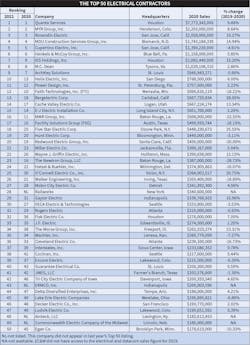

Hanging Tough: EC&M’s 2021 Top 50 Electrical Contractors Special Report

With a mixture of doggedness, patience, creativity, and flexibility, most of the nation’s top electrical contractors managed to outmuscle the unprecedented COVID-19 pandemic year of 2020, .many even posting revenue gains that helped push the group's top line by $1 billion over 2019.

Sponsored by LaborChart

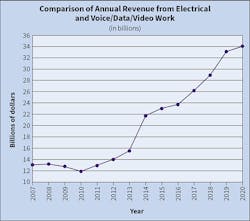

The companies, whose 2020 electrical revenues placed them in the 2021 installment of the annual EC&M Top 50 Electrical Contractors ranking (Table 1), escaped the debilitating fallout many in non-essential industries faced from the pandemic. But they still had to contend with project cancellations, delays and disruptions, seized-up markets, supply constraints, stay-at-home orders, distancing protocols, and a disorienting climate of uncertainty. The ultimate toll might not be fully revealed until 2021 or 2022 numbers are reconciled. Still, the Top 50 cobbled together enough business last year to log its 10th consecutive year of revenue growth, registering almost 3% higher than 2019 at $34.1 billion, nearly three times the amount the Top 50 booked a decade ago (Fig 1).

That number, however, obscures the fact that 2020 was clearly a challenging year for many of the Top 50 contractors. Responses to a range of questions in the annual EC&M survey that produces the Top 50 rankings confirm that contractors faced novel difficulties last year even as they had to contend with long-term obstacles that the pandemic only aggravated. At the same time, though, optimism that an overall bright future lies ahead came through in both the survey responses and commentary from select contractors.

Climate change

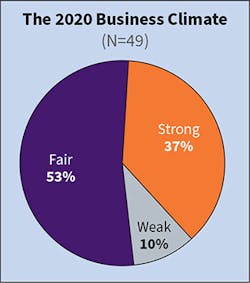

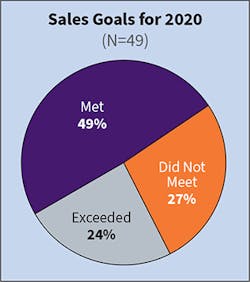

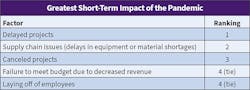

First, the obvious: There was broad agreement that 2020 was a downer. Even though 33 firms saw their revenues grow in 2020, only 37% of the Top 50 said they’d rate last year’s business climate as “strong,” as shown in (Fig 2). That’s a sharp drop from the last two surveys, in which more than 80% said the prior year’s climate was strong. “Fair” was this year’s description of choice, surely a reflection of COVID-19 keeping a lid on opportunity and complicating all aspects of running a business. More specifically, contractors said the year pummeled the optimism they had at the outset. Only one-quarter said they exceeded their sales goal for the year (Fig 3), down from nearly half of last year’s respondents who said they surpassed their 2019 sales goals. But failure to hit revenue targets wasn’t the chief negative by-product of the pandemic. Contractors said the most palpable short-term impacts were delayed projects and canceled projects along with material supply chain complications (Table 2).

At ArchKey Solutions (No. 9), St. Louis, combined revenues from multiple operating companies declined as work in some important markets receded or grew more complex to navigate.

“It was a challenging year, requiring a lot of adaptation and perseverance as our ‘normal’ ways of doing business changed rapidly,” says Clay Scharff, president and CEO. “Markets that were strong for us, like sports and entertainment, saw the largest impact, while other markets like mission-critical had more demands placed on them.”

Market and geographical diversification helped Commonwealth Electric Company of the Midwest (No. 49), Lincoln, Neb., deftly steer around the pandemic. Recent expansion into data center projects was fortuitous as those stayed strong and became especially abundant in the company’s Midwest backyard where power costs and labor availability lure builders. Still, multiple projects were delayed, the company idled 38% of its labor force for several months, and even a chunk of service business was curtailed for a time, says Company President Michael Price, who spent a lot of time figuring out how to work amidst the pandemic, which reduced productivity, among other impacts.

“I formed a COVID-19 response team to deal with all of the issues that it raised for how to adapt,” he says. “Since then, we’ve had to update that plan 18 times. As we got that figured out and learned how to work with it, we moved ahead.”

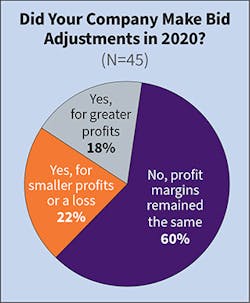

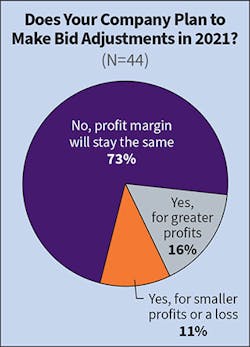

The contraction of new business opportunities due to heightened uncertainty, along with in-progress project delays and cancellations, led to generally more competition for projects that did go out to bid in 2020. That had the effect of putting the squeeze on more contractors to bid more aggressively — on more projects and on less favorable terms. Ten firms said they made bid adjustments resulting in smaller profits or even a loss (Fig. 4), a big shift from the last two surveys in which only 2% of firms said they did. About the same number of firms, however, said they bid for higher profits, while 60% said margins were unchanged, down from 77% in last year’s survey.

The scramble for work was evident in the Greater New York City market, where Five Star Electric Corp. (No. 18), Ozone Park, N.Y., is active. President and CEO Russ Lancey says his company was able to hold the line and stay selective but guesses many others felt pressure to bend.

“The market was more aggressive and competitive because everyone was hungry for work,” he says. “We saw some projects with as many as 15 companies on the bid list so that probably means it’s been slimmer pickings and maybe tougher going as far as being a successful bidder. A lot were just wanting to stay busy.”

Competition for available jobs seemed stiffer in markets that Interstates, Inc. (No. 37), Sioux Center, Iowa, works, especially in the second half as more companies scrambled for work as pandemic restrictions began lifting, says Joel Van Egdom, chief financial officer. A primary driver for that increased competition was the prolonged slowdown in the commercial building space.

“As companies worked through their backlog, we saw bid lists expand and companies get more aggressive on pricing and margins to win work,” he says. “Now, though, we’re seeing some declining to bid because their backlog is back up, and there are challenges in securing skilled workers. So there’s an opportunity to put some more margin back in.”

Market turbulence

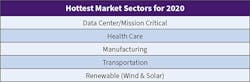

COVID-19 also scrambled the deck when it came to market sector opportunities for contractors. Markets that had been seeing increased activity in a brightening pre-pandemic economy, such as offices, education, and retail, stumbled. Others that had been strong stayed strong, despite O. And still others surged because their long-term prospects in a post-Covid future weren’t shaken. Tallying it all up, contractors again judged data centers and health care the two hottest markets but put three newcomers in the next three slots: manufacturing, transportation, and renewable energy (Table 3). The coldest sector list also shuffled from 2019, with private office, education/institution, and sports/recreation joining repeat selections hospitality and retail in the top five (Table 4).

Cupertino Electric (No. 5), San Jose, Calif., is trying to capitalize both on its multi-year effort to diversify across markets and double down on its key markets. In the former, a stronger push into renewable energy paid dividends in 2020. In the latter, data centers have stayed a consistent winner. A newer initiative puts the company in line to benefit from higher infrastructure spending as well.

“A new public infrastructure group under our commercial group will benefit us going forward as transit spending in California grows,” he says. “It’s part of an effort to get us deeper into large-scale projects where fewer competitors have those capabilities.”

Large, multi-year public projects that stayed alive also kept Fisk Electric Co., (No. 32), Houston, insulated from market gyrations that cut into gap-filling smaller project work, says Cory Borchardt, senior VP of operations.

“We didn’t see those slow anything like industrial and commercial, so we focused on and shifted resources to those large projects that were in place,” he says.

Water, airport, subway, and warehouse projects moved ahead; however, some others, such as hospitals, were suspended but now show new life. As Covid recedes, Borchardt says, Fisk expects further shifts in demand in health care and other key opportunity sectors “as money is reallocated into different types of projects” by clients whose perspective on future needs has been altered by COVID-19.

Sheer size helped MDU Construction Services (No. 4), Bismarck, N.D., manage market disruptions in 2020. The conglomerate’s 16 operating companies, geographically spread out, provided enough market diversification to keep combined revenues up for the year. But a key factor, says Vice President Ray Kelly, was the client base.

“Big national customers that remained consistent in their plans helped us,” he says. “There were not as many fits and starts with their plans, especially those in the mission-critical space, technology, and automotive.”

Rebound bound?

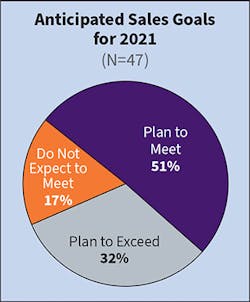

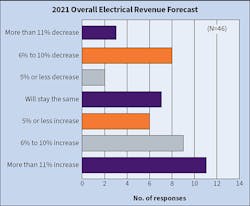

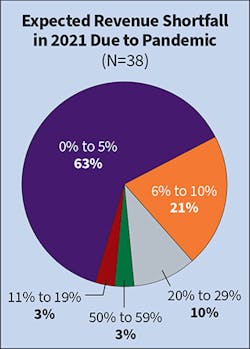

Midway through 2021, contractors were weighing whether more of that consistency and a return to normal was in the cards. That looked dicey with the emergence of the virus’ potent Delta variant, but by several measures, many of the Top 50 saw a better business year taking shape. Close to half said they were already back to “business as usual” (Fig 5); a third said they expected to exceed their sales goal for the year, up from 12% last year (Fig 6); 90% said they saw a chance for stable or higher profits, up 27 percentage points (Fig 7); 56% saw 2021 revenues increasing, up from 25% (Fig 8); and projections for pandemic-caused 2021 revenue shortfalls were much more heavily clustered on the low-end — 84% seeing a 0% to 10% range, compared with 64% last year (Fig 9).

Heartened by a big rebound in project starts and bidding late last year, Fisk Electric sees a chance for a repeat revenue gain for 2021 as large infrastructure projects proliferate and opportunities to piggyback on parent company Tutor Perini Corp.’s construction projects emerge.

“Work came back with a vengeance later in the year, and there was a lot of activity. Even with the materials price increases, we were seeing that put some owners on the hesitant side,” says Borchardt. “The amount of bid opportunities for us are now back to pre-pandemic levels, and pent-up demand is coming back.”

One of just a handful of companies that rated 2020’s business climate as “weak,” Egan Company (No. 50), Brooklyn Park, Minn., sees a chance for 2021 to be better, but the slow pace of project starts has President and CEO Duane Hendricks looking at a longer path back to normal. Bidding continues to be crowded, he says, while materials are harder to source.

“Things may start to loosen up next spring, and we’ll be in a position to get more new work,” he says. “We have the capacity to not overreact to market conditions so that puts us in an overall good position. We just have to be more selective in the projects we bid and make sure that we’re getting reasonable margins.”

Interstates, after realizing 9% revenue growth in 2020, sees continued strength in 2021 and beyond in its primary markets, which include industrial, food processing, and data centers, provided the overall economy stays strong and building costs don’t get out of hand.

“We’re not seeing any shaking of confidence of the owners we work with,” Van Egdom says. “Their capital budgets for the next year or two are as high as they’ve ever been in some cases, and there is a lot of cash on hand. We’d expect that appetites could wane if costs escalate but, so far, we’re not seeing any impact on how they plan to spend.”

A material problem

Rising costs that could come with a sustained resurgence of inflation could become worrisome for contractors. They’ve gotten a taste of it already as availability and prices of construction materials were affected beginning last year by coronavirus-related supply chain disruptions and a stimulus-flooded economy. A lack of visibility on material supply and price has also made project bidding and successful completion a more difficult task.

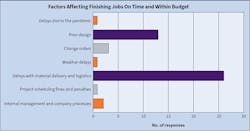

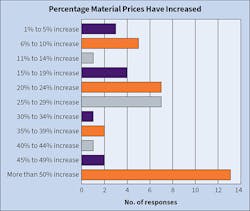

Delays and logistical challenges in securing materials, deemed a leading short-term by-product of the pandemic, also came in as the top-ranked impediment to on-time/on-budget project completion in 2020 (Fig 10). Those delays have cost implications that compound the profit worries presented by spiking prices of the materials themselves, which have continued into 2021. In last year’s survey, contractors said increases on the most price-volatile materials last year were mostly 10% and under. This year, the range has expanded greatly to include 28% saying the biggest increases are topping 50% on some materials (Fig 11), wire and cable and conduit/raceway/wireway (Fig 12), identified most often as the biggest price gainers of the year.

Five Star Electric’s Lancey says unusually widespread materials sourcing challenges have presented contractors with a new set of problems. Shortages, longer lead times, and wider materials price swings and spikes are taking uncertainty to new levels and pressuring contractors to become more accurate forecasters.

“It’s creating an additional layer of difficulty in bidding and building,” he says. “We’re letting owners know that things are taking longer than expected, and they’re more expensive. That’s taken into account when we bid, but it’s also a challenge when you have a project schedule laid out and things change.”

MDU’s Kelly says price escalations are complicating client calculations on timing for moving ahead with projects, with some owners contemplating holds because of “sticker shock” and some facing longer wait times. MDU has had some success moderating materials issues by leveraging sturdy relationships with suppliers, but some are unavoidable.

“With some of our big mission-critical clients, some lead times on transformers and similar equipment has moved out from 12 weeks to 36 weeks, adding maybe half a year to a facility ready date,” he says.

A new labor twist

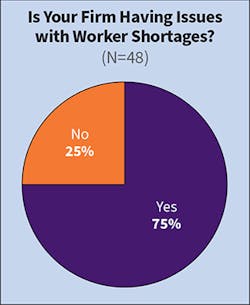

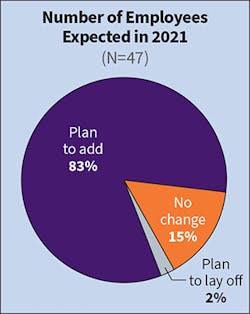

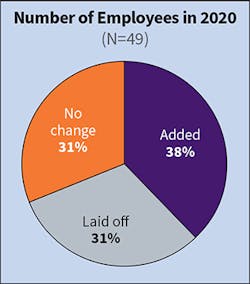

Another growing cost worry for contractors is the rising price of labor. Wages across the economy have been rising at their fastest clip in years since last summer. And if a surge in post-COVID-19 demand materializes, construction employers, already battling structural labor shortages, could face a heftier bill. That scenario could be teed up because after the business slowdown reduced labor pressures, three-quarters of the Top 50 now say they’re facing worker shortages (Fig 13). As business returns, 83% say they’re planning to add to their labor forces (Fig 14). That’s a big swing from last year on both counts: Only about a quarter said last summer they were short on labor and were expecting to add employees. As it happened, a little more than a third reported a net increase in hiring in 2020, down from 75% in 2019 (Fig 15).

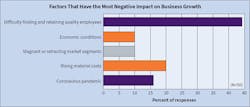

Costlier labor might be an acceptable tradeoff if it helps address contractors’ worker supply problems. Chronic skilled labor shortages have been a near constant backdrop for contractors and many of the Top 50 continue to see hiring as their biggest challenge if the worst of the pandemic is over. Echoing pre-COVID-19 Top 50 contractors, nearly half said finding and retaining quality employees was the single thorniest company growth impediment (Fig 16).

“If I had 150 electricians and foremen, we could hire them tomorrow,” says Commonwealth’s Price. “There’s a lack of workers. We’re trying to find electrical apprentices and field leadership as well to get the work done.”

Like many other contractors, Commonwealth is trying to adapt to the worker shortage by moving to more off-site pre-fabrication work that can utilize less skilled labor that’s in greater supply. Union agreements, however, complicate the company’s ability to take full advantage of pre-fab’s productivity features, he says.

The tight construction labor market has MDU thinking creatively on how to cope with the twin challenges of workers leaving and evolving electrical work demanding those with different skill sets. That’s prompting it to look farther afield — to new pools of talent in non-traditional places.

“We’re doing a lot of outreach to include those who might cross over from another industry, such as the software field where we could get people into our 3-D modeling area,” says Kelly.

While long-term growth will create professional talent needs at many levels, the more immediate need now might be the muscle and skills to simply get stuff built. Electrical foreman, journeyman, and electrician topped the list of the hardest positions to fill, a shift from 2019, when project manager and job superintendent ranked just below foreman (Fig 17).

“Our challenge is people — finding skilled workers to competently take on these jobs,” says Fisk’s Borchardt. “It’s been tough with incentives making it harder to keep people on the job. We’re trying to rebound from that, and we’ve resorted to doing more of our own recruiting and encouraging union apprenticeship committees to take on bigger classes.”

Interstates needs more electricians and foremen, too, but also is scouting for more project management and engineering talent needed for both construction and contracted plant operating system service work, says Van Egdom. The company is recruiting more outside the industry and banking on being able to offer prospects the opportunity to do more work remotely, a practice the pandemic has helped cement.

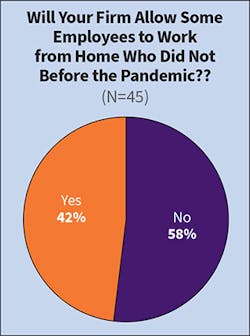

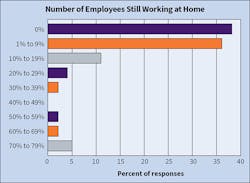

Far from all contractors, though, are sold on the idea of making work-from-home arrangements permanent or widespread. A solid majority said 100% office-based workers pre-pandemic wouldn’t have the chance to work remotely going forward (Fig 18). After transitioning many to at least some remote work in 2020, contractors have moved many back to the office. Nearly half last summer said up to 10% of their employees had shifted to some remote work. A year later, almost 40% said those arrangements have ended (Fig 19).

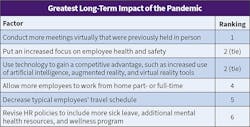

The pandemic, however, could produce some long-term human resource-management consequences for contractors. Eventual expanded remote work for employees is one but mentioned more often as lasting pandemic-induced changes were expanded virtual meetings, increased attention to employee health and safety, and using technology more to boost productivity and competitiveness (Table 5).

Technology payoff

The construction industry continues to increase and expand its adoption of information technology, and electrical contractors aren’t being left behind. Echoing survey findings that field workers are using apps and software extensively for project, time, and labor management (Table 6), and that product specifications, installation guidelines, and codes and standards requirements are the most accessed on mobile devices (Table 7), some contractors say productivity improvement is a primary goal of expanded digitization, especially as project schedules grow more compressed and staffing levels are pressured.

ArchKey’s Scharff says digitization has become central to the company’s “continuous improvement” push aimed at gaining better understanding of workflow and processes that are central to profitability. “Making sure you have the data and insight into your processes to make smart changes that will yield better, more efficient and safer results for our people is critical,” he says.

As sophisticated and capable as such technology has become, however, it demands worker buy-in and understanding to deliver its full value to contractors. That’s especially true when it comes to applications used on the ground in projects via mobile devices. Pushing technology out to work sites, where the work occurs, delivers a big part of the value proposition. That might be why more contractors surveyed have consistently named field apps and software as the area where employees need the most training (Table 8). That may partly reflect the still-unsettled state of the technology, says Cupertino’s Schott.

“A constant issue in front of us is so many new technologies and new software platforms,” he says. “It can be overwhelming when you have four different projects underway, and four different software platforms you’re working with. So you have to be careful sometimes about grabbing the shiny new thing. There’s an impact on employees when we throw too much at them.”

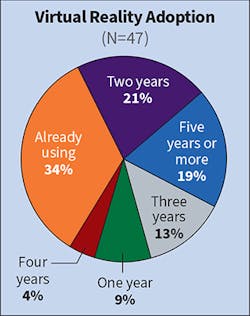

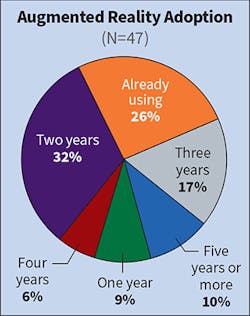

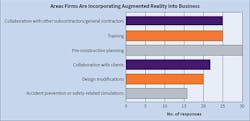

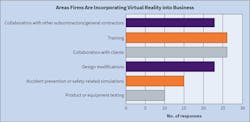

Some potentially game-changing construction technologies, however, have been moving ahead slowly. Notable are augmented reality (AR) and virtual reality (VR) — tools that allow unprecedented levels of detailed plan visualization, design changes, collaboration, and project planning and scheduling. The Top 50 survey has monitored sentiment on AR/VR as viable electrical design tools for several years, finding that most contractors say they’re still a ways down the road. This year, though, the ranks of those saying each is now viable took a jump, from 20% last year to a record 34% this year for VR (Fig. 20), and less dramatic, from 18% to a record 25% for AR (Fig. 21). What changed little, though, was that collaboration, planning, and training were selected as the primary applications for both AR and VR (Fig. 22 and Fig. 23).

Commonwealth Electric’s engineering group and building information modeling group has been experimenting with VR, “using it to show some customers where components will be while physically standing in the model,” but routine use, says Price, isn’t imminent with either AR or VR.

“The customer has to have the money for it,” he says. “But it’s interesting stuff and maybe there comes a time when that’s essential to making money, but not now.”

Now, it’s maybe fair to say, contractors need to focus on the nuts and bolts of getting their businesses fully back on track. In the wake of pandemic-related disruptions that may not show up in revenue and profit numbers until several quarters down the road, many might need to adjust to some new realities that could have staying power — from shifts in relative strengths of markets to employees working remotely to an ever tougher labor availability landscape. Indeed, contractors’ views of top challenges their businesses face in the next few years broadened this year, partly reflective of the pandemic’s impact. Labor-related issues still dominate contractors’ views of their “single biggest business challenge,” but now the list includes “price escalations;” vendor provision of “real-time information for cost and time impacts to our projects;” “securing enough work with a fair margin;” more bidding competition “after a year of delayed/canceled projects;” getting projects back on track after “delayed design and procurement;” and “navigating the outcome of this pandemic, not knowing how this will impact the construction industry.”

In conceding that 2020 was challenging but survivable by keeping an eye on the ball, ArchKey’s Scharff perhaps sums up the views of many contractors.

“The biggest challenges we face are the same as any other company in relation to looking at our business model and understanding where we can be more efficient, what markets are facing more pressure as a result of our changing environment, and where we can use our scale and experience to make a difference," he says.

Tom Zind is a freelance writer based in Lees Summit, Mo. He can be reached at [email protected].

About the Author

Tom Zind

Freelance Writer

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].