Big Year on Paper: EC&M’s 2022 Top 50 Electrical Contractors Special Report

It’s unlikely that 2021 and its swirling economic winds will be remembered as a home-run year for American industry. But one sector tore the cover off the ball — accounting-wise at least.

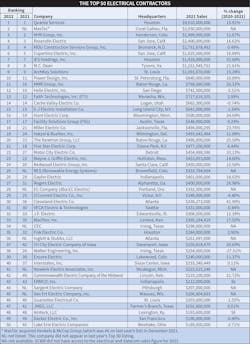

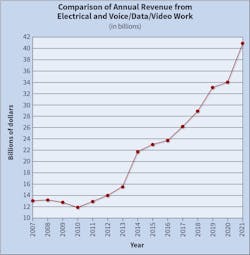

Even as the economy struggled to regain its footing in the wake of the COVID-19 pandemic and inflation, supply chain snarls and labor shortages, companies comprising the 2022 installment of EC&M’s Top 50 Electrical Contractors reported combined record revenues of almost $40 billion for the year (see Rankings Table), a 20% gain over the $34.1 billion amassed in 2020 by the 2021 Top 50 (see Historical Trends Chart). That eye-popping gain may be partly due to the timing of revenue bookings for firms and even the inflation spike, but its sheer magnitude — easily the biggest year-over-year jump in at least 15 years — suggests that, despite speed bumps, electrical contractors as a group have been busier than ever the last two years — from the start of the pandemic, through its depths, and beyond.

Looking back, several Top 50 contractors said 2021 (the calendar year that the 2022 survey is based on) was a period of rebound and reset that brought a surprising amount of success. Others described it as another challenging year.

Tom Schott, president and CEO of Cupertino Electric, Inc., (No. 6) San Jose, Calif., says the company’s 17% revenue gain was possible because it had multiple avenues for pursuing business.

“We’ve mostly recovered from the impact of the pandemic,” he says. “Our diversified approach to markets we serve — and our national presence — means we were able to rebound quickly and has allowed us to realize real growth and opportunity. Some of our markets were hit harder than others, but our diversified strategy allowed us to weather the storm.”

Commonwealth Electric Company of the Midwest (No. 42), Lincoln, Neb., saw its revenues climb 22% in the wake of a disruptive 2020.

“When COVID hit, we saw some significant reaction, mostly in project delays that caused about a 38% drop in some areas like service work and man hours, but that lasted about three months,” says Michael Price, chief executive officer. “But our revenues were back up in 2021, due in part to our geographic distribution across the Midwest and South that gives us good risk mitigation.”

“We thought business would ramp up in the second half last year, but it didn’t happen,” he says. “So, we saw basically no growth year over year. There was increasing competition from other contractors, and we did have to take some tighter-margin jobs to secure work — so gross profit was down too.”

Input insanity

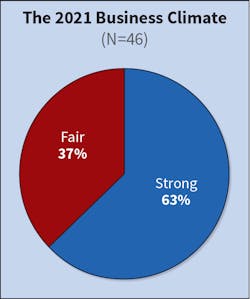

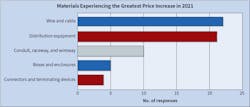

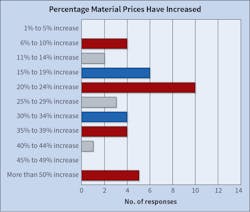

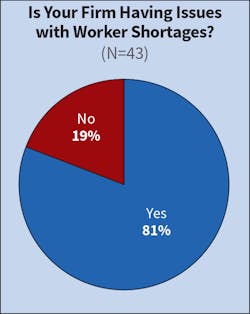

While Top 50 revenues were up, and many firms judged the business climate strong in 2021, there was no shortage of headwinds. After bubbling up in late 2020, severe supply chain problems and material price spikes surfaced in full force as 2021 progressed, complicating project starts, bidding, and scheduling. On top of that, contractors had to contend with the perennial problem of qualified worker shortages — one magnified by the combination of a surge in construction projects and heavy churn/disruption in the national labor force.

“That really stressed the importance of having good relations with suppliers and contract partners,” he says. “And it actually played to our strength as design-build contractors because getting in on a project up-front allows owners to procure long lead-time products earlier and mitigate supply chain risks, rather than waiting for designs to be complete and then placing orders.”

Contractors also described a 2021 environment where a lack of visibility on costs for materials and labor ate into profits and prompted more careful consideration of project opportunities. Schott said Cupertino’s margins remain “under pressure” from inflation, supply problems, and labor shortages and have made it “extremely important that we make sure we’re choosing the right projects and using discretion.” Atlanta-based Inglett & Stubbs (No. 36) saw its revenues rise but struggled to assemble a stable and reliable workforce from a more demanding labor pool and navigate a difficult materials market.

“With input costs growing, we had to tackle that by managing our margins more closely and pricing more aggressively in some cases,” says Gael Perlot, vice president. “We saw more projects going to the guaranteed maximum pricing format, so we had to add to our staffing on the accounting side.”

The hot stay hot

Those spiraling costs, combined with pricier labor and rising interest rates, made construction more expensive in 2021. That iced some projects, but many others moved ahead regardless, benefitting electrical contractors. For those properly positioned (able to take advantage of economically well-situated markets capable of absorbing higher construction costs), 2021 was a year to restore revenue streams and pad backlog.

Once again, the action for electrical contractors seemed centered in data centers/mission critical and health care, two markets that close to half of those surveyed included in their list of hottest markets for 2021 (Table 1). Both markets have been No. 1 or No. 2 on the hottest list for the last several years, while manufacturing placed third for the second consecutive year. As for cold markets (Table 2), retail, private office, and hospitality topped the list, closely mirroring last year’s ranking and offering further evidence of COVID-19’s lingering chilling effect on construction demand in possibly pandemic-scarred sectors.

“The office market has cooled down drastically, and hospitality too,” says Anthony Mann, CEO of E-J Electric Installation Co. (No. 15), headquartered in Long Island City, N.Y. “But the warehouse side of retail has been hot — the big distribution centers. And health care, which responded to COVID, is now getting back into a lot of its longer-term projects and driving forward on those. We also see some more opportunities coming in renewable energy and transit and airport work.”

“No one is building office space, and retail is still slow, though we’ve had strong years before in that,” he says. “The strong highlight today is mission critical projects. Data center construction seems to be recession-proof.”

More government work is on Guarantee Electrical’s radar as a possible bulwark against a construction recession. Arb says that work has grown partly because more of its long-time general contractor partners are securing government contracts. More of that work is coalescing in Colorado — Air Force base projects and a NORAD facility recently – prompting the 2021 acquisition of Berwick Electrical in Colorado Springs.

“A larger percentage of our backlog is in federal work; it now stands at about 30%,” he says. “It’s an emerging market for us, while we stay strong in areas like water, health care, and distribution and logistics facilities.”

When it does come, much of that work will likely flow to market specialists, but Schott says established companies with strong performance track records like Cupertino could be positioned to expand their portfolios via the funding push. The company, he says, has slowly leveraged its size, scale, and ability to execute to push into the public infrastructure market, where markets like water treatment and transportation are ripe for upgrades. That “separates us, and we’ve been positioning ourselves to do more of that work for the last few years.”

Spiking optimism

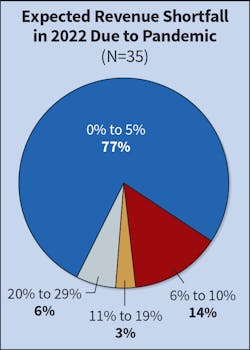

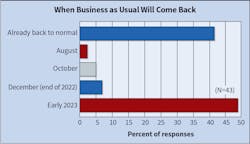

Meanwhile, the impact of the pandemic on business seems to be steadily fading. Fewer expect pandemic-related revenue declines greater than 10% in 2022; 91%, however, see lingering effects of up to 10% on revenues (Fig. 14), roughly in line with last year’s results. Still, half the companies surveyed seem to say business is not back to pre-pandemic normal just yet, but that “business as usual” will resume early next year. Many (42%) surveyed last year said business was back to normal in late spring 2021. This year, 37% said it was already back to normal (Fig. 15), suggesting that some may have been premature in their assessments.

“We’ve seen tremendous margin erosion based on the contracts we had in place,” he says. “Inflation has killed us, but the good news is that now these higher costs are in contracts so our margins should increase from where we are now.”

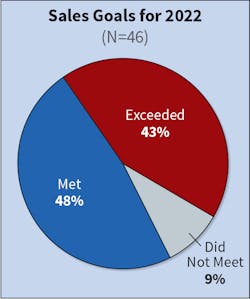

The company’s volume of business seems to be growing as well. From January through June, Goodrich says, backlog goals were exceeded. In July, however, they fell by 6%.

“I’m concerned we could be slowing, but it won’t affect us for 2022 revenues,” he says. “Next year could be flat.”

The economic backdrop also has the attention of Frank Musolino, CEO at Power Design, Inc. (No. 10), St. Petersburg, Fla., but the design-build firm’s concentration, expertise, and relationships in the growing multi-family residential sector is a bulwark against an uncertain market outlook. Despite rising construction costs, demand for multi-family and mixed-use residential/commercial construction looks strong and sustainable, he says, provided the economy stays out of anything but a shallow recession that could lead to higher unemployment.

“We’re sitting down with clients to look into the future, help them project their needs, and get into the queue on materials,” he says. “Some health-care clients are bringing us in earlier on because they’re aware of lead-time issues and the need to get engineering done faster.”

New manpower wrinkle

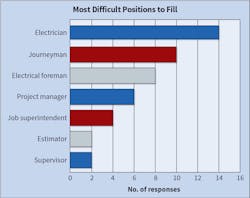

That will take skilled and professional labor, of course, a commodity that could continue to come at a premium in the current economy. Workers of all types might be in shorter supply due partly to a near unprecedented labor market upheaval, bad timing for an industry that has seen demand accelerate.

Cupertino’s Schott says the labor squeeze is as tight as ever, covering front-line field electricians to back-office project managers and support staff. To combat the problem, the company has ramped up efforts to burnish its image as a progressive employer.

Interstates is also squeezed front to back on labor, not a big change from previous years but feeling the press of the so-called “Great Resignation” phenomenon that may be drawing experienced people out of the labor pool, Van Egdom says.

“With turnover seemingly higher than it’s been, that adds to the challenges of both retaining and attracting new talent,” he says.

Gaylor Electric is attacking its “quality” labor pipeline deficit partly on two novel fronts: carefully crafted high school partnerships to identify and groom students for its apprenticeship programs and repurposing retiring employees to serve as teachers and mentors for young craft employees.

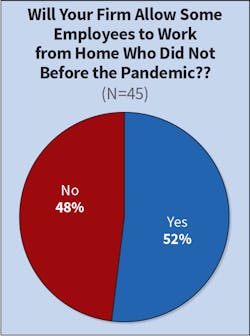

A tool contractors might employ to ease the recruitment challenge for some jobs is hybrid work arrangements. Accelerated during the pandemic, remote and remote/on-site blend structures could become workplace fixtures after technologies allowing online collaboration and sharing proved highly capable. Offering job candidates such flexible work options could be a way for contractors to expand their geographic search maps and lure talent reluctant to pull up stakes or be latched to an office.

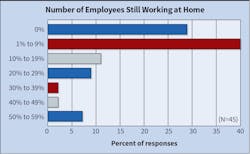

Contractors don’t seem to be on the same page when it comes to the feasibility of those arrangements. In a slight shift from last year, Top 50 contractors, by a narrow margin, say they’re permitting some former office-based employees who shifted to working from home fully or partially during the pandemic to continue doing so (Fig. 21). But those who are permitting it are being selective. About 70% offer the perk to less than 19% of their workforce (Fig. 22).

Technology’s lure

Unrelenting labor challenges find more contractors, Interstates included, turning to technology to mitigate the effects of manpower and talent shortages. Van Egdom says the company is exploring more deeply IT tools, including generative design, robotic process automation, and technology-aided prefabrication processes that can improve efficiency in design and project execution management — hopeful they can supplement or supplant some labor over time.

“Technology and automation are definitely a component of the solution to the labor issue that we continue to invest in,” he says. “Taking more work off site to a manufacturing environment is also an element of mitigating peak labor needs.”

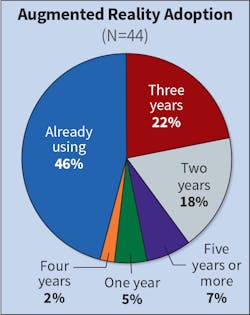

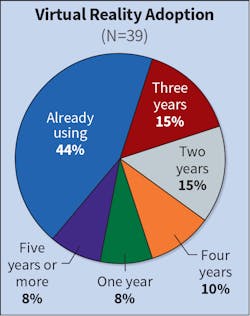

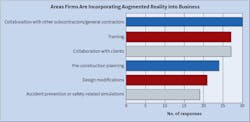

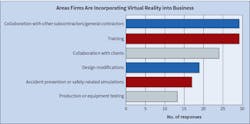

Inglett & Stubbs is still feeling its way through the AR and VR world, slowly embracing the tools as more projects incorporate them, and their potential benefits become clearer. Perlot is drawn to their seeming power to better unite design and construction phases, accurately monitor progress, and minimize costly problems that stem from miscommunication.

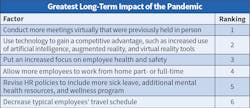

The ability to bring ever more powerful IT tools into all phases of work continues to open new efficiency and performance horizons for contractors. In particular, the growing power of mobile devices and the software they can utilize has continued to make field operations more nimble, informed, and capable in execution and oversight. Their importance is evident in the top ranking that “field apps and software” has on the list of topics contractors believe employees need the most training support on (Fig. 28). That may be because they have so many regularly used functions vital to operations — from top-ranked project management, time management and tool management to job costing/estimating, codes and standards guidelines, and inventory tracking (Fig. 29). And contractors point to a range of specific useful job-related information that employees are accessing on mobile devices, with product specifications and codes/standards requirements topping the list (Fig. 30).

“On-the-ground technology that can access information through the cloud gives us remarkable capabilities,” he says, which are needed because, “as technological advances in construction have pushed construction schedule timelines from where they used to be, expectations have followed suit to the point where we have to do in a week some things that used to take a month.”

As central participants in almost any construction project, electrical contractors will need to take advantage of every technology-aided tool at their disposal to take full advantage of what looks like a full slate of opportunities stretching to the long horizon. Coming off an incredibly strong year of revenue growth tainted by profit challenges, Top 50 companies face a near-term future that looks hazy at best due to the very mixed signals the broader economy is sending. By any measure, though, top contractors delivered at least a mild surprise in a 2021 buffeted by no shortage of economic headwinds and uncertainty. Can they deliver again in a year equally (if not more) economically perilous? Stay tuned.

Tom Zind is a freelance writer based in Lees Summit, Mo. He can be reached at [email protected].

About the Author

Tom Zind

Freelance Writer

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].