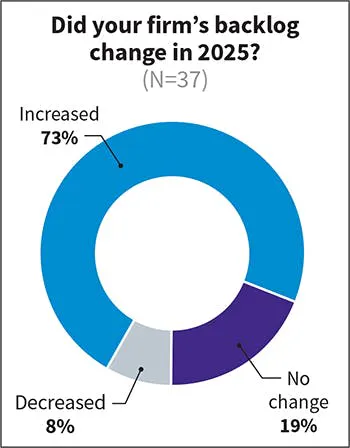

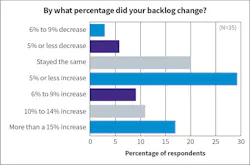

Also, more firms said they only met or did not meet revenue expectations (Fig. 4). Again, though, a slim majority said revenues exceeded expectations. On another measure, the share saying backlog increased dipped 13 points to 73% (Fig. 5). A majority of those reporting a change — up or down — put it at 9% or less. More this year reported no change (Fig. 6).

More tepid assessments of the year might be linked to complications design firms and their clients encountered. The year of the tariff imposed rising prices, supply chain backups, and uncertainty on project developers. That, plus the data center build-out bulge that upset a delicate supply and demand picture for essential electrical products, made life harder for many design firms and their clients.

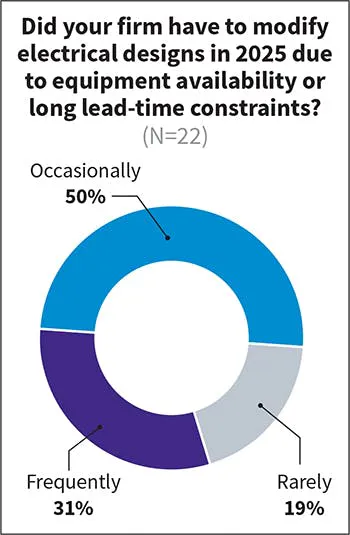

Broadly speaking, tariffs and shifting trade policies took their toll, Top 40 firms say. All said nothing positive came out of that for their firms, only negatives (Fig. 7). They weren’t crippling — most called the impact “minor” — but they amounted to something new to deal with. One byproduct (longer lead times on equipment and general availability issues) directly impacted their work, many said (Fig. 8). Half agreed they “occasionally” had to modify electrical designs, while another third termed project changes as “frequent.”

HED, (No. 34), Royal Oak, Mich., called the business climate only fair, largely because of “a lack of predictability and confidence in the market,” which led to more clients growing “gun shy about spending money than in the past,” says Nicki Sparks, principal and electrical engineering leader. Tariffs and uncertain timelines for product availability contributed to a higher level of projects put on hold, leading to backlog growth. Others, she says, demanded more frequent monitoring and project team coordination to lock down products, identify alternate suppliers, and minimize final design impact.

For Smith Seckman Reid (No. 29), Nashville, Tenn., last year was called strong, a continuation of a growth spurt that took hold in 2021, says Patrik Harden, director of electrical engineering. It ended the year with a two-year, $230-million backlog, setting SSR up for another year of 10% growth. SSR’s top markets were all clicking last year, most notably health care, specifically continuation of a massive pediatric hospital project.

“We’ve seen incredible growth from that project; you could clearly see its impact in our financials,” he says. “It’s the single largest in our history, still ongoing, with 15 electrical designers on it.”

A broad swath of markets, mostly infrastructure related, kept business humming for CDM Smith, Inc. (No. 23), Boston.

“Out of the gate in 2025, we were going crazy,” says Matt Goss, MEP practice leader, who attributed the firm’s “very strong” showing in part to growth in microgrid projects, which present a “hot opportunity.” Interest in them ramped up last year, he says, as the need for reliable sources of power more independent of a stressed electrical grid became more evident.

“Some projects were paused based on legislation (targeting renewable energy), but with changes in climate and the need for resilience in power sources, we continue to see the need,” he says. “Clients are much more attuned to that, seeing what’s going on around them and the need to be

more proactive.”

A resilient market

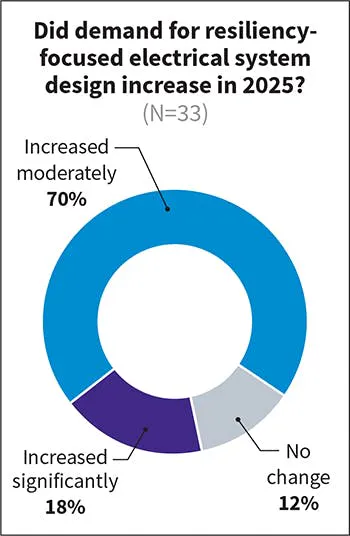

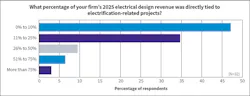

Microgrids and other similar resiliency/green power-inspired projects are growing out of a broad push to cement electricity as the nation’s dominant power source, a trend clearly benefiting — and challenging — design firms. Nearly 20% of Top 40 firms said demand for resiliency-focused system design increased significantly last year (Fig. 9), while most of the rest called demand growth “moderate.” Relatedly, close to 20% attributed more than 25% of their 2025 revenue to “electrification-related” projects spanning the likes of EV charging, grid modernization and microgrids (Fig. 10). Still, such projects remain on the fringe for most; nearly half put it at no more than 10%.

Entrenched in the mission-critical space, HED dealt with more resiliency concerns in 2025, Sparks says. Such facilities require robust backup and alternative power features that must be designed with a flexible and creative engineering approach.

“‘How does the building function from an interconnection standpoint?’ is a question designers face,” she says. “Energy nodes will become more critical, and that means staff must be open to different perspectives and ways of thinking. You can’t be black or white on electrical design anymore, except when it comes to safety.”

Power redundancy was a growing component of the complexity that Salas O’Brien (No. 6), Irvine, Calif., faced in its work in key markets like pharma and health care. President Darin Anderson says nearly all its clients are moving toward an “absolute-cannot-fail” stance when it comes to power. The question then becomes: “How much redundancy do you want to factor in,” he says.

While redundancy may depend on electric alternatives, including strictly to the grid via on-site generation employing renewables, microgrids, or generators, Anderson says interest in electrification among clients is moving ahead. It’s an especially high priority in California health care projects, he says, noting that “seven new hospitals in progress are all electric.” And, he adds, more higher education clients are embracing the concept.

Seeing growth amid obstacles

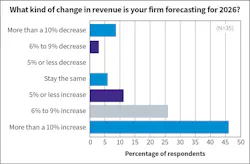

Electrification is certain to help drive the fortunes of design firms in 2026, a year top firms expect will deliver more growth. Optimism about current-year revenue growth is at a three-year high, with 83% expecting an increase (Fig. 11), a six-percentage-point boost. Most notably, nearly half see it rising more than 10%, a nine-point increase.

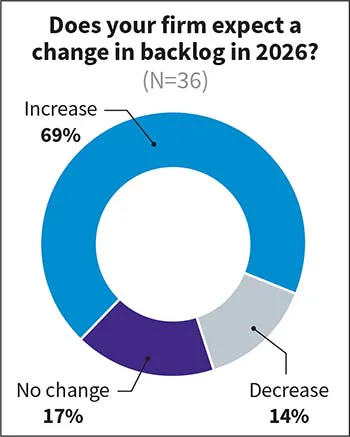

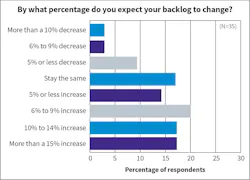

Slightly fewer firms, though, see their backlog increasing in 2026. Sixty-nine percent see an increase, down six points (Fig. 12). The biggest shift is in those expecting a decrease: 14%, up from 3% a year ago. More than half expecting a decline put it at five percent or less, while half expecting an increase see one of more than 10% (Fig. 13).

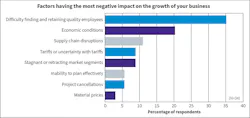

But business growth, maybe near-term at least, could be endangered by a broader mix of obstacles. In a noteworthy shift, more Top 40 firms identified factors other than labor challenges as the single most impactful growth threat — the share picking labor as the top negative plunged from 62% to 35% (Fig. 14). Drawing more mentions were supply chain disruptions, tariffs, stagnant/retracting markets, planning challenges, and project cancellations — each reflective of a year that elevated a menu of more pressing concerns for businesses. Second to labor, “economic conditions” stayed mostly steady at 21%.

Carollo Engineers expects more steady growth in 2026, fueled by relentless demand in the water systems business it dominates plus continued build-out of a growing instrumentation, programming and controls specialty whose leaders are “noticing more opportunity and chasing it” as it matures from “a side hustle” for the firm, says Karl.

The firm’s single biggest growth threat may come from an underappreciated, but growing concern. It’s an inability to plan effectively, Burdick says, a problem exacerbated by the digitally enabled planning environment that “at times” has “everyone moving so fast,” creating “a lack of overarching strategic thought.” Wasted time, misaligned objectives, “everyone jumping through hoops,” and chronic “multi-tasking” can hamper productivity and steal the time needed to pursue business growth.

Tempered growth is the 2026 forecast for CDM Smith, Goss says. He sees a continued lift from electrical infrastructure upgrades and resiliency projects, but also sees emerging opportunity in data centers, a “logical next step” the firm has been staffing up to take. He also has his eye on the manufacturing sector — one he expects will ramp up as the onshoring trend continues.

A lingering concern this year for CDM Smith and other firms is tariffs and the impact of other federal policies.

“There’s a lot of uncertainty,” Goss says. “They could negatively impact projects, causing them to be stopped or delayed, but the biggest thing is the angst and uncertainty (around them).” Maybe the plug is pulled or a design project is put on the shelf, so the client is wanting to wait it out a bit.”

Assessing federal policy impacts

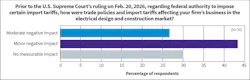

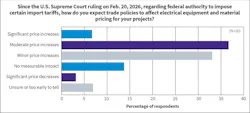

While there’s growing clarity around tariffs, due partly to a February Supreme Court ruling limiting their application, top firms remain wary. Seventy percent expect trade policies generally to impose minor to moderate price increases on electrical equipment and materials used in their projects (Fig. 15).

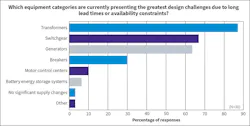

The flip side of that problem is availability, which has impacted electrical design activities. While a mix of electrical equipment has been harder to secure in the last year, firms’ biggest worry remains concentrated in the critical categories of transformers, switchgear, and generators (Fig. 16).

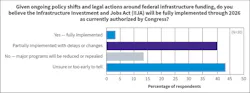

Another possible growth-related concern for design firms is the fate of federally supported infrastructure improvements. The Infrastructure Investment and Jobs Act (IIJA) contained billions for a range of projects when implemented under President Biden. The IIJA’s fate now is uncertain under a Trump administration that is more circumspect about some of its elements. That could most affect design firms working in areas tied to renewable energy, but four in 10 firms say how that plays out is anyone’s guess (Fig. 17). Another 40% expect some changes resulting in partial IIJA implementation or funding delays.

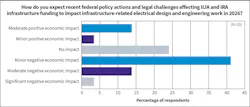

That, along with a similar scaling back of the Inflation Reduction Act (IRA), which also included money for infrastructure, would be mostly a negative for business, firms say. But maybe given the comparatively limited electrical profile of many funded projects, most firms expect changes to have either no impact or limited negative impact on their infrastructure-related work (Fig. 18).

EV charging infrastructure is one area where firms could feel some pain. If federal support wanes, says FTI’s Leipold, progress on building a nationwide charging network could stall. An early warning sign is car companies scaling back EV plans, Leipold says, but FTI, which is partnering in launching the privately funded Zero 60 charging network using both its design and construction business units, sees long-term opportunity.

The president of Toth & Associates sees risk to renewable energy in any scaling back of IIJA and IRA. That market has hit a speed bump already, possibly changing the calculations of utilities (the firm’s primary market), trying to gauge future electricity demand and plan for renewables integration.

“Five years ago, there were a ton of them (wind and solar farms) on the horizon, but almost overnight they seemed to go away,” Toth says. “If that’s all you did, now you’re hurting.”

Labor pressures cool

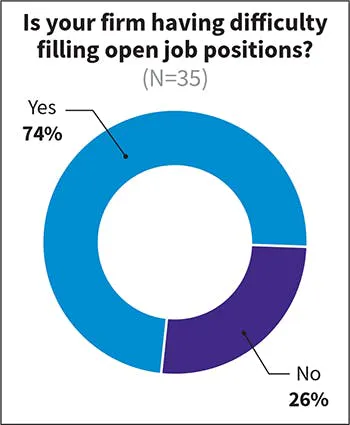

Infrastructure funding disruptions are one of several sources of growth risk for design firms. But one that’s persisted — labor — might be moderating. Finding and keeping employees was heavily marked down as a growth challenge this year amidst other pressing concerns. Also, the share of firms saying they were having trouble filling open positions dropped 15 points from last year, to 74% (Fig. 19), the lowest number in several years.

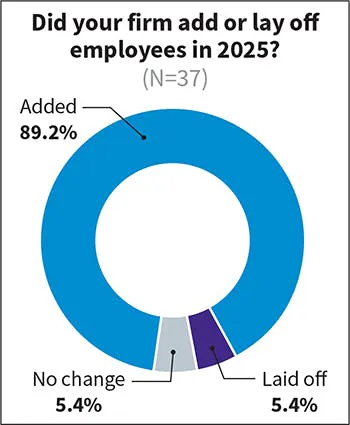

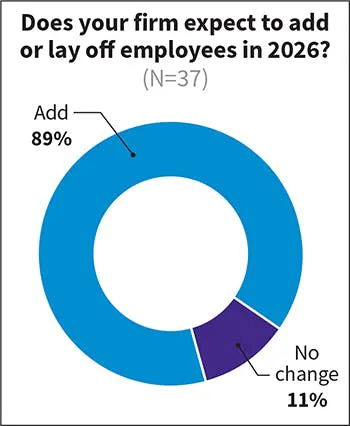

That’s good news because firms are still in hiring mode. Similar to previous years, 89% said they added employees in the prior year (Fig. 20), the same percentage that expect to add staff in the current year (Fig. 21), also in line with prior surveys. And, again, the most pressing needs in design staffing are clearly project engineer and supervising engineer, dwarfing others and both rising 10 percentage points (Fig. 22).

Like most other firms, SSR has an ongoing challenge of finding the five-to-10-year design talent but is willing to wait for the right fit. Experience applicable to the firm’s work is prized to maximize opportunity and help cultivate staff, so “we can wait for a year sometimes to find someone,” Harden says since “one out of 100 is what we’re looking for” in certain situations.

Newly minted talent is easier to find, Harden says, so the firm staffs career fairs and sometimes gets directly involved in helping college seniors with design projects. Internships are key, but half typically move on. For example, “one guy was here eight months and then decided to go build rockets.”

HED continues to hire, Sparks says, but the challenge to recruit and retain continues. The work can be a tough sell to younger talent when other engineering fields, other electrical disciplines and sometimes jobs “on the owner’s side” beckon, often with higher pay and more stimulation, she says.

"For the length of my career, it’s always been a challenge to find designers, and that’s partly because power is not taught as much in schools,” she says. “Most don’t know much about this industry so we have to woo them over.”

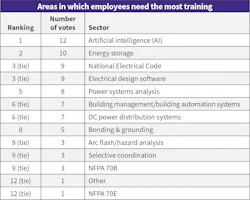

Training is one way firms can fight the staffing battle, providing a path to career growth for employees and a productivity boost alongside keeping the firm competitive in evolving markets. From a list of a dozen technical training areas, firms chose three needing the most attention and support. Four stood out: AI, energy storage, National Electrical Code, and electrical design software — each highly ranked last year. Last year’s top choice, power systems analysis, named by half, was named by only 28%, while AI advanced 10 points to 41% (Table 3).

Dedicated training time and dollars can be harder to find when business is booming, Carollo’s Burdick says. So the solution often is to deliver it on the job. Critical areas for the firm are electrical systems studies and codes.

“Everything is changing across the country with codes and mandates, and it’s just hard to stay on top of it all,” he says.

At FTI, growth in data center work is prompting the firm to look at building broader expertise it can market to clients.

“We’re standing up a data center operations course to meet that demand,” Leipold says. “There’s a lot of emphasis on design and build, but there’s also the element of what it looks like to maintain these sites in perpetuity. That will take some specialized training.”

“Top-notch technical excellence” remains an essential training priority for Salas O’Brien, delivered through a library of resources and subject matter experts, Anderson says. A softer skill, project management, is getting more attention as annual volume reaches 25,000.

“We just finished a 12-module education series on that, focused on tailoring skills for three levels, from rising to senior leader,” he says. “The growing speed and complexity of the work makes it all the more important to be well trained in the critical points.”

AI usage spreads

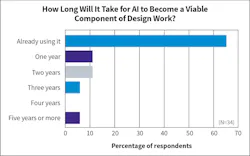

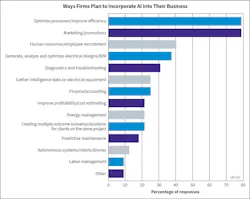

An answer to that and a host of other challenges firms face may lie in AI. Two-thirds say they’re already using it to some degree in their electrical design work — a 12-point increase over last year and 25 points higher than two years ago (Fig. 23). In addition to generating and optimizing designs, cited by 38%, AI’s utilization in other areas is expanding. Common applications that have grown notably over last year include diagnostics/troubleshooting, efficiency improvement, marketing, and human resources (Fig. 24).

Salas O’Brien is successfully leaning into AI to help smooth out common bumps in the design process, Anderson says, but a sharp eye is kept on the end game.

“It’s been a helpful tool to automate some repetitive functions and deliver more sophisticated projects in a more coordinated way, but the quality of deliverables still must be proven,” he says.

A technology council at SSR is spearheading customized AI design applications, building off a ChatGPT base.

“We’ll get a design request for a floorplan, say, and we’ll load it in there and let AI take a first pass at it,” Harden says. “We’re constantly feeding it new knowledge from parts of our server system.”

AI holds promise for his firm, Toth says, but “we’ve not yet seen it making monumental changes in actual design.” The concern is that it can’t yet be trusted like it can be for coding, spreadsheets, reports, and email writing, he says.

“It’s not there yet for the nuts and bolts of electrical design,” Toth adds. “There’s no acceptance yet of an AI-stamped drawing.”

About the Author

Tom Zind

Freelance Writer

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].