Resilient Revenue: EC&M’s 2023 Top 50 Electrical Contractors Special Report

Even when times are hard, good times can often roll on. A collection of the nation’s largest electrical contractors showed that’s possible by registering a solid percentage revenue increase in 2023, even in the face of significant supply chain and inflation pressures that brought higher materials and labor prices, shortages, and delivery delays.

The contractors who make up the 2023 EC&M Top 50 by self-reported prior year electrical and voice/data/video revenues brought in $43.901 billion in revenue as a group in 2022 (see Rankings Table). That was up 7.4% from $40.889 billion reported by last year’s Top 50, a number that was 20% higher than the 2021 Top 50’s Covid-tarnished revenues of $34.1 billion (see Historical Trends Chart).

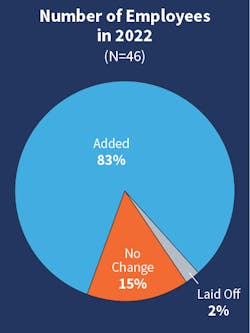

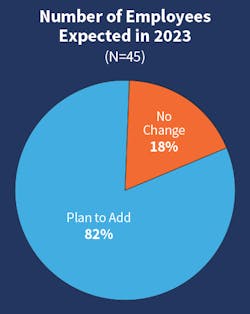

Although 16% of companies reported revenue declines in 2022 — and many alluded to supply chain headaches in EC&M’s Top 50 contractor survey of business conditions and concerns — three-quarters judged last year’s business climate strong (Fig. 1). The 2022 Top 50 business climate reading was 63% strong for the prior year; the year before — for 2020 — it stood at just 37%. A big factor in that assessment boost might have been the element of surprise: For the first time since 2019, a majority of firms said prior-year revenues exceeded expectations (Fig. 2).

At Cupertino Electric, Inc. (No. 6), San Jose, Calif., 2022 was a solid year in which expectations were generally met and revenues ticked higher, giving the company a two-year growth rate of 5% to 10%. President/CEO Tom Schott says the firm’s heavy involvement in three core sectors provided a mixed bag of performance, but one that yielded a steady flow of work.

“Continued softening in the commercial market was a problem area, but data centers and energy stayed strong as it has the past few years for us,” he says. “Interest rates and inflation presented some problems that led to some general caution in the market and companies maybe not expanding as much as they’d like. Cost of construction was a factor.”

Reporting one of the highest Top 50 revenue growth rates for 2022, MDU Construction Services Group, Inc. (No. 4), Bismarck, N.D., enjoyed strong demand in the utility, mission critical, and high-end manufacturing segments and benefitted from a presence in centers of torrid growth.

Five Star Electric Corp. (No. 42), Ozone Park, N.Y., although low bidder on many large-scale public bids, has seen reluctance of owners/agencies to move forward and award many of these projects. Rising construction and borrowing costs combined with supply chain issues and extended material/equipment lead times have presented many of these clients with financial and political headwinds, says Russ Lancey, president and CEO.

“We had a good year overall, but given the macroeconomic challenges, we endured a lot new projects being delayed, canceled, or going out for rebid.”

Profit challenge

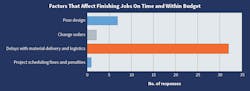

Higher and more unpredictable materials and labor costs, contractors say, have made attempts to squeeze out higher profits more difficult. For many operating in 2022, the primary goal was not to take stinging hits by failing to factor in that volatility and uncertainty. Of eight factors possibly compromising a firm’s ability to complete jobs on time and within budget, material delivery delays and logistics was the largely unchallenged top choice (Fig. 4).

“It’s hard to generalize on our approach, but our bids didn’t necessarily have higher margins built in,” says Rob Smith, president of Sargent Electric Co. (No. 47), Pittsburgh. “It was more about contingencies. There was more time spent on understanding the potential impact of the cost environment — labor pressures and unit cost factors — we were operating in.”

Guarantee Electrical Company (No. 33), St. Louis, had some success in margin expansion, the result of careful analysis and strict adherence to procedures, says Nick Arb, vice president of market strategies.

“We have robust internal processes that help us evaluate many factors,’ he says. “Knowing our internal capacities is key, our geographic location and available workforce, our relationship with clients, and the potential profitability. It’s always about mitigating risk of the unknown using all the available information to protect yourself.”

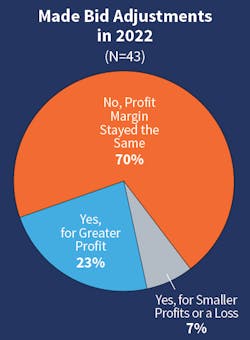

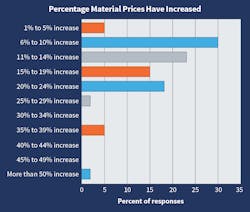

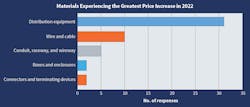

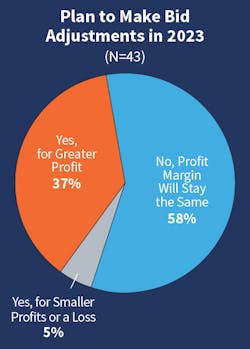

Looking ahead to 2023 and its possible profits picture, contractors see cause for more optimism, possibly stemming in part from more supply chain certainty. After the biggest share of last year’s Top 50 saw prices rising on their most volatile material (wire and cable named by the majority) between 20% and 24% in 2022, this year two-thirds (Fig. 5) see that material (distribution equipment selected by most, as shown in Fig. 6, rising between 6% and 19% in 2023. That expected moderation could partly explain why more than a third say they’ll look to adjust bids for greater profits this year (Fig. 7).

Willis Wiedel, CEO of Encore Electric (No. 38), Lakewood, Colo., sees evidence of supply chain stabilization and moderating prices and the prospect of a more profitable and predictable 2023. If that proves to be a mirage, though, the company still sees a path through the turmoil.

“Things feel like they’re getting better compared with a year ago, with the escalation in prices having stabilized some,” he says. “But we’ve also learned how to manage the supply chain issues better, and we have to continue to do that.”

Schott also sees signs that supply chain snarls that disrupted project timelines are easing, improving prospects for smoother jobs with fewer potentially costly surprises.

“It’s hard to not have some margin erosion when you have projects that have to pause, but we’ve been able to come up with some creative solutions to keep projects moving,” he says. “The worse may be over on supply chain issues, but we’re not completely out of the woods.”

Backups, delays impactful

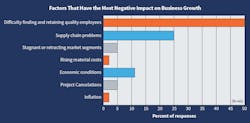

Contractors can only hope that’s the case because material shortages and delivery delays apparently exacted a toll in 2022. Of possible factors exerting the greatest short-term impact on business (see Fig. 8), supply chain issues got the clear nod as the most problematic, followed by delayed and canceled projects. No other listed concern drew any votes, suggesting the three were somewhat intertwined and dominant in terms of impact.

MDU, in line with its emphasis on heavily utilizing data in project planning, has studied the impact of Covid-related delays and cancellations and supply chain constraints on its operations. The conclusion is that problems in receiving materials can produce consequential ripple effects, Thiede says. While the situation has improved, the company is still contending with project delays.

“The best thing we can do is leverage our purchasing power and the integrity of our purchasing practices and lean on/talk with suppliers early and often,” he says. “We continue to get better at managing it.”

Sargent saw projects stalled for a variety of reasons in 2022, “a lot associated with the supply chain,” says Smith, but also for feasibility reassessment. They were disruptive, but the silver lining in some delays was the chance to work with clients to revisit hastily drawn up project designs.

“We were seeing more clients waiting to commit and then scrambling to put projects together,” Smith says. “With supply chain issues and longer schedules, we can sometimes convince customers to go back and get better engineering packages.”

Expecting growth

With the current fiscal year-end looming, Guarantee Electrical’s Arb sees a big revenue number coming, a result of a recent geographic expansion effort paying dividends and strong organic growth in some key sectors. Moving into 2024, though, he’s factoring in the risk of an economic downturn that would bring a tapering of that growth. An early sign is data pointing to a slowdown in projects-in-design.

“We continue to see high-quality project opportunities in various market segments, although the volume of opportunities appears to be slowing,” he says. “Refining an approach to pursuing the best work available will be critical.”

Hunt Electric Corporation (No. 16), Bloomington, Minn., is ahead of pace on 2023 revenues but is also cautious about the future, given the potential for lagged impact of higher interest rates on project commitments, says John Axelson, president and CEO. Tempering that concern, for now, is a strong continuing revenue stream from extended duration projects and established clients.

“We’re lucky to be involved in some hyperscale (billion dollar-plus) projects that have driven our growth,” Axelson says. “We have a handful of them, in areas like mission critical and battery manufacturing. Everyone, though, is wondering about a recession, and so we could see some downturn next year.”

Working in contractors’ favor looking ahead is the fact that electrical is a target-rich environment. The push for electrification and all that entails — grid renewal, electric vehicle charging infrastructure, battery production — along with a manufacturing renaissance, a growing health-care economy and a renewable energy push, puts electrical contractors at the center of the action.

Hot markets still sizzle

Likewise, MDU is being drawn into changes occurring in the energy markets. A transmission and distribution market specialist, the company is working on more utility transmission system upgrade work.

“There are some growing opportunities in West Coast undergrounding of service, with PGE undertaking a big initiative in the San Francisco area,” Thiede says. “Transmission line reconductoring is another area where we see some emerging opportunity.”

Commonwealth Electric Company of the Midwest (No. 30), Lincoln, Neb., sees continued strong demand for mission critical work — new and upgrades — in its Nebraska/Iowa and Arizona/Utah operational hubs, says Neil Davidson, executive vice president. But other markets beckon.

The markets picture for contractors could become cloudier if economic recession fears are realized. A steadying factor could come in the form of pre-committed public infrastructure spending. Most Top 50 firms, though, see limited near-term benefit.

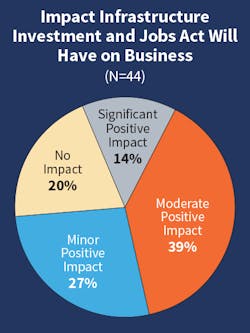

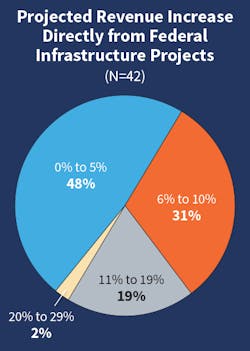

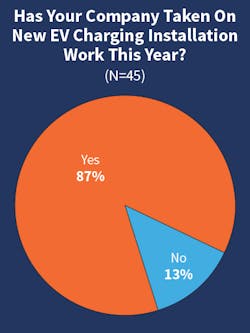

Two-thirds see the Infrastructure Investment and Jobs Act (IIJA) having at best a moderate positive impact on their business (Fig. 11) in 2023. If any 2023 company revenue can be tied directly to spending under the act, roughly half say it will be miniscule, and half say it could be in the 6% to 19% range (Fig. 12). Projects most likely to produce that revenue (Fig. 13) are electric vehicle charging infrastructure, renewable energy, and electric grid updates. Given the act’s goals, EV infrastructure work may be the most accessible for the average contractor, and the survey confirms it. Most said they’ve handled such work recently (Fig. 14). But 85% say 2023 revenue tied to that work won’t exceed a 5% share.

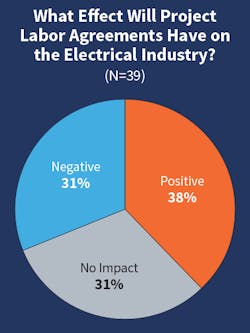

Infrastructure work funded through the act, though, could come with some caveats for contractors. Many projects will likely require all contractors to sign on to project labor agreements (PLAs) that would subject them to rules laid out in an executive order mandating them on many federally funded infrastructure projects. Non-union contractors are balking at the PLA requirement and could be reluctant to take on infrastructure work that requires the agreements. Top 50 contractors were split on their view of PLAs, with roughly a third each (Fig. 15) saying they’d be a positive, a negative, or of no consequence for the electrical industry.

Encore’s Wiedel doesn’t see much immediate benefit from infrastructure upgrades, nor long-term upside because that’s not a focus specialty. Some EV charging station work has come the firm’s way, but only as a supplement to facility construction. Other infrastructure-like projects have filtered in, but they haven’t stirred excitement.

“There’s a battery plant we’re handling in Colorado, but I’m nervous about that industry because the technology is changing so fast,” he says.

“A few years ago that was just onesie-twosie type work, but now it’s more of a pure play where we’ve done entire campuses involving dozens of charging stations and associated infrastructure,” he says. “To accommodate that additional load more generation is needed as well as upgrades in switchgear and distribution.”

Though cautious on 2023 revenues, Five Star Electric is seeing signs that the infrastructure spigot is opening. “A record number of new opportunities are starting to hit for us,” Lancey says. “We’ve come out of the post pandemic slowdown and are seeing many publicly funded project opportunities on the horizon.”

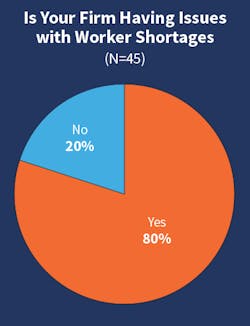

Labor worries persist

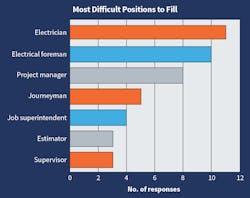

“We could bid more work and build our backlog if we could consistently find the labor we need,” Davidson says, noting Commonwealth Electric’s greatest needs are journeymen and project managers. Entry-level slots are somewhat easier to fill, he says, but that entails the “long game” of hiring and training that requires a strong commitment to steadily cultivating a workforce.

Hunt Electric’s labor challenges vary, with field workers abundant in some regions and scant in others, and slots like project managers and senior estimators a struggle to fill but modelers and BIM experts easier. One way the company is working around the field labor issue, Axelson says, is employing more prefab where union rules permit, building components off site and shipping to areas where the skilled labor pool is shallower.

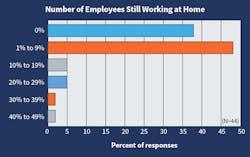

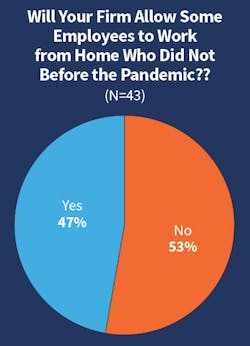

The complexion of labor availability and management issues for contractors has changed in the wake of the Covid pandemic, which necessitated more remote work in some job classifications. The ability to design more jobs that require minimal in-person, in-office collaboration has opened the hiring lens for more contractors and yielded some productivity benefits. Still, contractors may be slowly moving away from remote work; most Top 50 contractors say only a fraction of their employees who had started working from home were still doing so (Fig. 21). Yet half say (Fig. 22) they’re letting formerly office-bound employees continue working from home on a full- or part-time basis.

“We started offering remote as an option before Covid, and we’re continuing it,” he says. “On our BIM modeling side, it’s allowed us to hire more people. We have to try to understand what different generations in the workforce are looking for.”

At Cupertino Electric, about a third of non-union support workers are in hybrid setups, a good compromise that puts most headquarters personnel in the office two to three days a week.

“More time in the office is probably better for our culture, but remote can help us attract and retain,” Schott says.

Integrating technology

Guarantee Electrical continues to explore emerging technologies that could move the needle.

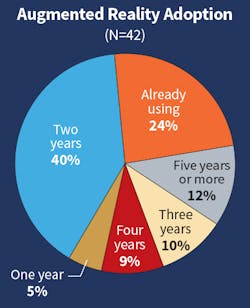

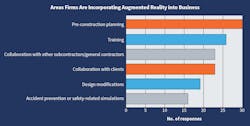

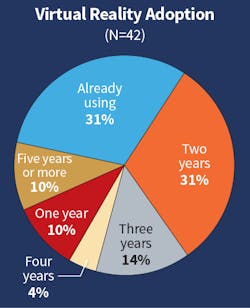

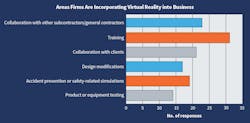

Sargent Electric’s Smith says AR and VR hold some promise and are being used with some clients for BIM modeling and training. And AI could be helpful in data mining that could improve areas like project planning and manual preparation.

“All new technology takes longer to gain widespread deployment than people anticipate,” he says. “But Apple’s new AR offering, VisionPro, could help make that more mainstream.”

Technology in its most basic, well-established form continues to make a difference for contractors, but it demands attention as it evolves. Of various areas contractor employees might need better training in, field apps and software was the overwhelming choice (Fig. 28) of the Top 50.

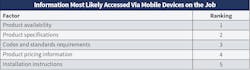

Encore Electric views mobile devices as a critical conduit for getting all types of vital information to workers, most members of the “generation that does so much on mobile devices,” Wiedel says. That understanding has expanded Encore’s appreciation for how they can be utilized beyond relaying shop drawings and installation specifications. Information on managing mental health, substance abuse and addiction — critical issues for construction workers — can be easily relayed to employees, 70% of whom are in the field. “We’re able to meet our people where they are,” he says.

More advanced procurement and tool management software geared to electrical contractors is giving Hunt Electric more reason to embrace technology.

“We’re finding more and more meaningful software,” Axelson says. “Early on, a lot of it was out there without knowing how it would help. Now we’re finding more options for use in working with real time models, materials management and purchasing and safety.”

Further adopting and adapting technology to electrical construction is only one of many issues on the plates of electrical contractors. They’ve been tested in the last year by unprecedented supply chain problems, inflated prices for materials and labor, project delays, and growing economic uncertainty. In their own words, contractors lay out a grab bag of challenges they face: “increased competition”; “incomplete construction documents”; “qualified supervision”; “proficiency in mission-critical projects”; “interest rates affecting private sector spending”; “economic slowdown that will put pressure on pricing”; “staying current with the latest technological advancements and the employees to run them.”

Yes, the future is uncertain. But by all measures, the Top 50 survey included, electrical contracting most assuredly has a future.

Tom Zind is an independent analyst and freelance writer based in Lees Summit, Mo. He can be reached at [email protected].

About the Author

Tom Zind

Freelance Writer

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].