Amped Up: EC&M’s 2025 Top 50 Electrical Contractors Special Report

Key Takeaways

- EC&M's 2025 Top 50 Electrical Contractors posted a 15% revenue increase in 2024, reaching $59.5 billion, driven by high demand in data centers, energy, and digital markets.

- Most firms reported strong business climates, with 75% exceeding revenue expectations, despite challenges like labor shortages, material costs, and policy uncertainties.

- Contractors are increasingly adopting advanced technologies such as AI, AR/VR, and sophisticated project management tools to improve efficiency and competitiveness.

- Uncertainty around federal funding and tariffs is influencing project planning with many firms preparing for potential delays and cost increases in 2025.

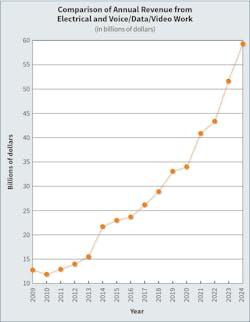

In a year that may prove to have been the calm before a storm of disruptions to the economic status quo, the nation’s leading electrical contractors levered an overall favorable construction climate to post revenues of $59.5 billion in 2024, topping last year’s total by 15%.

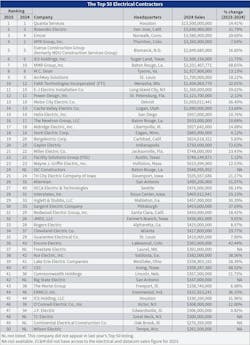

All but three of the 50 firms that make up EC&M’s 2025 Top 50 Electrical Contractors (see Rankings Table) — a distinction based on prior year revenues reported in its annual proprietary survey — posted revenue gains for 2024, helping keep a recent string of record-setting years for the Top 50 alive (see Historical Trends Chart). Double-digit gains proliferated, several topping 50%, indicative of broad high demand for their services in a building boom taking its cues from a largely strong and resilient economic backdrop and the steady march of nothing short of a revolution in digital technology.

Most Top 50 firms rated 2024 a solid year on several key measures. But it was one in which both persistent and fresh challenges complicated the picture. From labor shortages and inflated material prices to project design and execution lapses to a lack of clarity on funding and the integration of new technologies, contractors had to again navigate seemingly rising levels of uncertainty and change.

And on that score, there’s likely no light at the end of the tunnel. Moving through early 2025, contractors were expressing some caution about the future, stemming from worries about the impact of a grab-bag of newly or increasingly relevant economic factors, some linked to policy priorities of a frenetic Trump administration: tariffs, trade, immigration, interest rates, energy, taxes, regulation and artificial intelligence. See “The Impact of Economic Policy Uncertainty on the Electrical Industry.”

Flying above turbulence

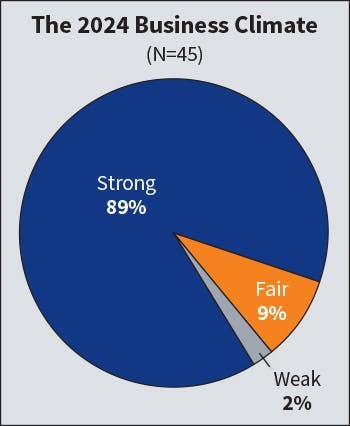

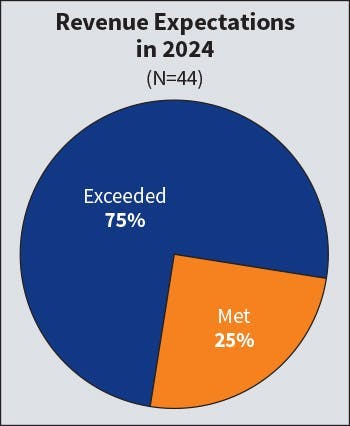

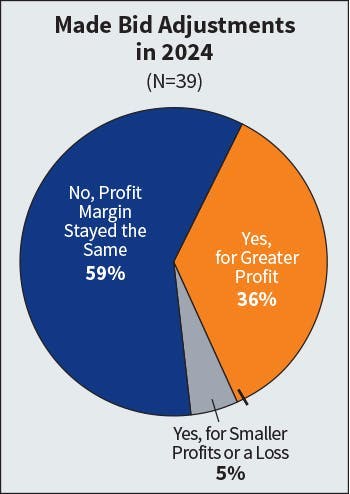

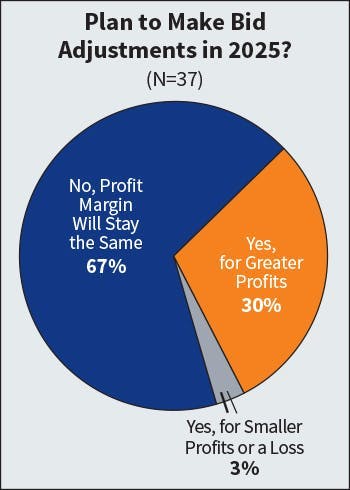

Generally speaking, contractors said last year was a good one for plying their trade. Nearly nine in 10 judged the 2024 business climate to be a strong one overall (Fig. 1). Robust top-line growth drove that assessment, but more so perhaps, upside surprises. Seventy-five percent of contractors, the highest share in years and 17 points higher than last year’s Top 50, said their prior-year revenues beat expectations (Fig. 2). But the revenue boost, aided by more business to pursue, didn’t change their bid strategies. Like last year, only about a third said they adjusted bids for higher profits (Fig. 3). The year was a good one for many companies, but some say it would have been better if not for creeping uncertainty.

Riding several high-growth construction markets like data centers, energy infrastructure and semiconductors, revenues rose 69% at MMR Group, Inc. (No. 7), Baton Rouge, La. President and CEO James B. Rutland said the company pushed through a cloud of substantial client reticence to spend by staying “disciplined, diversified, and ready to move where our clients needed us most.”

That flexible approach helped the company navigate a business climate it termed only fair. Uncertainty around the presidential election and future policy implications caused many clients and investors to hold off on large-scale capital project spends, says Business Development Manager Matt Allen. “As a result, the market remained cautious throughout the year, with much momentum deferred until after the election cycle concluded.”

E-J Electric Installation Co., (No. 11), Long Island City, N.Y., also powered through obstacles that made for a tougher business climate. Its fiscal year revenues grew 60%, partly through two acquisitions but also from securing large-scale data center and infrastructure projects in new geographies, says President Anthony Mann. The company demonstrated an ability, he says, “to manage complex projects at a national scale” while navigating “labor shortages, material delivery impacts, rising material prices, tariffs, and occasional project cancellations.”

A big data center debt

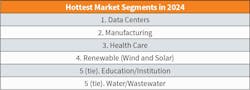

Little, though, distracted contractors invested in the most active markets, a list indisputably crowned by data centers. Eighty-six percent of contractors put that sizzling market, fueled by the spread of artificial intelligence, on their list of their firms’ three “hottest” markets (Table 1), a 17-percentage point gain from last year and 47 points ahead of this year’s runner-up (manufacturing). Other markets on the hot list again included health care and renewable energy. Education/institution broke into the top five, while power fell out. Big movers on the list included public building (down 11 percentage points from last year); manufacturing (down 10); power (down nine); and pharmaceutical (up seven).

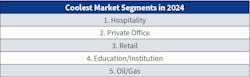

There was some churn in the slow-market rankings (Table 2), but the top-laggard list stayed mostly constant. Hospitality moved up to the top spot, ahead of private office, retail, education/institution and oil/gas. Movers included education/institution and oil/gas (each up 12); water/wastewater (up nine); private office (down 11); residential (down 10); and retail (down eight).

Ahead of its spinoff as a separate company from MDU Resources in November, Everus Construction Group (No. 5), Bismarck, N.D., sharpened its focus on key markets. Eleven of its 15 operating companies are electrical contractors, many continuing to double down on markets benefitting from megatrends, such as data centers, grid modernization, and high-tech reshoring. But the newly independent company is also looking to score in a variety of markets by expanding access to knowledge and experience across its operating units.

“There’s strong demand for specialized expertise in areas like data centers and health care, complex jobs that demand companies with resources and experience,” says Jeff Thiede, president and CEO. “But we’re diversified and working on cross-training people and sharing resources/best practices to help our companies look at other trending markets.”

An abundance of data center, mission-critical, and water projects just in its own Texas backyard has sharpened the focus of Alterman, Inc. (No. 26), San Antonio. President/CEO Greg Padalecki has moved to solidify its presence in those booming markets, seizing the opportunity to take profitable work that’s seemingly dropping in the lap of qualified firms.

“We’re not battling with competitors over projects like office buildings or hotels as much anymore,” he says. “Now we’re doing projects that aren’t as sexy, barns full of servers, but there’s a lot of this to go around. If you’re in the MEP space, you’re in the right place these days.”

Pittsburgh-based Sargent Electric Company (No. 30) is preparing to be nimbler when it comes to targeting markets, says President Rob Smith. Stalwarts, like data centers and utility power, look to have legs, but renewable energy is now an open question. Others (like manufacturing) and, notably, steel, could pop while others more linked to consumer spending trends could be vulnerable.“It’s making us look more closely at our priorities and flex to where capital spending is occurring,” he says. “That’s not new, but we do expect to do more different work than in the last few years.”

As an example, power plant construction could expand as AI drives power demand, but more might be distributed energy projects utilizing renewable gas or, eventually, nuclear, he says, evidence that “picking winners and losers” may get more challenging.

2025 flashes yellow

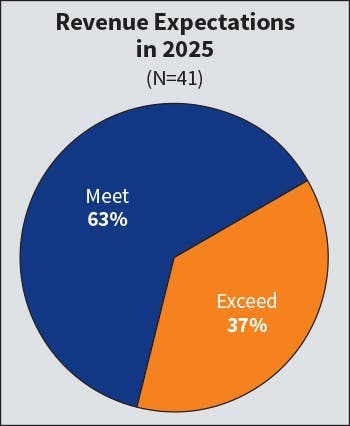

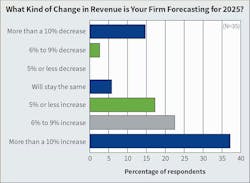

That changing market for electrical services, coupled with concern and uncertainty about the economy, might be helping temper contractors’ views about business in 2025. In an eye-opening shift, the share of contractors expecting revenues to exceed expectations (Fig. 4) this year fell 20 points. Last year, 57% said they thought 2024 revenues would beat expectations; this year 37% thought they would.

Coming as notably more contractors said their revenues surprised last year, the drop suggests many think a sharp change in fortunes could be at hand or at least growing doubt about the prospects for an upside surprise. The smart money may be on the latter because 60% see healthy current year revenue growth (Fig. 5) of at least 6% — 10 points above last year.

More evidence of slowdown fears shows up in expectations for changes in bidding and margins. Thirty percent said they thought they’d be adjusting bids for higher profits this year (Fig. 6), down 14 percentage points from last year. Most expect no change.

Houston-based ICS Holding, LLC (No. 45) saw the year start slowly, but later regain some momentum. Fresh off the promise of an injection of capital from a private equity deal in January, its operating companies saw some prospects tapping the brakes in the first quarter.

“All those uncertainties around tariffs, the course of interest rates and funding squashed together with all of the geopolitical backdrop has really led owners to pause,” says Cory Borchardt, CEO. “Not a lot of cancellations, just some delaying, telling us to just be ready.”

Oil and gas projects, a staple of some firms, were “very rocky the first half of the year,” he says, due to tariff and regulatory uncertainty. Manufacturing projects, though, have stayed strong, as have education and healthcare and other markets that offer good prospects for ISC firms that tend to steer clear of megaprojects — those with at least a $1 billion price tag. Such projects, though, are becoming the bread and butter of more contractors, among them MMR. A strong data center market helped it hit the $1 billion mark in current year bookings in May, Allen says, putting it on track for a $3 billion year, well ahead of last year’s $2.3 billion. Building those data centers, and powering them, too, more with on-site generation, is seen supplying long-term opportunity.

“We’ve built relationships with those clients, and that’s maybe the hardest thing to do,” Allen says. “At the beginning, they didn’t know who we were, but now they know our culture and quality of work and they’re trusting us.”

Prospects for sprawling infrastructure megaprojects, some with big slugs of electrical, looked good during the Biden administration. But the Trump administration acted quickly to gut much of the enabling legislation passed under Biden, leaving the question of critical federal spending commitments hanging.

Funding stream worries tempered

That’s cause for concern, some contractors say. Slightly more than half agreed disrupting funding through the Infrastructure Investment and Jobs Act (IIJA) and the Inflation Reduction Act (Fig. 7) would have some negative economic impact on federal construction projects this year and next. But a third said it would be only minor, while a quarter expected no impact.

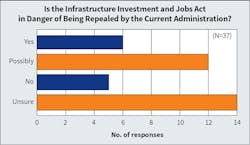

A death blow to the IIJA, in the form of a complete repeal, could come, and the prospect of seeing $1.2 million for transportation and infrastructure spending through 2026 gone could be unsettling. But most contractors don’t know what to make of that (Fig. 8); 70% said they were either unsure of its fate or said it was merely a possibility.

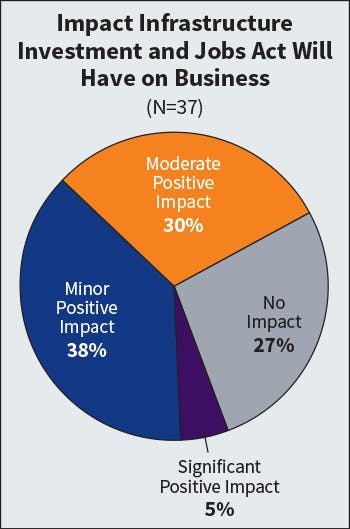

In terms of their own business, contractors don’t seem to have much riding on the question of federal support for infrastructure. More than a quarter see no impact this year from the IIJA (Fig. 9), up 13 percentage points from last year. But many do report having some stake in it; 68% see a moderate or minor impact this year. Yet those who are now benefitting from federal infrastructure spending may not be heavily invested in its fate. Sixty-five percent placed the boost to new project revenue in 2025 at no more than 5% (Fig. 10).

Growing concerns over funding are a component of the uncertainty that E-J Electric is contending with, but they’re not likely to pose an unmanageable threat, Mann says. Some projects have been cancelled for that and other reasons, but many key infrastructure projects will ultimately find a way to get done.

“Project cancellations are often tied to funding changes either politically or privately within institutions, and shifting federal policies are on our radar,” he says. “The IIJA offers opportunity but also some uncertainty in how funds are allocated regionally. We’re proactively planning across regions, leveraging our national scale to balance risk and seize opportunities as they arise.”

Rising costs on the radar

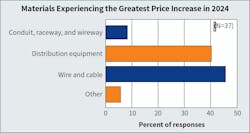

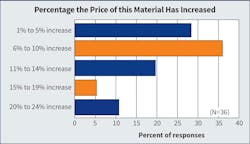

Threats to the funding stream for future projects are a real concern for contractors. But a more immediate one might be the cost of materials, and the sudden emergence of the tariff issue has only compounded that worry. Thirty-seven contractors said they experienced materials price increases in 2024, down from 40 last year. Those increases were heavily concentrated in wire and cable and distribution equipment, the survey found (Fig. 11), and increases were largely in the range of 1% to 10% (Fig. 12).

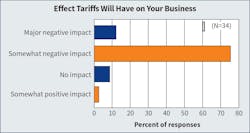

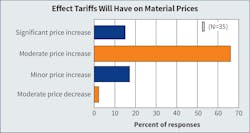

Tariffs may have had some impact on prices last year, but the brunt of it will likely be felt in 2025. It’s hard to quantify now, but at mid-year three-quarters of contractors surveyed (Fig. 13) expected tariffs would have somewhat of a negative impact on their businesses. And if tariffs stick, two-thirds say electrical market material prices are likely to rise moderately in 2025 (Fig. 14).

Tariff uncertainty has compounded the materials price inflation and availability problem that predates the Trump administration, says Sargent Electric’s Smith.

“The reason for project delays is the economics,” he says. “Higher prices for everything — concrete, steel, labor — has caused some reevaluation. If everything has gone up, you’ve got to either put it back in the box or go back and rework it. So we’re seeing more value engineering to take costs out.”

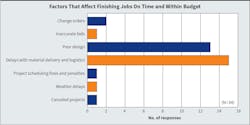

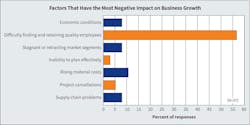

While tariffs and their potential impact are problematic, they aren’t a crisis in the view of Everus Construction Group’s Thiede. He notes the industry had a dry run when the pandemic brought supply chain and cost problems that, while still present, were worked through. Contractors, however, do say delays with materials and logistics remain the top obstacle to getting jobs done on-time and within budget (Fig. 15); just edging out “poor design,” 44% say those delays are the chief problem, though that’s down 19 points since last year, indicating progress. Now, with tariffs, it’s time to get creative again.

“How we mitigate this is working daily with our suppliers to try to anticipate pricing, continue monitoring the market and update our costs,” he says. “More cost-plus, fixed price, and master service agreements are needed as well as communication to make sure we’re being proactive in managing risk.”

Labor pressures confound, but tick down

Tariffs are a new wrinkle in a contractor cost picture that has been dominated by labor. The supply and demand picture for workers has long been imbalanced, giving contractors a dual problem of rising wages and tighter supply. When asked in the survey to name their greatest business challenge over the next few years, most mentioned something related to labor — shortages, cost, quality, training, recruiting and the like. But the survey offers some signs that pressures may be easing, though labor remains a top concern.

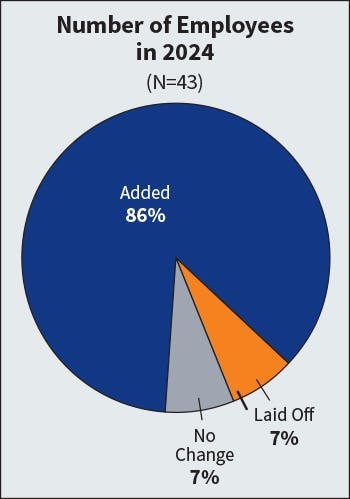

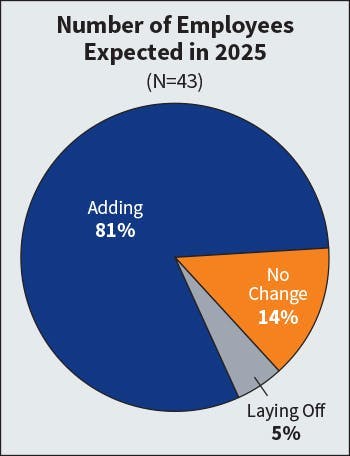

Demand stayed strong in 2024, with 86% saying they added employees (Fig. 16), up six percentage points. But the share saying they expect to add workers in the current year (Fig. 17) fell 10 points — from 91% in 2024 to 81% this year.

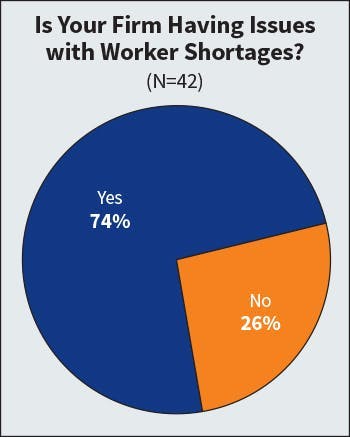

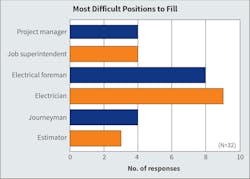

Similarly, the share saying they’re dealing with labor shortage issues (Fig. 18) fell 10 points, to 74%. But staying mostly steady was the belief that difficulty finding and retaining quality employees was the factor most comprising growth (Fig. 19). Fifty-seven percent checked that as the biggest worry, down only slightly. And a range of key jobs are proving difficult to fill, the single toughest again being electrician, up six points in mentions to 28%, followed by electrical foreman (Fig. 20).

Staying fully and competently staffed is challenging Alterman, Inc. Turnover of an increasingly “less tenured” workforce is “off the charts,” says Padalecki, complicating his efforts to fully exploit strong demand.

“It’s not kept us from growing but added challenges,” he says. “We’re managing a younger and what seems to be churning workforce.”

Strong field supervision has become key to managing that deficit, but roles like experienced electrical foreman are also harder to fill. Hiring them has become “almost futile,” Padalecki says, so in-house candidates are being moved into those slots faster than he might prefer.

A shortage of qualified workers is making it harder for Hunt Electric Corp., (No. 18), Eagan, Minn., to pursue all the opportunities it would like.

“There are fewer projects where we feel like we can bring the resources to make it successful,” says CEO John Axelson.

To get more out of its workforce, Axelson says the company is trying to improve labor management, “going further down into the ranks to find people to lead and do a better job of getting them ready for that than in the past.”

Better labor management is also one way Everus companies are addressing labor supply challenges. Thiede says its firms are largely securing the skilled trade workers they need and matching their labor realities to business opportunities, but the emphasis on securing strong management talent is growing also. Companies are looking for more college-trained people for field supervision, estimating, and project manager roles, Thiede says, and the hunt is on for “people with fresh ideas willing to look at things differently.”

Tech training seen key

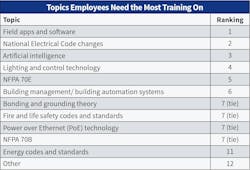

With skilled and experienced workers harder to find and keep training has taken on more urgency. The increasing complexity and breadth of electrical work is also a contributor. But contractors may have their work cut out for them wedging technical training into their schedules, so focus areas must be prioritized. Again this year, that’s technology and codes, broadly. Apps and software used in the field, the National Electrical Code, and artificial intelligence were the top choices for training areas most needing support (Table 3).

Ensuring that employees know their way around key information technology tools is increasingly vital. They have been critical to improving productivity and communication, especially in the field through mobile devices, which contractors say have become especially helpful to workers needing product specifications, codes and standards requirements and installation instructions (Table 4).

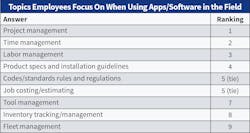

Specialized apps and software, too, are helping workers bridge the knowledge and experience deficit that has widened. Contractors say they’re most useful, and more so since last year, in project management. Also topping the useful list are time management, labor management and product specs and installation guidelines (Table 5).

While technology in the field has come a long way, Borchardt says, ICS still sees adoption and utilization gaps that need to be filled. A workforce trending ever younger will help with that transition, but more focused training on how to best use and apply it will help ensure it infiltrates the company’s work processes.

“The days of the craft worker not needing to rely on some of electronic device are behind us,” he says. “Not enough is being done as an industry to get this training out to the workforce. But it’s not always classroom; we’re finding peer training is key.”

Hunt Electric’s Axelson is hopeful his firm and the industry boost adoption of job site technology. Other industries have moved well ahead of construction on that front, but the gap could close with the help of emerging AI applications.

“There will be continued adoption of new technologies in the field, and it will help us from a productivity standpoint as it has other industries,” Axelson says.

AI to the rescue?

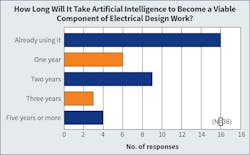

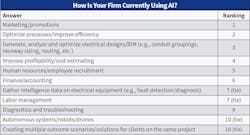

There’s seemingly no limit to projections about what AI may be able to deliver on the business management front, and that’s evident in Top 50 contractor views. Reported utilization of AI, with 42% saying they’re using it (Fig. 21), is up 18 points. Those in that camp say AI is broadly useful, but especially in marketing/promotion work, efficiency improvement and electrical design (Table 6).

“AI is coming fast for us,” says Padalecki. “It’s not going to make the screwdriver turn any faster, but it will enable better workflows. More processes are being automated and it’s helping us identify constraints and gaps in those processes.”

At Sargent Electric, Smith says he’s hopeful AI will deliver on its many promises. For now, it’s helping on the margins with contract reviews and report writing. Down the line it might cut back on labor needs, but it’s too soon to say.

“We’re short of seeing step changes in productivity and don’t see major headcount changes coming from it, but maybe doing more with the headcount we have,” he says.

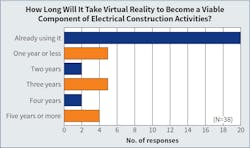

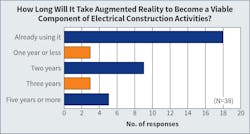

The strong pickup on AI among contractors might bode well for further technology adoption, an area where construction has lagged. But uptake on two tools that seem a natural fit for helping better merge design and construction for improved project planning and outcomes — augmented and virtual reality (AR/VR) — has been halting with no clear trend visible.

This year’s survey reflects that, with reported current VR usage up 15 points to 53% (Fig. 22) and AR usage flat, at 47% (Fig. 23). Half using the tools, though, indicates some commitment, as does concurrence that there’s a range of potential applications.

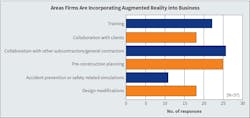

Collaboration, pre-construction planning and training are seen as top candidates among several for possible AR application (Fig. 24). Far fewer this year, though, see client collaboration and accident prevention as potential uses for AR. More, though, see it being used for collaboration with other contractors.

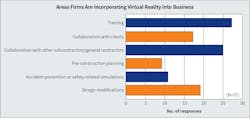

For VR, top likely uses are training, contractor collaboration and design modifications (Fig. 25). Accident prevention and product/equipment testing bring up the rear and dropped further in mentions.

Hunt Electric’s chief is cautious about making predictions for both tools at his firm because so much will depend on the evolution of a critical mass of industry usage. Modeling teams are working with them some and they are showing some potential, Axelson says, but “we haven’t seen adoption with GCs or owners to where it will become as utilized as BIM modeling. Eventually, we may get there.”

At E-J Electric, though, AR/VR is solidly in the mix of technology aids, helping improve job-site visualization, training, and planning. Mann says both, along with other technologies, are “giving us a competitive edge and allowing us to deliver smarter, faster, and more cost-effective solutions.”

About the Author

Tom Zind

Freelance Writer

Zind is a freelance writer based in Lee’s Summit, Mo. He can be reached at [email protected].